Download

1 / 14

140 likes | 170 Views

Learn about qualified profit sharing, eligibility and vesting rules, formulas for contributions, integration with FICA, withdrawals options, savings plans, and employer stock in qualified plans.

E N D

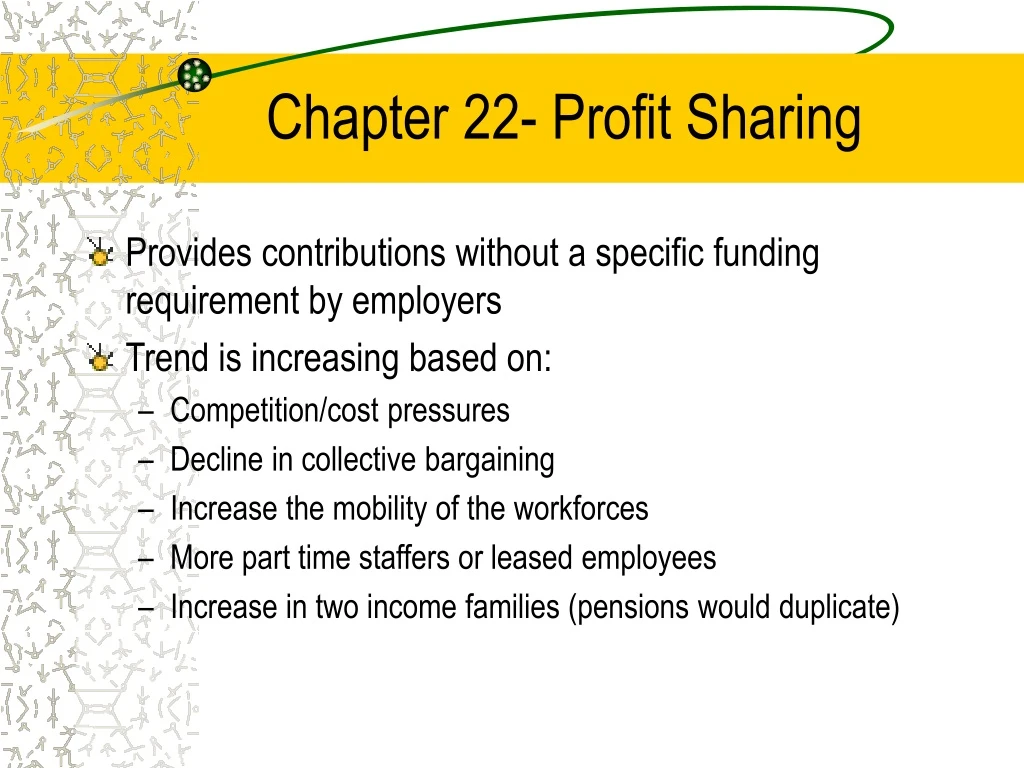

Chapter 22- Profit Sharing • Provides contributions without a specific funding requirement by employers • Trend is increasing based on: • Competition/cost pressures • Decline in collective bargaining • Increase the mobility of the workforces • More part time staffers or leased employees • Increase in two income families (pensions would duplicate)

Qualified Profit Sharing • Defined contribution plan in which the employer’s contributions are based on profits. Even non-profit firms may have plans; • Characteristics: • Specified percentage of profits each year, but in unprofitable years, nothing must be provided • Nondiscriminatory formula for allocating the contributions to employees

Qualified Profit Sharing • Since it’s a DC plan, benefit is in each employee’s account, available at termination or lump sum retirement payment • Plan may permit employee withdrawals or loans during employment • Eligibility and vesting are generally liberal because it’s an incentive plan • Forfeitures are reallocated to remaining participants (helps long service employees) • Limited to 15% of payroll of covered employees

Eligibility & Vesting • Minimum age requirement of 21 • Not longer than one year waiting period (or 1 ½ years if based on plan entry dates) • IRS requires that contributions be substantial and recurring so company cannot delay payments too many years

Formulas • A company wide percentage of contribution is determined by the firm. For example, if the company achieves its revenue goals, a specified percentage of sales above that amount would be paid into the profit sharing plan. • Then the firm has to take this amount and divide it up on a non discriminatory basis among all eligible employees.

Formulas • If the plan is based on compensation, it may be base pay or total pay including incentives. Only the first $150,000 (as indexed for inflation) of each employee’s earnings is considered for the annual contribution. On individual basis, it can’t exceed $30,000 or 15% of compensation (1995 figures – indexed in future). • Service is another factor used in the formula. You have to be careful that service does not lead to favoring highly compensated employees.

Formulas • Profit sharing plans do not require a fixed retirement benefit. The plan operates as a supplemental form of incentive compensation rather than a retirement plan. • It can be purely discretionary but the formula type of plan is more useful an an incentive plan.

Integration with FICA • Profit sharing plans may be integrated with social security to avoid duplication of benefits and reduce plan costs to the employers. • The maximum amount that an employer can deduct for profit sharing contributions is 15% of the compensation paid during that year to all employees that are participating in the program.

Withdrawals • IRS allows preretirement withdrawals of employer-contributed amounts after as little as 2 years after contribution or 5 years of participation. ‘Hardship’ withdrawals are allowed. • 10% early withdrawal penalty before 59½, death or disability; • As with pension plans, profit sharing plans may provide incidental death or disability benefits.

Savings Plans • Employees take after tax contributions usually with matching employer contributions. They are currently used in conjunction with a 401(k) plan, since a savings plan alone does not allow maximization of the potential tax benefits from a qualified plan.

Employer Stock in Qualified Plans • QP may not invest more than 10% of assets in employer stock. Employees are allowed to vote as shareholders on issue. Advantages: • Market can be created for employer stock • Employer can obtain a deduction for noncash contributions to the plan • Employees receive an ownership interest in the firm, may act as an incentive for better performance • Unrealized appreciation of stock is not taxed to the employee at time of distribution but only when employee sells the securities, then it is taxable as capital gain.

Employer Stock in Qualified Plans • Two types of QP • Stock Bonus Plan – a DC plan similar to a profit-sharing plan except that employer’s contributions are not dependent on profits; benefits are distributable as stock of the employer company. Typically, formula is based on employee compensation. Employer contributions may be in cash or stock into individual employee accounts. Employees may contribute after-tax dollars. Value is stated in ‘x’ number of shares and dividends may be used to buy more stock or can be currently taxable income if taken as cash.

-Employer Stock in Qualified Plans • ESOP – Employer Stock Ownership Plan – is a stock bonus plan with additional feature. The plan can be used by employer to raise funds on a tax-favored basis. The funds can be used for any purpose, not just company stock! The ESOP allows a firm to indirectly borrow money from bank and repay the loan with fully deductible payments (not just interest). Figure 22-2 explains in detail (p. 571).

ESOP • ESOP contribution allocation formula may not be integrated with social security • Diversification requirement – employees age 55 with 10 years of service are entitled to an annual election requiring the employer to diversify investment in the participant’s account (to reduce investment risks). The plan must offer at least 3 investment options, other than employer stock.