Download

1 / 7

70 likes | 138 Views

CP 58 is not a tax form. This is a profit and loss statement that shows income from incentives, allowances, bonuses, etc. For agents, dealers and distributors, similar to the EA form received by the employee.<br>The SST (Sales and Service Tax) is levied on taxable supplies of goods and services made in the course of or for the purpose of developing a business in Malaysia by a taxpayer. It is imperative for invoice format SST registered companies to issue the correct and correct tax invoice to the client. It acts as the primary evidence in support of the provisional tax credit claim. It is obligatory to issue a tax invoice, which separately indicates the amount of the accrued value added tax and the cost of supplies.<br>

E N D

What is CP58 Form? • CP 58 is not a tax form. This is a profit and loss statement that shows income from incentives, allowances, bonuses, etc. For agents, dealers and distributors, similar to the EA form received by the employee.

Who are required to file CP58 form? • The Inland Revenue Board of Malaysia (IRBM) states that if a company pays an agent more than RM5,000 in cash or non-cash benefits during a calendar year, they must prepare a CP58 form for each agent. These forms do not need to be sent to the tax office, but if the tax office requires all the information on the benefits paid, the company must provide all the information on the incentive payments, including remunerations of less than RM5,000.

What rewards must be reported? • Remuneration to an agent for achieving results is generally divided into two categories: monetary rewards and non-monetary incentives. • Cash rewards include base markups, commissions or bonuses. If the company provides cash incentives to the agent, it must indicate the actual amount paid on a CP58 form. • Material non-cash benefits include benefits, travel packages, tickets, accommodation, car, home, and so on. For non-cash consideration, the company must prepare a CP 58 form based on actual costs.

When is the due date to provide CP 58 form? • The CP 58 must be submitted to the agent, dealer or distributor no later than March 31st of the year immediately following the year in which the above incentives are paid.

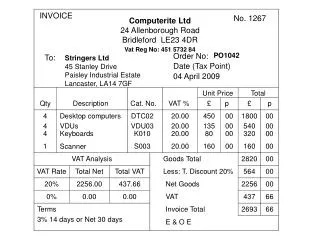

What is SST Invoice? • The SST (Sales and Service Tax) is levied on taxable supplies of goods and services made in the course of or for the purpose of developing a business in Malaysia by a taxpayer. It is imperative for invoice format SST registered companies to issue the correct and correct tax invoice to the client. It acts as the primary evidence in support of the provisional tax credit claim. It is obligatory to issue a tax invoice, which separately indicates the amount of the accrued value added tax and the cost of supplies.

There are TWO TYPES of tax invoices: • Complete tax invoice • Simplified tax invoice A simplified tax invoice is commonly used by retailers who issue a huge number of invoices to end consumers on a daily basis by Malaysia invoice requirements, such as supermarkets, restaurants, petrol kiosks and other points of sale. This can be an invoice, receipt, or a voucher with the required information on a simplified tax invoice or SST invoice template. A simplified invoice like a sample SST invoice without the name and address of the recipient can also be used to apply for input tax. However, the maximum tax payable is MYR 30. If the recipient wishes to claim the full amount of input tax (more than MYR 30.00), a full tax invoice will be more appropriate as it includes the recipient's name and address.