Download

1 / 40

550 likes | 1.3k Views

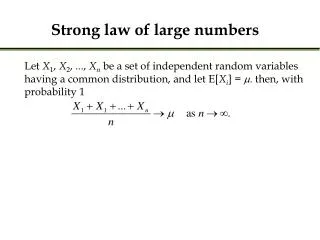

Strong law of large numbers. Let X 1 , X 2 , ..., X n be a set of independent random variables having a common distribution, and let E[ X i ] = m . then, with probability 1. Central Limit Theorem.

E N D

Strong law of large numbers Let X1, X2, ..., Xn be a set of independent random variables having a common distribution, and let E[Xi] = m. then, with probability 1

Central Limit Theorem Let X1, X2, ..., Xn be a set of independent random variables having a common distribution with mean m and variance s. Then the distribution of

Conditional probability and conditional expectations Let X and Y be two discrete random variables, then the conditional probability mass function of X given that Y=y is defined asfor all values of y for which P(Y=y)>0.

Conditional probability and conditional expectations Let X and Y be two discrete random variables, then the conditional probability mass function of X given that Y=y is defined asfor all values of y for which P(Y=y)>0.The conditional expectation of X given that Y=y is defined as

Let X and Y be two continuous random variables, then the conditional probability density function of X given that Y=y is defined asfor all values of y for which fY(y)>0.

Let X and Y be two continuous random variables, then the conditional probability density function of X given that Y=y is defined asfor all values of y for which fY(y)>0.The conditional expectation of X given that Y=y is defined as

The sum of a random number of random variables Example: The number N of customers that place orders each day with an online bookstore is a random variable with expected value E[N].

The sum of a random number of random variables Example: The number N of customers that place orders each day with an online bookstore is a random variable with expected value E[N]. The number of books Xithat each customer i (i = 1, 2, ..., N) purchases is also a random variable E[Xi] with expected value E[Xi].

The sum of a random number of random variables Example: The number N of customers that place orders each day with an online bookstore is a random variable with expected value E[N]. The number of books Xithat each customer i (i = 1, 2, ..., N) purchases is also a random variable E[Xi] with expected value E[Xi].What is the expected value of the total number of books Y sold each day? What is its variance?

The sum of a random number of random variables Example: The number N of customers that place orders each day with an online bookstore is a random variable with expected value E[N]. The number of books Xithat each customer i (i = 1, 2, ..., N) purchases is also a random variable E[Xi] with expected value E[Xi].What is the expected value of the total number of books Y sold each day? What is its variance? Assume that the number of books are independent and identically distributed with the same mean E[Xi]=E[X] and variance Var[Xi]=E[X] for i=1,..., N. Also assume the number of books purchased per customer is independent of the total number of customers.

If N is Poisson distributed with parameter l, the random Y = X1+X2+...+ XN is called a compound Poisson random variable

Computing probabilities by conditioning Let E denote some event. Define a random variable X by

Computing probabilities by conditioning Let E denote some event. Define a random variable X by

Computing probabilities by conditioning Let E denote some event. Define a random variable X by

Example 1: Let X and Y be two independent continuous random variables with densities fX and fY. What is P(X<Y)?

Example 1: Let X and Y be two independent continuous random variables with densities fX and fY. What is P(X<Y)?

Example 1: Let X and Y be two independent continuous random variables with densities fX and fY. What is P(X<Y)?

Example 1: Let X and Y be two independent continuous random variables with densities fX and fY. What is P(X<Y)?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?

Example 2: Let X and Y be two independent continuous random variables with densities fX and fY. What is the distribution of X+Y?