Work Breakdown Structure

Work Breakdown Structure A hierarchical system which sub-divides larger elements of the project into smaller elements called “work packages”. C OST C ONTROL Project cost control begins with the preparation of the cost estimate and the construction budget.

Work Breakdown Structure

E N D

Presentation Transcript

Work Breakdown Structure • A hierarchical system which sub-divides larger elements of the project into smaller elements called “work packages”.

COST CONTROL • Project cost control begins with the preparation of the cost estimate and the construction budget. • The information that is generated for estimating purposes can be in terms of productivity rates, unit costs, or both. • Small contractors frequently work in terms of unit costs while large contractors base their estimating on productivity rates

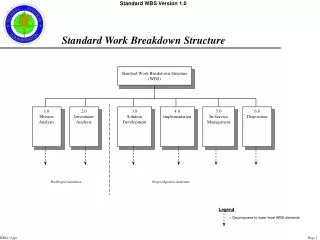

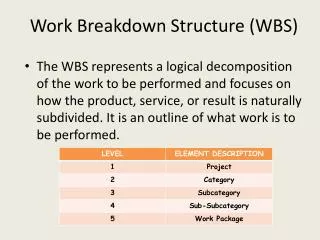

WORK BREAKDOWN STRUCTURE • Work Breakdown Structure (WBS) requires the project to be divided and subdivided into smaller parts • The smallest unit of the WBS is the work package, which called a contract package if the work is contracted out.

WORK BREAKDOWN STRUCTURE (cont.) • It is necessary that the scope of the work for each work package be described in relation to the work to be done in the other work packages. • Work packages should be defined in terms of design, construction methods, and completion requirements, with associated performance dates

WORK BREAKDOWN STRUCTURE Project must be structure into small elements that are: 1. Manageable • Specific authority and responsibility can be assigned. 2. Independent • With minimum interfacing or dependence on other elements. 3. Measurable • In terms of progress.

Characteristics of Work Package 1. Represents units of work at the level where the work is performed. 2. Clearly distinguish one work package from all others. 3. Contains clearly defined start and end dates that are representative of physical accomplishment. 4. Specifies a budget in terms of dollars, man-hour or other measurable units. 5. Limits the work to be performed to relatively short periods of time to minimize the work in progress.

The Project Cost System Objectives of Establishing Project Cost System. 1. Keep the construction costs of the project within the established budget, 2. Develop labor and equipment productivity information for estimating the cost of future work

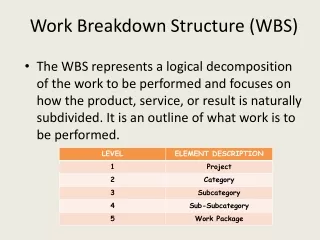

Cost Code Project Number Area Code Work Type Code Distribution Code • Cost Code for stripping concrete formwork for bridge deck (Labor). 9708B 05 03157.20 3

Project Number 9708B05 03157.20 3 • Eighth project in 1997 (Bridge)

Area Code 9708B0503157.20 3 • Geographic location OR • Associate Field Cost to Specific supervisor or Management

Work Type Code 9708B 0503157.203 03 Concrete 0315 Concrete Formwork 03157 Wood Concrete Formwork 03157.20 Wood Concrete Formwork for Deck 03157.30 Wood Concrete Formwork for Abutment

Distribution Code 9708B 05 03157.203 1. Total 2. Material 3. Labor 4. Equipment 5. Sub-Contract

COST CODES • Each account of a contractor's accounting system is assigned its own code designation as a means of identification and classification. • The most widely used cost codes are CSI (Construction Specifications Institute) and UCI (Uniform Construction Index).

Cost Code and Cost Control • All items of expense are charged to the project where they are incurred. • "General" or "miscellaneous" cost accounts should not be used, is poor practice, and should be avoided. • The cost code is to serve its basic purpose, it must be understood and used consistently by all company personnel.

COST ACCOUNTINGREPORTS • Labor and equipment summary cost reports must be prepared often enough so that excessive costs can be detected while there is time to do something about them. • Cost report intervals are a function of the project size, nature of the work, and the type of contract involved. • There must be a balance between the cost of generating the reports and the value of the management information received

COST ACCOUNTINGREPORTS (cont.) • Cost reports are frequently prepared daily on complex projects involving multiple shifts • Most contractors match their cost control system to their payroll periods and to their time-monitoring system.

LABORAND EQUIPMENT COSTS • The job costs associated with materials, subcontracts, and non-labor items of project overhead are of a reasonably fixed nature. • Labor and equipment costs have considerable uncertainty and fluctuate substantially during the construction period.

LABORAND EQUIPMENT COSTS (cont.) • Contractor can control labor and equipment to some extent, and require constant management attention • Detailed cost accounting methods must be used with labor and equipment expenses if effective management control over them is to be obtained.