Download

1 / 14

140 likes | 212 Views

Learn the essentials of accounting, including balance sheets, income statements, debits, credits, journalizing, ledger posting, and the double-entry system. Explore trial balances, T-accounts, and more in this detailed tutorial.

E N D

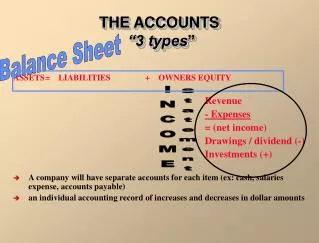

THE ACCOUNTS “3 types” Balance Sheet ASSETS = LIABILITIES + OWNERS EQUITY Revenue - Expenses = (net income) Drawings / dividend (-) Investments (+) • A company will have separate accounts for each item (ex: cash, salaries expense, accounts payable) • an individual accounting record of increases and decreases in dollar amounts INCOME Statement

Debit = left side Credit = right DR CR DEBITS AND CREDITS

Title of Account Left or debit side Right or credit side Debit balance Credit balance ILLUSTRATION 2-1: BASIC FORM OF ACCOUNT (T-account) • In its simplest form, an account consists of 1. the title of the account, 2. a left or debit side 3. a right or credit side. • The alignment of these parts resembles the letter T, and therefore the account form is called a T account.

Account Form Tabular Summary Cash Cash Debit Credit $15,000 - 7,000 15,000 7,000 1,200 1,200 600 1,500 1,500 900 - 600 600 200 - 900 - 200 - 250 Balance ILLUSTRATION 2-2TABULAR SUMMARY COMPARED TO ACCOUNT FORM 8,050 250 1,300 600 - 1,300 $8,050

DEBITING AN ACCOUNT Example: The owner makes an initial investment of $15,000 to start the business. Cash is debited and the owner’s Capital account is credited.

CREDITING AN ACCOUNT Example: Monthly rent of $7,000 is paid. Cash is credited and Rent Expense is debited.

DEBITING AND CREDITING AN ACCOUNT Example: Cash is debited for $15,000 and credited for $7,000, leaving a debit balance of $8,000.

Assets Liabilities Equity DOUBLE-ENTRY SYSTEM MUST EQUAL • Value of debit entry the value of the credit entries in every transaction • Thus, total debits will always equal the total credits accounting equation will always stay in balance.

Liabilities Assets Owner’s Equity Owner’s Capital Owner’s Drawings Assets Liabilities Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. + - - + - + Revenues Expenses Dr. Cr. Dr. Cr. - + + - ILLUSTRATION 2-7DEBIT/CREDIT RULES AND EFFECTS, and Normal act. Balances = + = + - + - normal balance + -

JOURNAL LEDGER JOURNAL ILLUSTRATION 2-9THE RECORDING PROCESS 1. Analyze each transaction. 2. Enter transaction in a journal. 3. Transfer journal information to ledger accounts.

ILLUSTRATION 2-10TECHNIQUE OF JOURNALIZING What is significant about all of the circled info on the General Journal below? J1 GENERAL JOURNAL Date Account Titles and Explanation Ref. Debit Credit 2002 Sept. 1 Cash 15,000 M. Doucet, Capital 15,000 Invested cash in business. 1 Equipment 7,000 7,000 Cash Purchased equipment for cash.

ILLUSTRATION 2-14POSTING A JOURNAL ENTRY In the ledger, enter in the appropriate columns of the account(s) debited the date, journal page, and debit amount shown in the journal and the account number to which the journal was posted.

THE TRIAL BALANCE • A list of accounts and their balances at a given time. • Shows that debits and credits are equal after posting. • May uncover errors in journalizing and posting. • The procedures for preparing a trial balance consist of 1. listing the account titles and their balances, 2. totaling the debit and credit columns, and 3. proving the equality of the two columns. What problems and limitations are there with a trialbalance?

ILLUSTRATION 2-28A TRIAL BALANCE PIONEER ADVERTISING AGENCY The total debits must equal the total credits. Notice the order of the accounts BS then IS accounts Trial Balance October 31, 2002 Debit Credit Cash $ 15,200 Advertising Supplies 2,500 Prepaid Insurance 600 Office Equipment 5,000 Notes Payable $ 5,000 Accounts Payable 2,500 Unearned Revenue 1,200 C. R. Byrd, Capital 10,000 C. R. Byrd, Drawings 500 Service Revenue 10,000 Salaries Expense 4,000 Rent Expense 900 $ 28,700 $ 28,700