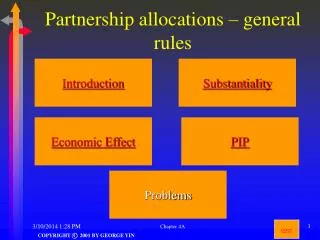

Partnership allocations – general rules

Partnership allocations – general rules . Introduction. Substantiality. Economic Effect. PIP. Problems. oper. Partnership allocations - introduction. lots of flexibility why? problem with flexibility responsibility. Orrisch.

Partnership allocations – general rules

E N D

Presentation Transcript

Partnership allocations – general rules Introduction Substantiality Economic Effect PIP Problems Chapter 4A oper

Partnership allocations - introduction • lots of flexibility • why? • problem with flexibility • responsibility Chapter 4A

Orrisch • special allocation of depreciation deductions and gain chargeback to O • evidence of tax avoidance purpose: • depreciation deduction is predictable amount; • O had taxable income, C did not; • C avoids future CG tax. • TP: merely equalize capital accounts • TP: SEE met – do capital account adjustments consistent with tax allocations insulate the latter from challenge? Chapter 4A

Orrisch (simplified facts) • O and C each contributes $1,000 to the OC partnership which purchases 5-year depreciable property for $2,000. • In the first 3 years, partnership income and expenses are exactly equal except for $400 of depreciation deductions each year which are all allocated to O. • Beginning year 4, partnership sells the property; parties agree to allocate any gain disproportionately to O equal to prior allocations of depreciation to him. • All other items to be split equally. Chapter 4A

Orrisch: capital accounts O,C: $1,000 initial contributions $400 depreciation/yr – all to O sale yr. 4 – gain chargeback to O all other items shared equally Chapter 4A

Orrisch: capital accounts O,C: $1,000 initial contributions $400 depreciation/yr – all to O sale yr. 4 – gain chargeback to O all other items shared equally Chapter 4A

Orrisch: capital accounts O,C: $1,000 initial contributions $400 depreciation/yr – all to O sale yr. 4 – gain chargeback to O all other items shared equally Chapter 4A

Orrisch: capital accounts O,C: $1,000 initial contributions $400 depreciation/yr – all to O sale yr. 4 – gain chargeback to O all other items shared equally Chapter 4A

(iv) rules respect pos. bal. on liquidation EE no deficit DRO take into account expected dists. substantiality shifting QIO transitory overall test Section 704(b) regulations or alt EE or “DBL” SEE PIP deemed PIP Chapter 4A

Problem 4-1 • G (general partner) and L (limited partner) each contributes $100K to partnership GL which purchases 10-year depreciable property for $200K cash • L has no DRO; otherwise, EE tests are met. • partnership agreement contains a QIO. • all dep allocated to L • partnership breaks even except for $20K/yr. in depreciation deductions. Chapter 4A

Problem 4-1(a) G,L $100K contribs. each all dep allocated to L GL breaks even except for $20K/year depreciation L-no DRO Chapter 4A

Problem 4-1(b) G,L $100K contribs. each all dep allocated to L GL breaks even except for $20K/year depreciation L-25 DRO Chapter 4A

Problem 4-1(c) G,L $100K contribs. each all dep allocated to L GL breaks even except for $20K/year depreciation L-no DRO Chapter 4A

Problem 4-1(d) G,L $100K contribs. each all dep allocated to L GL breaks even except for $20K/year depreciation L-no DRO Chapter 4A

Problem 4-1(e) G,L $100K contribs. each all dep allocated to L GL breaks even except for $20K/year depreciation L-no DRO Chapter 4A

Blank Chapter 4A

Rev. Rul. 97-38 • G (general partner) and L (limited partner) each contribute $100K to partnership GL which purchases 5-year depreciable property for $200K cash and a $800K recourse note. • L has no DRO; G to restore deficit only to pay creditors, not L; otherwise, EE tests are met. • partnership agreement contains a QIO. • all tax items to be shared equally, except all depreciation deductions to G. • partnership breaks even except for $200K/yr. in depreciation deductions. Chapter 4A

Rev. Rul. 97-38 G’s limited DRO (end yr. 1): liabs: 800 value: 800 DRO: -0- Chapter 4A

Rev. Rul. 97-38 Chapter 4A

G’s limited DRO (end yr. 2): liabs: 800 value: 600 DRO: 200 Rev. Rul. 97-38 Chapter 4A

(iv) rules respect pos. bal. on liquidation EE no deficit DRO take into account expected dists. substantiality shifting QIO transitory overall test Section 704(b) regulations or alt EE or “DBL” SEE PIP deemed PIP Chapter 4A

A B 50% 50% allocate $50 t.i. $50 t-e inc. allocate $50 t.i. $50 t-e inc. AB partnership Reason for “substantiality” test $100 tax. inc. $100 t-e inc. Chapter 4A

(zero bracket) (high bracket) A B 50% 50% allocate $100 t.i. $0 t-e inc. allocate $0 t.i. $100 t-e inc. AB partnership Reason for “substantiality” test $100 tax. inc. $100 t-e inc. Chapter 4A

Orrisch: capital accounts O,C: $1,000 initial contributions $400 depreciation/yr – all to O sale yr. 3 – gain chargeback to O all other items shared equally Chapter 4A

Shifting and Transitory Allocations • is there strong likelihood that allocations will not affect substantially the CA balances of the partners yet will reduce their collective tax liabilities after taking into account their individual tax situations? • presumption of “strong likelihood” • “shifting”: allocations take place w/i single year • “transitory”: allocation in one year that is offset by an allocation in a subsequent year Chapter 4A

Value = basis rule Value = basis rule: there is never a “strong likelihood” that a special allocation of depreciation deductions will be offset by a later allocation of gain pursuant to gain chargeback provision Chapter 4A

Five-year rule • transitory allocation not present if the original allocations will not be largely offset within five years (determined on a FIFO basis) Chapter 4A

“Overall” Test for Substantiality • looks behind the pre-tax effect of an allocation on partners’ capital accounts • two-pronged inquiry: allocation must improve after-tax consequences of at least one partner and there must be strong likelihood that no partner is made worse off by the allocation (again determined after taxes) Chapter 4A

(iv) rules respect pos. bal. on liquidation EE no deficit DRO take into account expected dists. substantiality shifting QIO transitory overall test Section 704(b) regulations or alt EE or “DBL” SEE PIP deemed PIP Chapter 4A

Partner’s interest in partnership • partner’s share of economic benefit/burden corresponding to tax item being allocated • item-by-item determination • all partnership interests presumed equal • factors to consider: • partners’ relative contributions • partners’ interests in economic profits/losses • partners’ interests in cash flow/non-liq. distribs. • partners’ interests in liquidating distributions Chapter 4A

Deemed PIP • special rules provided to validate allocations of items which cannot have economic effect • tax credits • section 704(c) items • nonrecourse deductions Chapter 4A

Problem 4-3(a) Sale at the end of Yr. 6 Sale at the end of Yr. 5 book value: 80 book value: 100 book basis: 80 book basis: 100 G/L : -0- G receives $88 ($80 proceeds plus $8 from L’s contribution G/L : -0- G receives $100 Chapter 4A

Problem 4-3(b) Sale at the end of Yr. 1 book value: 180 book basis: 180 G/L : -0- G receives $100; L receives $80 Chapter 4A

Problem 4-4 • A (LP) contribs $80; B (GP)contribs $120 • A has no DRO; B has unlimited DR0 • PS buys dep prop--$200 • $50 annual dep ($200/4) • all items allocated 40:60, except dep allocated entirely to A • PS agreement satisfies requirements of alt EE test • contains gain chargeback provision Chapter 4A

Problem 4-4(a) Chapter 4A

Problem 4-4(b) Chapter 4A

Problem 4-4(c) Chapter 4A

Problem 4-4(d) Sale for $175 Sale for $250 Chapter 4A

Problem 4-4(e) Sale for $150 Chapter 4A

Problem 4-4(f) B has unlimited DRO B has limited DRO Chapter 4A

![G1 - COMMISSION'S RULES [5 Exam Questions - 5 Groups]](https://cdn0.slideserve.com/386427/g1-commission-s-rules-5-exam-questions-5-groups-dt.jpg)