Download

1 / 3

30 likes | 51 Views

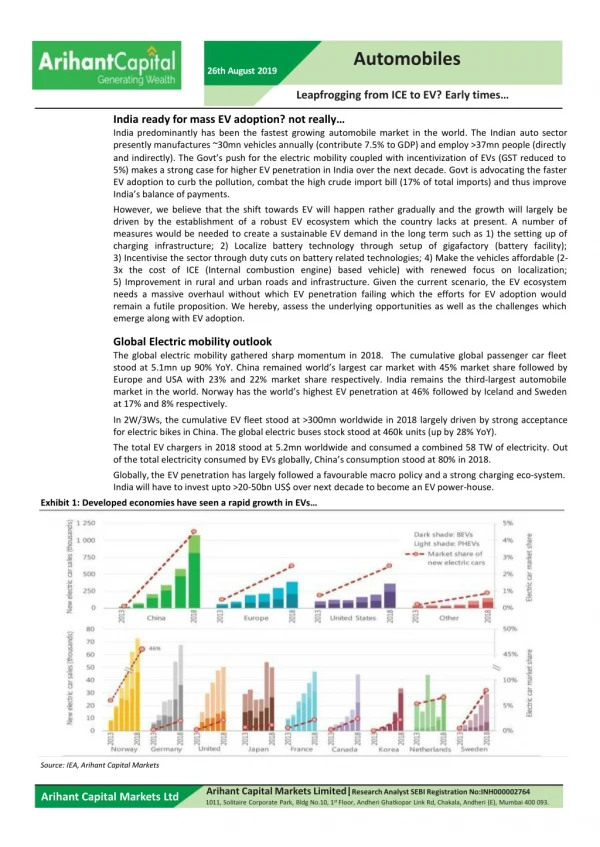

India predominantly has been the fastest growing automobile market in the world. The Indian auto sector presently manufactures ~30mn vehicles annually (contribute 7.5% to GDP) and employ >37mn people (directly and indirectly). The Govtu2019s push for the electric mobility coupled with incentivization of EVs (GST reduced to 5%) makes a strong case for higher EV penetration in India over the next decade.

E N D

Automobiles 26thAugust2019 LeapfroggingfromICEtoEV?Earlytimes… IndiareadyformassEVadoption?notreally… Indiapredominantlyhasbeenthefastestgrowingautomobilemarketintheworld.TheIndianautosector presentlymanufactures~30mnvehiclesannually(contribute7.5%toGDP)andemploy>37mnpeople(directly andindirectly).TheGovt’spushfortheelectricmobilitycoupledwithincentivizationofEVs(GSTreducedto 5%)makesastrongcaseforhigherEVpenetrationinIndiaoverthenextdecade.Govtisadvocatingthefaster EVadoptiontocurbthepollution,combatthehighcrudeimportbill(17%oftotalimports)andthusimprove India’sbalanceofpayments. However,webelievethattheshifttowardsEVwillhappenrathergraduallyandthegrowthwilllargelybe drivenbytheestablishmentofarobustEVecosystemwhichthecountrylacksatpresent.Anumberof measureswouldbeneededtocreateasustainableEVdemandinthelongtermsuchas1)thesettingupof charginginfrastructure;2)Localizebatterytechnologythroughsetupofgigafactory(batteryfacility); 3)Incentivisethesectorthroughdutycutsonbatteryrelatedtechnologies;4)Makethevehiclesaffordable(2- 3xthecostofICE(Internalcombustionengine)basedvehicle)withrenewedfocusonlocalization; 5)Improvementinruralandurbanroadsandinfrastructure.Giventhecurrentscenario,theEVecosystem needsamassiveoverhaulwithoutwhichEVpenetrationfailingwhichtheeffortsforEVadoptionwould remainafutileproposition.Wehereby,assesstheunderlyingopportunitiesaswellasthechallengeswhich emergealongwithEVadoption. GlobalElectricmobilityoutlook Theglobalelectricmobilitygatheredsharpmomentumin2018.Thecumulativeglobalpassengercarfleet stoodat5.1mnup90%YoY.Chinaremainedworld’slargestcarmarketwith45%marketsharefollowedby EuropeandUSAwith23%and22%marketsharerespectively.Indiaremainsthethird-largestautomobile marketintheworld.Norwayhastheworld’shighestEVpenetrationat46%followedbyIcelandandSweden at17%and8%respectively. In2W/3Ws,thecumulativeEVfleetstoodat>300mnworldwidein2018largelydrivenbystrongacceptance forelectricbikesinChina.Theglobalelectricbusesstockstoodat460kunits(upby28%YoY). ThetotalEVchargersin2018stoodat5.2mnworldwideandconsumedacombined58TWofelectricity.Out ofthetotalelectricityconsumedbyEVsglobally,China’sconsumptionstoodat80%in2018. Globally,theEVpenetrationhaslargelyfollowedafavourablemacropolicyandastrongchargingeco-system. Indiawillhavetoinvestupto>20-50bnUS$overnextdecadetobecomeanEVpower-house. Exhibit1:DevelopedeconomieshaveseenarapidgrowthinEVs… Source:IEA,ArihantCapitalMarkets ArihantCapitalMarketsLimited|ResearchAnalystSEBIRegistrationNo:INH000002764 1011,SolitaireCorporatePark,BldgNo.10,1stFloor,AndheriGhatkoparLinkRd,Chakala,Andheri(E),Mumbai400093. ArihantCapitalMarketsLtd

Automobiles IndiaEVoutlook:MassEVadoptioncanleadtometamorphosisacrosstheindustry… EVshaveasimplermanufacturingmechanismvstheICEvehicle(partsgetreducedby2/3rdinEV)andthuswill definitelyleadtoentryfromtheglobalpeersinthissegment.Aswecanseeinexhibit1,theshiftfromICEto EVwillleadtobatterypackwillform35%ofthevehiclecostandthedrivetrainwillundergosignificant transformationastheelectricmotors,inverterandcontrolunitsreplacestheexhaustsystemand transmission.Weexpectalotofautocomponentplayerstoundergosignificantamountofde-riskingoftheir businessesovernextfiveyearsthroughintroductionofnewproductswithJVs/tie-upswithinternational players. EnduranceTech MindaIndustries MindaCorp AsEVtechnologyevolves,focuswouldbeonlight-weightingthroughaluminiumdie-casting/alloywheels,DC motors,batterymodule,wiringharnessandADAS(advanceddriverassistedsystem)andadvancedtelematics. BharatForge Exhibit1:TheshiftinvehiclecompositionfromICEtoEV(batterypackforms~35%ofthevehicle) EV Batterypack ICE Others 5% 35% Electricmotor 40% Chassis 15% Exhaussystem 10% Auxsystem 12% Drivetrain 20% Others 7% Drivetrain 35% Engine 42% Vehicle body 20% Auxsystem 16% Transmission 32% Inverterand controlunit 48% Chassis 8% Equipment 20% Vehiclebody 10% Equipment 25% Source:Company,ArihantCapitalMarkets ChallengesandopportunitiesinEV SprucingupthecharginginfrastructureremainskeyforEVadoption ThesuccessofEVswillbedrivenbyPan-Indiainstallationofchargingstations.TheGovtistakingnecessary stepstoaddressthischallengethroughadequatetie-upscoupledwithincentivizationthroughtheFAMEII scheme(Rs10kCrsubsidy)toattractEVbuyers.Presently,thereare150publicchargingstationsinIndia(vs 976kstationsinChinaincluding401kpublicstations).Wethusbelievetheinstallationofpubliccharging stationswillberequiredtofirmlyrolloutEVadoption.Thechargingstationsshallattractinvestmentsupto ~$15-25bnovernextfivetoeightyearswhichremainsaconcern.CompaniesinIndiasuchasABB,Acme Industries,FortumIndiahaveshowninteresttosetupbatterychargingstationsinIndia. BreakthroughinbatterystoragetechnologyshalldriveEVaffordability Thehighbatterycostsattached(35%ofvehiclecost)coupledwithlowvolumesleadtohighcostofownership forEVsandmakethemunaffordable.Anybreakthroughtowardsreductionofthecostofbatterymodulescan maketheEVsinexpensive.Themostcommonbatterymodulescompriseof1)NMC-graphitebatteriescells– whichusethenickel-manganese-cobaltascathodeandGraphiteasanode.Thesearethemostcommonly usedbatterycellsandcost$150-200/kWhhoweverhavealowlife-cycleof500chargings.2)NMC-LTO– Thesecellsuselithium-titanium-oxideasanodevsthegraphiteandcomewithlife-cyclesof10,000charging andcosts$450/kWh.3)LFP-Graphite–lithium-ferrous-phosphate-graphitehigherlife-cyclesvstheNMC-LTO batterycellscosts.Researchisunderwaytoincreasethebatterystorageby10xthusmakingthevehiclemore affordable. EVadoption–Buses–2Ws/3Ws–PVs Publictransport,speciallytheintra-citytransportbusescouldseeearliestEVadoptionastheyareknownto emithighestpollutingmaterialsfollowedby3Ws/2Wsintandem.ThePVscouldbethelastsegmentforEV adoptionduetohighcostsattached.TheGovthadrecentlydraftedaproposalforall3Wsandall2Ws<150cc toconverttoelectricby2023and2025respectively.However,theOEMbacklashcoupledwiththeunviability ofthecharginginfrastructureresultedinasofterstancebytheGovtrecently.Thisunderlinesthehurdles towardsEVadoption. ArihantCapitalMarketsLtd 2of3 26August,2019

Automobiles WeexpectEVstoseegradualadoptionoverFY19-FY32e WefirmlybelieveEVadoptionlikelytoseeagradualincreaseonaccountof1)aviablecharginginfrastructure; 2)IncreasedawarenessaboutEV;3)Focusoncostreductioninbatterystoragethroughlocalization.Wethus believe,FY20etobeaninflectionpointforIndianautomobileindustrywhereOEMswillbetechnologically wellversewiththeEVadoptionbyFY32ethusleadingtofastestadoptioninbuses(75%)followedby2W/3W with61%/64%respectivelyandthePVstoadoptgradually(38%)untilFY32onaccountofhighercostof ownershipvsICEvehicles. Exhibit1:TheshiftinvehiclecompositionfromICEtoEV(batterypackforms~35%ofthevehicle) 100% 75% 64% 80% 60% 59% 51% 49% 61% 38% 39% 40% 30% 26% 20% 0% 18% 7% 9% 1%2% FY19FY20eFY21eFY22eFY23eFY24eFY25eFY26eFY27eFY28eFY29eFY30eFY31eFY32e 3W2WPVBuses Source:Company,ArihantCapitalMarkets Heroin2WsandMarutiinPVstodrivethee-mobilityovernextdecade Wefirmlybelieve,amongstthe2Ws,Heroshallbenefitfromthe2Wadoptiononaccountofitsstrong presenceinEVsegmentwithproprietaryproductsanditsinvestmentinAtherEnergy(electric2Wstartup). ThecompanyshallenablesmoothtransitiontoEVsoverthenextdecade.Other2WOEMslikeBajajAutoand TVSareworkingonelectricbikes/scootershowevertie-upswithotherOEMs.InPVs,wefirmlybelieve,Maruti shallleadthepackwithastrongtechnologypartneravailableatitsbehestandthusdrivetheaffordable electricmobilityjuggernautoverthenextdecade.WhileM&MhasbeenvocalaboutEVaspirationsandalso remainsapioneerinthisspace,itspresentmodelshavenotabletogarnerdecentvolumesinEVs. Ratingscale EPS(Rs) FY20e 5 P/E(x) FY20e 12 ROE(%) FY20e 17 CMP (Rs) TP (Rs) Reco Company AshokLeyland BajajAuto FY19 FY21e FY19 FY21e 10 FY19 26 FY21e 17 60 75 ACCUMULATE ACCUMULATE HOLD 7 6 9 2750 6250 365 3021 6004 431 151 248 14 165 257 16 183 286 19 18 25 26 16 9 17 15 22 19 14 10 6 21 17 22 27 17 12 21 21 16 22 25 10 14 MarutiSuzuki TVSMotorCo HeroMotocorp M&M 24 16 HOLD 23 21 2642 533 2114 590 REDUCE HOLD 169 39 166 33 184 32 16 25 10 11 FiemIndustries 367 599 BUY 42 47 60 9 8 12 ArihantCapitalMarketsLtd 3of3 26August,2019