Download

1 / 17

170 likes | 299 Views

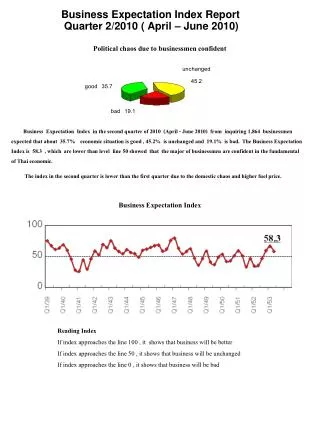

Qatar Business Optimism Index Q3 2010. Presented by Dun & Bradstreet Qatar Financial Centre (QFC) Authority. Business Optimism Index. The D&B Business Optimism Index is recognized world over as an indicator which ascertains the pulse of the business community

E N D

Qatar Business Optimism Index Q3 2010 Presented by Dun & BradstreetQatar Financial Centre (QFC) Authority

Business Optimism Index • The D&B Business Optimism Index is recognized world over as an indicator which ascertains the pulse of the business community • Provides insight into the short-term outlook of business units on key business parameters including sales, profits, pricing, headcount and investment • Provides analysis of major trends and issues concerning the business community

Survey • Sample of business units representing Qatar’s economy is selected • 500 business owners and senior executives across business units are surveyed • The Q3 survey was conducted during June 2010 • Respondents are questioned about their expectations on relevant business parameters • Survey also captures respondent feedback on current business conditions

Composite Business Optimism Index • The Composite Index is calculated separately for the hydrocarbon and non hydrocarbon sectors • Within the non hydrocarbon sector the index is calculated: • for the six individual indices • for the five sub sectors within • For the hydrocarbon sector the Composite Index takes into account the aggregate behavior of the three individual indices

World Economic Outlook Real GDP (%) Global composite manufacturing & services PMI Source: IMF forecast, Q1 2010 are actual figures Source: JPMorgan and Markit • Global economy expected to grow 4.6% in 2010, up from April forecast of 4.2% • The US economy registered growth of 2.7% in Q1 2010 as against a revised GDP growth rate of 5.6% in Q4 2009. 2010 growth revised upward to 3.3% • The global composite PMI showed expansion (i.e. scoring > 50) for the eleventh consecutive month

Economy of Qatar Quarterly GDP2009 (QAR mn) • Qatar’s nominal GDP growth in Q4 2009 over the previous quarter was 9.7%; mining & quarrying sector grew 23.8% • Real GDP growth is expected to surge from 8.7% last year to 18.5% in 2010 • Higher oil & gas revenues will lead to a surge in current account balance from US$ 14 bn in 2009 to US$ 28 bn in 2010 Crude oil production Source: OPEC

Composite Business Optimism Indices Non Hydrocarbon Sector Hydrocarbon Sector • Business optimism in the non hydrocarbon sector lifted by improvement in all parameters • Surge in hydrocarbon optimism mainly due to an increase in level of selling prices expectation

Manufacturing Sector Global Manufacturing Purchasing Managers’ Index Manufacturing Sector: Composite Index Source: J P Morgan and market economics in association with ISM and IFPSM • The Global Manufacturing Purchasing Managers’ Index has shown growth for twelve consecutive months • Manufacturing sector BOI increase on the back of improvement in hiring outlook • BOI for Sales Volume drops but for New Order increases, suggesting mixed demand outlook in the third quarter

Construction Sector Construction sector: Composite Index • The global construction sector is witnessing a gradual upturn; sector is evolving as emerging markets continue to drive global recovery • Strong demand expected in the construction sector as BOI for Volume of Sales has jumped to 49 as against 26 in previous quarter • The BOI for Level of Selling Prices has stayed stable, reflecting recent correction in international commodities market

Trade & Hospitality Sector Retail sector growth in developed countries likely to remain slow whereas emerging markets are expected to witness rising retail sales in 2010 In Qatar, respondents are optimistic about the sector due to expectations of a huge increase in BOI for level of selling prices which moved to 26 from -5 in Q2 Demand levels are expected to improve modestly Trade & Hospitality sector: Composite Index

Transportation & Communication Sector Global transportation sector showing strong signs of revival amid recovery in trade sector and increased passenger traffic Qatar’s transport and communications sector has shown a substantial improvement on the back of strengthening demand and better pricing outlook Transport & Comm. Sector: Composite Index

Finance and Business Services Sector Global Services Purchasing Managers’ Index Finance & Business Services sector: Composite Index Source: JPMorgan and Markit • The Global Services PMI for the month of May stands at 56.3, showing expansion for the eleventh month in a row • Qatar’s finance & business services sector optimism rises on the back of better Selling Price outlook • Demand is expected to see modest improvement in third quarter

Oil & Gas sector Hydrocarbon Sector: Composite Index • Oil prices fell by 20% to USD 67 from their early May peak of USD 84 on concerns of Euro Zone debt crisis, but have risen since then to average USD 73 in June • Qatar’s hydrocarbon sector optimism has improved significantly in the third quarter primarily due to a higher BOI score for level of selling prices • Last quarter’s reading on BOI for Level of Selling Prices (-8) for the hydrocarbon sector is validated by the decline witnessed in oil prices during May

Other Highlights • Raw material costs is the leading concern for non hydrocarbon segment, 48% of the respondents have cited it as a factor which might affect their business • Availability of finance is a concern for 29% of the business units in non hydrocarbon sector • 31% of companies in the non hydrocarbon sector intend to investment in business expansion • For 50% of the companies in the hydrocarbon sector project delays could be a major factor which might impact their business in the third quarter

Conclusion • Business outlook improves in Qatar despite continuing debt troubles in Euro Zone • All sub sectors show an improvement in sentiments buoyed by robust demand outlook • Transport & logistics sector shows major improvement due to improved demand and consequently profitability outlook • Hydrocarbon sector displays surge in optimism levels on the back of expectations of rise in level of selling prices