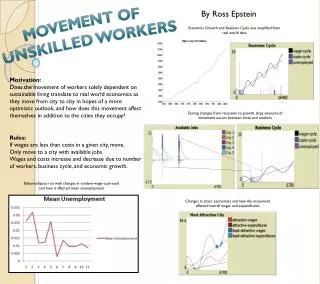

MOTIVATION

MOTIVATION. Chapter 4: Linear Algebra. Vector Spaces Algebra of Matrices Inverse Matrix. MOTIVATION. VECTOR SPACES: MOTIVATION.

MOTIVATION

E N D

Presentation Transcript

MOTIVATION Chapter 4: Linear Algebra Vector Spaces Algebra of Matrices Inverse Matrix

MOTIVATION VECTOR SPACES: MOTIVATION Most mathematical objects representing physical system will turn out to be vectors. We already know many of them: position, velocity, acceleration, forces electric field, but there will be many others like the wave functions of quantum mechanics describing the probability of a system to be in some given configuration. When not describable by vectors, systems will be described by generalization of vectors, called tensors. You will study tensors later in your career! Now physical laws act on systems. Very often this action, if linear, can be represented by matrices. Remember how in the last chapter, the change of basis, or the rotation of vector, was written in terms of a matrix. Well, this is a very common occurrence and thus in this chapter we must study: • First, vector spaces • then matrices And since manipulating matrices will involve dialing with determinants, we’ll study: • determinants as well. hence the 3 sections of this chapter!

I. VECTOR SPACES A. DEFINITION A vector space over the Reals (respectively complexes) is a space made up of elements (vectors) subject to 2 laws, usually called “addition” of vectors and “multiplication” of vectors by reals (resp. complexes) satisfying the following properties V is a Group with respect to has the following properties:

I. VECTOR SPACES B. BASES Linear Combination: A linear combination of vector is a vector of the form: Linear Independence: A setof vectors is linearly independent if on cannot find real numbers Such that: In-particular vectors that are proportional to each other are obviously linearly dependent. Basis: A set of linearly independent vectors is called a basis if: ; In other words can be written as a linear combination of the basis vectors. Theorem: If a basis has n vectors, then all bases must have n vectors. And n is called the dimension of the vector space Proof: Assume a basis B1 with n vectors. And another with m vectors, and

I. VECTOR SPACES C. VECTOR COMPONENTS Vector Components: They are the coefficients of the decomposition of a given vector on the chosen Basis. Theorem: Decomposition on a basis is unique D. INNER PRODUCT and NORM Given a vector space V, an inner product is a bilinear map of VV into the Reals. .

I. VECTOR SPACES E. EXAMPLES 3D Euclidian space: with Euclidian norm: Minkowski Space: with Minkowski norm: Functions: Functions form an infinite dimensional vector space but polynomials of degree n over the reals form a vector space of degree n+1. example n=2 then P2(x)=a+bx+cx2

I. VECTOR SPACES A. DEFINITION cont’d E4.1-1: Addition of 2 matrices= matrix obtained by adding matrix elements i.e. C=A+B iffcij=aij+bij Multiplication by a real: C= l A iffcij= laij Show that 2x2 matrices form a vector space w/ respect to matrix addition and multiplication by a number. What is the identity element? E4.1-2: Show that 2 D Euclidian space of our usual physics “vectors” is a vector spacewith respect to additions and multiplication by a scalar as usually defined. Given a vector V=(1,0) find a vector W which is linearly independent of V. Show then that any other arbitrary vector A=(a,b) must be linearly dependent on V and W. Write explicitly the expression of A in terms of V and W • E4.1-3 Consider the vect. Space of 2x2 matrices defined in 4.1-1. • Find a basis of the space: • guess the basis and show that it is linearly independent • prove that any matrix can be written in terms of that basis by doing it explicitely • What is the dimension of that space?

II. ALGEBRA OF MATRICES A. MATRIX DEFINITION – coeff are Reals (Resp. Complexes) B. MATRIX MULTIPLICATION • Composition of linear transformation on vectors leads to definition of matrix multiplication:

II. ALGEBRA OF MATRICES B. MATRIX multiplication cont’d C=AB defined such that C=[cij] where And in general for any nxn matrices: (1)

II. ALGEBRA OF MATRICES C. MATRICES form Group with respect to Multiplication Group: a group is a set whose elements are subject to an operation: with the properties: Closed under is associative has an identity element Any element has an inverse If also commutative group is called Abelian Matrices form a non-Abelian group with respect to Matrix multiplication. : Non-commutative: (eg if n=3 consider a rotation around x axis then z axis and compare to z then x rotation): Closure: Associative: E4.2-3: Use Mathematica to compute (AB)C and A(BC) and show that associativity is verified

II. ALGEBRA OF MATRICES C. MATRICES form group, contn’d Identity matrix: Find matrix I such that AI=IA=A for any A: Thus we require: Solution: if and if Solution is valid for any arbitrary A We often write: where delta is called the Kronecker symbol defined by: We also write: or Inverse: harder to study, brings in knowledge of determinant etc… so topic of next section. E4.2-4 Show that a 2x2 matrix representing a rotation of 300 composed with a 2x2 matrix for a rotation of -300 gives the identity as it should.

III. INVERSE MATRIX A. EXAMPLE: COMPUTATION A-1 in n=2 case

III. INVERSE MATRIX A. EXAMPLE: COMPUTATION A-1 in n=2 case

III. INVERSE MATRIX B. DEFINITION OF DETERMINANTS Permutation “symbol” (or Levi-Civita symbol) Definition of determinant in terms of permutation symbol: See how it works for n=2 Example [3x3] matrix:

III. INVERSE MATRIX B. DEFINITION OF DETERMINANTS 4.3-1 Compute determinant of rotation matrix in 2dim. (3 dim is harder) and compute the det of a stretch: conclusion? E4-3-2 Show that the vector is the cross product of A and B Note: In n dimensions the determinant sum consists of all the terms made up of n factors with no two factors being in the same row or column. Proof: the row numbers are all different (just look at the definitions) and any two identical column numbers would generate 2 factors in the sum that would cancel because of the Levi-Civita symbol Thus since any of the rows appear only once exactly (i.e. each term in the sum has all rows represented exactly once), and any of the columns appear only once as well (i.e. each term in the sum has all columns represented exactly once), we can rewrite our definition of the determinant as a sum over the rows just as well as the sum over columns we had:

III. INVERSE MATRIX C. Some VERY useful PROPERTIES OF DETERMINANTS Note that if any two columns are the same, or proportional, the determinant is zero. Thus a ZERO DETERMINANT INDICATES LINEAR DEPENDANCE of the corresponding vectors! • If a column is added to another (or first multiplied then added), the determinant is unchanged! Let, for instance: Let’s multiply the 2nd column by lambda and add that to the first: Developing along the modified column we get: Expanding the above det, we get: But that’s nothing more than: Because the 2nddet is zero, we have proved our theorem in this simple case

III. INVERSE MATRIX C. Some VERY useful PROPERTIES OF DETERMINANTS Likewise, as in 2, if a ROW is added to another (or first multiplied then added), the determinant is unchanged! E4.3-3 Prove this (#3 above) for a 3x3 matrix adding l*(3rd) row to 2nd row. • If a column, or a row, is multiplied by a number, the determinant is multiplied by that number! E4.3-4 Prove this using the definition of the determinant.

III. INVERSE MATRIX D. COFACTORS Definition of cofactors of a matrix a=[aij]: Where is the minor determinant of aij obtained by computing the determinant of the (n-1)x(n-1) matrix obtained by removing the ith row and jth column to [aij]. [aij] is the matrix of cofactors. Example: Cofactors of a 3x3 matrix Now let’s compute the following sum along one row or one column: Note: All results give the same answer which is also the DETERMINANT !!!!! E4.3-5 Compute the matrix of cofactors of a 2x2 matrix and show that all possible sums give the determinant. E4.3-6 Compute the determinant of a diagonal matrix diag(a11,a22,………….,ann)=

III. INVERSE MATRIX D. COFACTORS Expression of the determinant in terms of the cofactors (general expression): E4.3-7 Compute the matrix of cofactors of and show that all possible computations of the determinant give the same answer. Use the two expressions above (6 computations). Now use the original expression with the Levi-Civita symbol (ij…) and show that it gives again the same answer.

III. INVERSE MATRIX E. EXPRESSION OF INVERSE MATRIX E1. Preliminaries:we know: The preliminary result is to show that: We prove this preliminary result for n=3 (and will only give a taste of the proof for an arbitrary n): Starting from the matrix We first compute the matrix of cofactors: Then, as an example, we compute for i=2, and k=3

III. INVERSE MATRIX E. EXPRESSION OF INVERSE MATRIX Now let’s try: and let’s show that is zero again since I and k are different: This sum clearly adds up to zero (terms cancel 2 by 2) but it is useful to realize that it can be can be written as the following determinant: which is again obviously zero because two rows are identical: the i=1 and the k=3 rows! Since we already know that as we proved earlier, we can put together the two results as: When i=k we get the det since , and when we get zero as we just proved for a couple cases: i=2, k=3 and i=1, k=3. This completes our proof for n=3. The proof for a general n is more complicated. I just give a taste of it on the next slide. Our inverse matrix is now at hand: E2. Expression of the inverse: First we define the transpose matrix of A (A being the matrix of cofactors of a)as: Thus our preliminary result can be written as: Which in matrix form is expressed as: Which prove that if the determinant of a matrix is non-zero its inverse is given by: (if det is zero the inverse does not exist)

III. INVERSE MATRIX D. EXPRESSION OF INVERSE MATRIX OPTIONAL: GENERAL CASE proof of : for arbitrary n: Again, we compute: Since we remove , it follows that if, then the row i will be represented twice in the factors since all the rows but k are represented already. And because we’ll then have 2 identical row the entire expression will vanish. If i=k, then will nicely take the place of the removed and thus give us the determinant of “a”. The details of the proof are a little hard, since we have to take into account the and turn the into an n.

III. INVERSE MATRIX D. EXPRESSION OF INVERSE MATRIX E4.3-8 Compute, by hand, the determinant, then the matrix of cofactors then the inverse if it exists of the following matrices: Then multiply the inverse matrix by the matrix to show that it gives the identity; Do both a-1a and aa-1 E4.3-9 Use mathematica to do 4.3-8 E4.3-10 Use expression of the inverse to compute the inverse matrix of a rotation by qin 2dim. Comment on the result (what is the rotation angle of the inverse matrix?) Then multiply your inverse by the original matrix to prove you get the identity. E4.3-11 Compute the inverse of a stretch by and again multiply by original to show that you get the identity.