Download

1 / 19

190 likes | 200 Views

Learn about the importance of savings and the advantages and disadvantages of using credit. Understand credit terms and how to develop good credit. Explore real-life case studies on bank loans and the use of long-term vs. short-term credit. Discover the hidden costs of credit and the impact of interest rates on your payments.

E N D

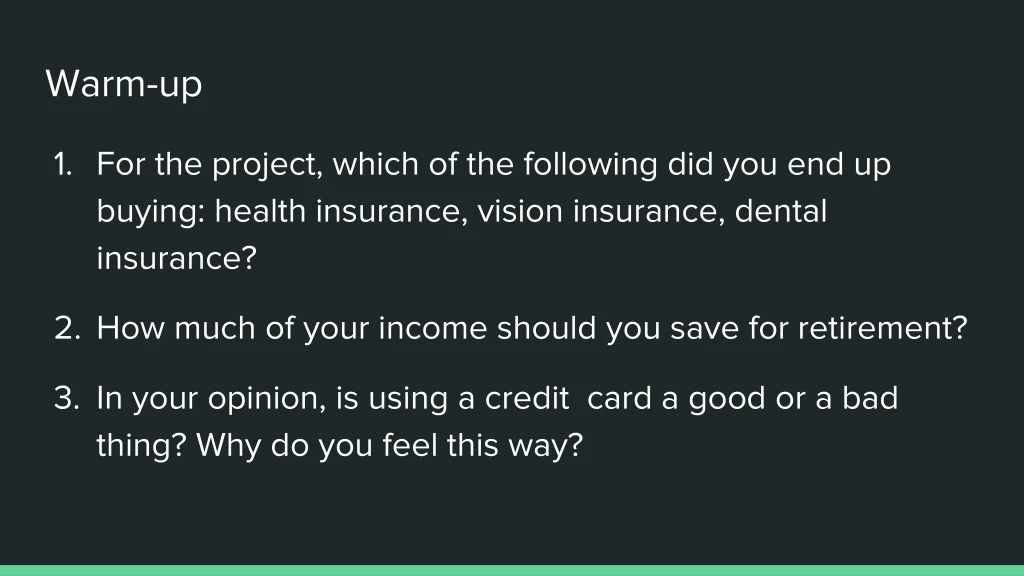

Warm-up • For the project, which of the following did you end up buying: health insurance, vision insurance, dental insurance? • How much of your income should you save for retirement? • In your opinion, is using a credit card a good or a bad thing? Why do you feel this way?

POCKETS: SAVINGS & CREDIT Unit 7

SAVINGS Most planners will tell you that you ought to keep at least 3 months’ living expenses in an insured savings account or money market account. If you are a contract employee or a seasonal worker, they will probably say 6 months.

Advantages of Credit Disadvantages of credit 1. Immediate Possession 2. Flexibility 3. Safety 4. Emergency Funds 1. Overspending 2. Higher Cost 3. Impulse Buying

When you are deciding to use credit, there are some questions that you should ask yourself before you proceed: 1. Do I really need this item or can I wait? 2. What is the least amount that I have to borrow? 3. How much are the interest rate (APR) and other fees? 4. How much is the monthly payment and when is it due? 5. Can I afford the monthly payment? 6. What will happen if I do not make the payments on time? 7. What will be the extra cost of using credit and is it worth it? 8. What will I have to give up to pay for it?

Credit Terms • People who borrow are called debtors. • The people who loan money are called creditors. • Finance charges, is the amount that is paid over the original loan amount, which is the interest plus any other additional fees. • Annual Percentage Rate (APR) is the rate of interest that is paid every year on a loan for the use of the money.

Credit Terms • A credit report is a record of one’s personal financial transactions or credit history. A credit score is a number that reflects creditworthiness.

Credit Terms • Secured Credit is credit for which the consumer must put up some property of value (collateral) to cover the amount of the loan. • Money that is loaned on nothing but the promise to repay in the future is called Unsecured Credit. • Charging any amount above a legally set amount is called Usury.

Developing Good Credit • Always pay bills on time. • If you have a savings account, it’s good to make additional regular deposits, no matter how small. Lenders like to see a consistent savings pattern. • It’s better for your credit score to maintain a low balance on one card and pay it off each month than to have no balance at all. • AVOID: Writing checks you do not have enough money in your account to cover. Having a lot of credit cards and loans. Changing credit cards frequently

Bank Loans Case # 1 Donna is a single mother of two children. Her only source of income consists of public assistance payments of $650 a month and $120 per month from the pension from her late husband. She wants to purchase new kitchen appliances totaling $989. She lives in subsidized housing. Her share of the rent and other expenses total $575 a month.

Bank Loans Case # 2 Bruce is a bricklayer who is always looking for work. Due to weather and other factors, he is seasonally unemployed. He currently brings home $950 a month. He owes $200 a month for his car, $175 a month for the High Definition big screen TV, and $300 a month for rent and has no money saved in the bank. He wants to borrow $4,000 to purchase a motorcycle.

Bank Loans Case # 3 Susan, 22, is in her second year of college. She has excellent grades in school and plans to attend medical school after graduation. Until recently her parents paid her bills, but are now unable to and she is on her own. She is seeking $10,000 dollars to finish college and pay her living expenses. She has never borrowed any money before but plans to repay her loan when she graduates from medical school.

Why would a person use long versus short-term credit (Payday loans)? http://freakonomics.com/podcast/payday-loans/ What types of purchases would they make with each type of credit?

While use of credit has advantages, it also can come at a price. The biggest part of that price is usually the interest rate. Advertisers like to focus on the monthly payment—“Buy it now for only $99 a month” or, only a “$15 monthly minimum payment”—but they don’t tell you how much you will really pay for the item. Let’s assume that you spent $375 on new clothing and shoes. How many months will it take you to pay off $375 if you makes the minimum payment of $15 each month? Are we missing anything here? Are we sure that it is only going to take Tiffany 25 months?

When Tiffany signed up for her credit card, or when she received it in the mail, did she ever check to see what the APR was on the card? Let’s assume the APR was 21%. How will this affect the amount that Tiffany has to pay off, as well as the amount of time it will take her? According to the chart, how many months did it take Tiffany to pay off her purchase? How much did her $375 in clothing end up costing her due to the high percentage rate?

Given these negative factors, why do you think people still sign up for credit cards? What is a likely mistake you could make after putting a lot of debt on one credit card? What consequences could you face if you opens additional credit cards? What consequences would you possibly face if you miss a monthly payment, or are unable to make the payment for consecutive months?

Credit Laws • Credit CARD Act of 2009

Credit Laws • Under the Fair Debt Collections Practices Act, consumers are protected from abusive and unfair collection practices. Collectors are limited to reasonable times and places. Acts of harassment or abuse and misleading or false statements are prohibited.

Explain how consumer protection laws and government regulation contribute to the empowerment of the individual (e.g., consumer credit laws, regulation, FTC-Federal Trade Commission, protection agencies, etc.). Summarize various types of fraudulent solicitation and business practices (e.g., identity theft, personal information disclosure, online scams, Ponzi schemes, investment scams, internet fraud, etc.). Summarize ways consumers can protect themselves from fraudulent and deceptive practices (e.g., do not call lists, reading the fine print, terms and conditions, personal information disclosure, investment protection laws, fees, etc.). The nature of compound interest as it relates to debt. Options available to the consumer if debts reach an unsustainable level. The consequences of bankruptcy. Consumers often protect themselves from unfair or deceptive practices by filing lawsuits against people or businesses that use unfair or deceptive practices. Federal Trade Commission (FTC), Consumer Finance Protection Bureau (CFPB), state attorney general offices, departments of consumer affairs, etc. https://www.justice.gov/criminal-fraud/mass-marketing-fraud