Download

1 / 12

120 likes | 228 Views

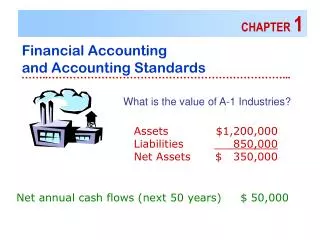

CHAPTER 1. Financial Accounting and Accounting Standards. ……..…………………………………………………………. What is the value of A-1 Industries?. Assets $1,200,000 Liabilities 850,000 Net Assets $ 350,000. Net annual cash flows (next 50 years) $ 50,000. Accounting provides Information. Assets &

E N D

CHAPTER 1 Financial Accounting and Accounting Standards ……..…………………………………………………………... What is the value of A-1 Industries? Assets $1,200,000 Liabilities 850,000 Net Assets $ 350,000 Net annual cash flows (next 50 years) $ 50,000

Accounting provides Information Assets & Liabilities Future Cash Flows Investors Creditors Government Agencies

Assets $1,200,000 Liabilities 850,000 Net Assets $ 350,000 Net assets might not reflect firm value: • Most assets are recorded at historical cost. • Intangible assets are frequently not recognized. Net annual cash flows (next 50 years) $ 50,000 A $500,000 investment would yield a 10% return. A $1,000,000 investment would yield a 5% return.

2003 2004 2005 Future Cash Flows • Characteristics • amount • timing • uncertainty • Important to investors & creditors

equipment / depreciation gains / losses sales stock options inventories pension obligations • Projecting future cash flows • requires more than just current cash flows • financial reporting provides information

? March 2000 Market value $25.6 billion ? amazon.com 4th quarter 1999 Operating loss $185 million Net loss $323 million

Possible explanations Current financial reporting is irrelevant! • backward looking • neglects intangibles • “rules” have changed Market was overpriced! (A bubble)

Objectives of Financial Reporting • Information to stockholders and creditors • Future cash flows • Assets and liabilities Challenges of Financial Reporting • Non-financial measurements • Forward-looking information • Intangible assets • Timeliness

PARTIES INVOLVED IN STANDARD SETTING • Federal agency • Requirements for all companies that issue stock SEC • Accounting must conform to GAAP CAP ’39 – ‘59 APB ’59 – ‘73 FASB ’73 – present • Private organizations • Set accounting standards

FAF AICPA CAP ’39 – ‘59 ASB APB ’59 – ‘73 • Concepts • Standards • Interpretations • Technical Bulletins • Emerging Issues • Rsrch Bulletins • APB Opinions • Auditing Stnds • Guidelines • Stmnts of Position • Practice Bulletins FASB

ISSUES IN FINANCIAL REPORTING The Political Environment • “The FASB is committed to rendering its final decision without regard to any of the social, economic, or public policy considerations.” (J.Carter Beese, SEC) • “Truth in accounting means telling it like it is, without bias or intent to encourage any particular mode of behavior.” (Dennis Beresford, FASB) • Other post-employment benefits (OPEB), stock options, derivatives, etc.

Responsibilities of Accountants • Detect fraud? • Verify that financial reporting rules have been followed (i.e. proper form)? • Ensure that the accounting reflects the substance of the economic event? • Auditor independence • Expectations gap