Download

1 / 81

810 likes | 955 Views

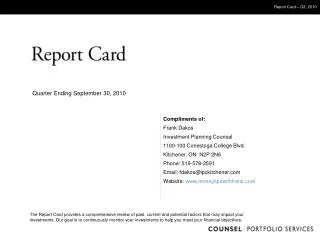

Report Card – Q3, 2010. Quarter Ending September 30, 2010. Compliments of: Frank Dakos Investment Planning Counsel 1100-100 Conestoga College Blvd. Kitchener, ON N2P 2N6 Phone: 519-578-2591 Email: fdakos@ipckitchener.com Website: www.moneytipswithfrank.com.

E N D

Report Card – Q3, 2010 Quarter Ending September 30, 2010 Compliments of: Frank Dakos Investment Planning Counsel1100-100 Conestoga College Blvd. Kitchener, ON N2P 2N6 Phone: 519-578-2591 Email: fdakos@ipckitchener.com Website: www.moneytipswithfrank.com The Report Card provides a comprehensive review of past, current and potential factors that may impact your investments. Our goal is to continuously monitor your investments to help you meet your financial objectives.

About This Report While this is a quarterly communiqué, the comments in this Report Card refer to the last three and 12 months. Market discussions are related to the indices and do not analyze or reflect your personal investments. Counsel Portfolio Services examines the performance and risk management of each mandate within your Counsel investment solution. We review the performance, risk management and overall effectiveness of each sub-advisor and underlying fund manager. Counsel investment solutions adopt a long-term approach to investing. Each portfolio solution is properly diversified to reflect an appropriate: Asset mix Geographic allocation Investment style mix A market-cycle typically refers to a period of between six and eight years. Please refer to the chart at the end of this presentation for further information on Counsel portfolio solutions. The benchmarks used for each Counsel investment solution can be found at the end of this presentation.

Agenda Market & Economic Overview What The Investment Specialists Say Review Of Counsel Investment Solutions Appendix: Counsel’s View Of The Investment Specialists

Global Stock Markets: Index Movements • Despite continued economic uncertainty globally, stocks rallied in most developed markets • North America and emerging markets led the recovery registering strong double digit gains since the crisis bottomed • China has had the weakest recovery in the year-to-date and since the March 9, 2009 low • Argentina, Mexico, Philippines, Thailand and Turkey hit record highs • Canada, India, Indonesia, Korea, Malaysia, Singapore and South Africa posted new bull market highs Performance is calculated using local currency. Data as at: September 30, 2010 Source: Morningstar Direct, Counsel Portfolio Services

National Debt Mounts . . . % of GDP$ billions 1) Ireland 1,267% $2,386 2) Switzerland 423% 1,338 3) United Kingdom 408% 9,087 4) Netherlands 365% 2,452 5) Belgium 320% 1,246 6) Denmark 298% 607 7) Austria 253% 832 8) France 236% 5,021 9) Portugal 214% 507 10) Hong Kong 206% 631 11) Norway 199% 548 12) Sweden 194% 669 13) Finland 189% 365 14) Germany 179% 5,208 15) Spain 172% 2,409 16) Greece 161% 553 17) Italy 127% 2,310 18) Australia 111% 891 19) Hungary 106% 208 20) United States 94% 13,454 Top 20 debtor nations as a percentage of GDP* * World’s 75 largest economies Source: CNBC, January 2010

How Are The Markets Doing? U.S. continues to trade below its fair value Stalled recovery in Europe Source: RBC Global Asset Management, The Global Investment Outlook, October 6, 2010.

How Are The Markets Doing? Emerging markets will have problems, valuations are high Canada reasonably valued Source: RBC Global Asset Management, The Global Investment Outlook, October 6, 2010.

Bank of Canada Rate Moves 9 rate cuts over 2008 & 2009 3 rate hikes in 2010 BOC Overnight Rate (%) as at October 19, 2010 5% 4% 3% 2% 1% 0% “The economic outlook for Canada has changed. The Bank expects the economic recovery to be more gradual than it had projected in July, with growth of 3.0 per cent in 2010, 2.3 per cent in 2011, and 2.6 per cent in 2012. This more modest growth profile reflects a more gradual global recovery and a more subdued profile for household spending.” – Mark Carney, Governor, Bank of Canada- 1.00% (as at October 19, 2010) 2007 2008 2009 2010 BOC raised the rate by 25 bps on June 1, July 20 and September 8 Source: Bank of Canada, as at October 20, 2010

Is Gold Entering A Bubble Phase? There is a possibility that Golds are entering the “blow-off” stage of a bubble Source: Picton Mahoney Asset Management., October 2010 Update

Why So Much Volatility Now? • Investors are holding their investments for far shorter time periods • This has led to increased trading activity and, therefore, increased volatility

Is This Recovery Like The Others? • Current market • Composite of previous recoveries • Chart shows that the current recovery is exactly like previous recoveries if viewed from the bottom of the crisis Source: RBC Global Asset Management, The Global Investment Outlook, October 6, 2010.

Bear Markets And Recoveries • Bear markets last an average of 13 months, and plunge an average of 28.0%, but all losses are restored an average of 19 months after the bear’s end • The most recent bear was unusually long at 17 months (but not nearly the longest), and the most severe since the Great Depression • Symmetry is evident in the recovery since March of 2009 • The profile is similar to the norm, but the scale of advance was the greatest of the post-war era • If this recovery had continued to track a “normal” cycle, losses in the bear market would have been recovered by September 2010 Source: RBC Global Asset Management, The Global Investment Outlook, October 6, 2010.

Catalysts For Improvement • Share Buybacks • M&A activity is increasing Source: RBC Global Asset Management, The Global Investment Outlook, October 6, 2010.

Global Mergers & Acquisitions Volume of Announced M&A Deals(1)($ trillions) 2009-10 Major Announcements/Closed Deals 5.0 4.5 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 $68 billion $41 billion $46 billion $31 billion $19.7 billion $3.2 billion merger 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 YTD Urge to merge . . . stymied in 2009 / Opportunities in 2010 (1) Includes announced deals (not withdrawn) >$25 million in value Source: Dealogic, June 30, 2010, USD

Catalysts For Improvement • Corporate balance sheets are strong – interest coverage at peak levels • Cash flow levels are at the highest they have been since 1960

Going Forward Global recovery will continue, despite financial turbulence 2015

Patience Is Rewarded • 1999 – 2009 was the worst decade on record, generating -5.7% Source: Sionna Investment Managers Inc., Canadian Equity Market Commentary, Third Quarter, 2010

Patience Is Rewarded • Dating from 1939, the average 10-year equity return was 10.8% in the periods following sub-par returns

Canadian Currency Performance The Canadian dollar moved closer to parity with the U.S. dollar - The CAD$ last traded above parity in April CAD$ appreciating due to continued weakness in the U.S. dollar, which has also led to higher commodity prices, and higher interest rates in Canada U.S. dollar weakened on fears of a double-dip recession and the continuous need for more stimulus, i.e. second quantitative easing Euro recovered from oversold levels, despite continued weakness in its economies CAD vs. Euro CAD vs. U.S. Dollar Source: Bank of Canada Source: Bank of Canada

Canada: Equities Versus Fixed Income Strong recovery in equities over the quarter, supported by strong corporate earnings, rising commodity prices and realization that a double-dip in the recovery is unlikely Equities recovering as fixed income offering paltry yields Falling interest rates over the last twenty years supported both equity and fixed income returns Interest rates cannot fall at the same pace and can in fact rise Expect lower returns from fixed income and equities relative to historical levels Long-term: Equities vs. Bonds Short-term: Equities vs. Bonds Source: Globe and Mail

Canadian Market Overview Investment Style Performance Market Cap Performance S&P TSX Completion Total Return S&P TSX 60 Total Return S&P TSX Small Cap Total Return MSCI Canada Growth Index MSCI Canada Value Index. Source: Morningstar Direct Source: Morningstar Direct • Financials, Energy and Materials sectors account for 75% of the TSX • Strong recovery in Materials, due to rising Gold price, mergers & acquisitions (e.g. Potash and BHP) • Technology was the weakest sector – influenced by concerns around the growth of Research in Motion • Financials weaker due to concerns around global regulation of banks

U.S. Market Overview September rally the strongest one for that month since 1939 Growth stocks outperformed value stocks dues of its lack of exposure to Financials and its higher weight in commodities All sectors did well: Materials, Energy and Technology performed better than the Financials in Q3 Financials affected by global banking sector regulations Small caps outperformed due to their heavier weight in Industrials and Energy Investment Style Performance Market Cap Performance S&P 500 Total Return S&P Mid Cap 400 Total Return S&P Small Cap 600 Total Return Russell 1000 Growth Index Russell 1000 Value Index Source: Morningstar Direct Source: Morningstar Direct

International Market Overview Growth stocks outperformed value stocks because of its lack of exposure to Financials and its higher weight in commodities Emerging markets, in particular commodity rich nations such as Brazil and Norway, provided the greatest gains Ireland continues to have financial problems and could possibly be the next Greece All sectors performed well: Materials, Energy and Technology did better than the Financials in Q3 Financials affected by global banking sector regulations Potential inflationary concerns were reflected in the performance of the Materials and Energy sectors – rising prices for Gold and Oil Investment Style Performance MSCI EAFE Growth MSCI EAFE Value Source: Morningstar Direct

On The Economic Recovery “U.S. corporations are producing almost as much as they did near the economic peak, but with much lower labor costs. It is possible that the recent improvement in the tone of the stock market will improve corporate confidence and kick-start capital spending programs.” – Picton Mahoney Asset Management Inc. “We believe there will continue to be a very slow, and at times, disjointed recovery, as consumers and governments repair their financial conditions. This recovery process will take years and will continue to require the coordinated actions of major central banks and governments, with the bulk of global growth coming from the rapidly developing economies of the BRIC nations." – Leon Frazer & Associates Inc. “We continue to view a slower, modest economic recovery as the most probable scenario over the next twelve months. There appear to be many areas of the economy where things appear to be held up in a fine balance. The economy appears to be walking many tightropes at once.” – Mawer Investment Management Inc.

On The Economic Recovery • “It is unlikely that the economy will revert anytime soon to contraction. Historically, recessions are precipitated by inflation-induced central bank tightening, asset-bubble implosions or a currency shock. These issues are behind us and, according to J.P. Morgan, four economic areas bear the brunt of U.S. recessions: housing, automotive sales, capital expenditure and inventory. Activity in all four areas is at, or below, the average trough level in prior recessions.” – Thornmark Asset Management Inc. • “Expect longer term period of below trend economic growth, earnings growth and wealth accumulation.” – Picton Mahoney Asset Management Inc. • “We believe that the global economy is currently in recovery mode, although the recovery will be uneven and choppy at times.” – Forum Securities Ltd.

Double Dip Recession? • “While the pace of the recovery has faltered, at this stage we view the likelihood of a double dip recession as low. We are encouraged by the recent improvement in both economic data and the stock market.” – Acuity Investment Management Inc. • “The “soft landing” versus “double dip” debate seems to be resolving in favour of the “soft landing” camp. We are not looking for acceleration in economic growth, but do expect a slow but upward trend to emerge.” – Picton Mahoney Asset Management Inc. • “We are not in the ‘double-dip camp. We expect a slow U.S. recovery and believe that the economy will create growth and jobs in 2011. The developing world markets can continue to grow without much inflationary pressure from the rest of the world.” – Marsico Capital Management, LLC

On Interest Rates “We do not view current interest rate levels as sustainable and feel that rates will eventually rise materially from these levels if the economic recovery continues.” – Leon Frazer & Associates Inc. “The interest rate backdrop remains favourable, as most major central banks are holding interest rates at rock bottom levels. Even the Bank of Canada has signaled a pause in its modest rate hike cycle as it assesses conditions in the U.S. and domestically.” – Acuity Investment Management Inc. “Administered interest rates in North America are expected to remain near current levels through the remainder of the year. In the new year the BoC should resume rate hikes as Canadian economic conditions exceed those of the U.S.” – Thornmark Asset Management Inc. “Compared to market expectations in the spring, the probability of significant rate increases by the Bank of Canada over the next 6-12 months has diminished.” – TD Asset Management Inc. “For 2011, we anticipate the Bank of Canada will increase rates again, probably by more than what is implied by market participants.” – Montrusco Bolton Investments Inc. “Eurozone shocks, fiscal drag and central banks’ knowledge of the mistakes of 1937 should keep rates at rock bottom levels at least into 2011 and until growth establishes firm root.” – RBC Global Asset Management Inc. “Even, after recent plunge, yields reflect a ‘reasonable’ view of the future, but total returns seem unlikely to exceed low single digits.” - RBC Global Asset Management Inc.

On Inflation • “Inflation data remains encouraging. This will ultimately be good for economic growth, but it makes it improbable that short rates will continue to stay at 1% for much longer.” – Montrusco Bolton Investments Inc. • “Inflation is expected to be benign until 2012, at which point normal cyclical inflation pressures will begin to build.” – Thornmark Asset Management Inc. • “Inflation continues to be non-existent when measured by official agencies. However, it is hard to find many things in our day to day lives that cost less than they did a year ago. We continue to believe that as the economic recovery continues, inflation has the potential to increase to moderate or even severe levels given the amount of stimulus in the economy. We continue to believe the recovery will be very slow so inflation is not a current concern.” – Leon Frazer & Associates Inc. • “Along with our forecast for subdued growth, we expect inflation and interest rates to generally remain low. We also expect investors to continue to look for higher growth in places like emerging markets. However, valuations in these markets already incorporate this.” – Mawer Investment Management

On Currency “Improving commodity prices will help boost the Canadian dollar.” – Acuity Investment Management Inc. “No material change in the CAD/USD exchange rate is anticipated in the short to mid-term. The CAD will fluctuate in a trading range around par.” – Montrusco Bolton Investments Inc.

On Commodities “The is a possibility that Gold is entering the “blow off” stage of a bubble.” – Picton Mahoney Asset Management Inc. “Commodity prices continue to be volatile and inversely correlated with the U.S. dollar. Bulk commodities continue to be demanded by the growing economies of developing nations in increasing quantities.” – Leon Frazer & Associates Inc. “The Canadian equity market will continue to be positively impacted by the renewed confidence in the global demand for basic materials and the resulting increases in the underlying commodity prices.” – Montrusco Bolton Investments Inc. “With global economic leadership from emerging economies and a generally coordinated global economic expansion, demand for commodities will remain high, particularly while the US$ is in decline. Therefore, we expected commodity prices to remain at current-to-higher levels (with the exception of gold). Towards 2012 and beyond as inflation pressure mount, expect commodity prices to reaccelerate to higher levels.” – Thornmark Asset Management Inc.

On Market Volatility “We expect stocks to continue their rally, but within the context of a longer term trading range.” – Picton Mahoney Asset Management Inc. “Investors seem to have become hypersensitive to the potential for adverse events to occur in the economy and in the stock markets. It certainly doesn’t help that the 10 year compound annual growth rate of the S&P 500 index has recently experienced the second worst bear market since 1880. We still believe a substantial ‘wall of worry’ exists that can help sustain further gains in equities. – Picton Mahoney Asset Management Inc. A market filled with volatility and one hundred reasons why it should not go up, historically has been an excellent stock picker’s market. It seems that there has never been as much uncertainty and confusion concerning the macro picture. – Dreman Value Management Inc.

On Market Outlook “Emerging markets are expected to carry more of the economic load this time.” – Picton Mahoney Asset Management Inc. “Investors can generate solid returns in a tepid economic recovery if the recovery maintains itself and if valuations are attractive. We believe both of these conditions exist today.” – Picton Mahoney Asset Management Inc. “We are cautious about the next six to 18 months as stimulus continues to be withdrawn and taxes go up. We continue to believe that North America is in a slow recovery that will take years.” – Leon Frazer & Associates Inc. “The biggest opportunity we can see going forward is the eventual retrenchment of the capital that rushed out of equity markets and into bonds and cash over the past two years. With 10 year interest rates at all-time lows, and quality corporate balance sheets in excellent shape, and a continued economic recovery we can make the case for dividend paying investments to lead a sustainable stock market recovery.” – Leon Frazer & Associates Inc. “We feel with the stabilization of the U.S. economy, a possible second round of quantitative easing by the Federal Reserve, and demand for commodity from buoyant emerging market countries, Canadian equities should perform better than the rest of the world.” – PanAgora Asset Management Inc.

On Market Outlook • “We continue to believe we are in the 10th year of a sideways market, which usually lasts a minimum of 15 years.” – Sionna Investment Managers Inc. • “Modest recovery/mild inflation remains our base case. Threat of a double dip is valid, but unlikely. The prospect for a protracted period of sub-par growth is becoming a comfortable consensus.” – RBC Global Asset Management Inc. • “Recent rally alleviated prior ‘oversold’ condition in markets, so a period of consolidation/correction is now a growing possibility. But, barring double dip for economy, stocks should ultimately produce superior intermediate/long-term returns as risk premiums normalize and as earnings power to the upside.” – RBC Global Asset Management Inc. • “Prospect of many years of range bound trading cannot be ignored as global economy gradually crawls back from the bust. In that environment full recognition of equity market potential will be delayed and tactical trading will be key to success.” - RBC Global Asset Management Inc.

Counsel Balanced Portfolio * Target asset allocation weights adjusted in October 2009, following annual review of Counsel portfolios. ** In February 2010, the target asset allocation weights were adjusted following merger of Counsel Select America (U.S. equities mandate) into Counsel U.S. Growth. Counsel U.S. Value and Counsel U.S. Growth were added as new underlying funds to the Portfolio. Monthly allocation may not add up to 100% as net working capital has been excluded. This Portfolio is managed using a multi-manager process. The current sub-advisor or underlying mutual fund managerfor each mandate is listed beside the mandate for which it provides portfolio management / sub-advisory services. This Portfolio invests in underlying mutual funds (which may be managed by Counsel) currently sub-advised by the sub-advisors listed beside each investment mandate. For information on the underlying funds, please refer to the prospectus, which is available on our website at www.counselservices.com or on the SEDAR website at www.sedar.com.

Counsel Balanced Portfolio Effective Top 10 Sector Allocation Effective Asset Class Mix Effective Geographic Mix

Counsel Balanced Portfolio Positive and negative attribution for Q3, 2010 Positive and negative attribution for the 12 months ended 30 September, 2010 + Positive attribution to overall Portfolio, reflecting that the mandate outperformed its relative benchmark on a gross returns basis. - Negative attribution to overall Portfolio, reflecting that the mandate underperformed its relative benchmark on a gross returns basis.

Counsel Fixed Income Effective Investment Mix Effective Bond Maturity

Counsel Canadian Value Effective Asset Class Mix Effective Top 10 Sector Allocation

Counsel Canadian Growth Effective Asset Class Mix Effective Top 10 Sector Allocation

Counsel U.S. Value Effective Asset Class Mix Effective Top 10 Sector Allocation