Download

1 / 26

260 likes | 518 Views

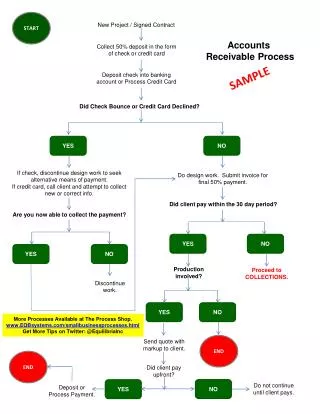

Fiscal Policy Training Accounts Receivable, FI0305 Laura Foltz Business Affairs What is A/R? Debts owed to university For goods or services University has sold or provided to customers Short term Expected to be paid in 30 days No interest charge Reconciling Balances

E N D

Fiscal Policy TrainingAccounts Receivable, FI0305 Laura Foltz Business Affairs

What is A/R? • Debts owed to university • For goods or services • University has sold or provided to customers • Short term • Expected to be paid in 30 days • No interest charge #1

Reconciling Balances • Individual account balances • Control balance • Perform aging periodically • Review past due accounts • Reconcile individual accounts to control balance periodically #1,2

Invoicing • Pre-numbered invoices • Invoice number accounted for periodically #2

Cashiers should NOT • Handle disputed items • Approve refund of credit balances and credit adjustments • Where possible, the duties of the accounts receivable bookkeeper and the cashier should be separated. • A/R write-offs should be approved by an employee who does not handle cash receipts. #2

Billing and Collections • Regular billings - all customers on account. • Statements or invoices mailed monthly • Students at end of term, monthly if necessary • Written routine collection procedures • Special reminders/collection letters mailed for all past due accounts 2,3

Delinquent Accounts • Customers – Services discontinued • Students – Holds placed on account • Release of grades and records • Registration • Certain debts can be cancelled if student dies during enrolled term • Delinquent amounts over $2,000 • submit a list of accounts to General Counsel's Office for consideration. #3, 17, 18

External Collection Agencies • Six Months & $50 or more • Referred to Business Affairs • If not used, justification on write-off request #3

Allowance for Doubtful Accounts • Aging of Accounts Receivable. • Individual customer account balances categorized by length of time outstanding • Business Affairs estimates the relative uncollectibility for each category based on past experience. • The estimated uncollectible amounts in each category are totaled to determine the total allowance. #4

Year End Aging Categories • 0-30 days • 31-90 days • 91-180 days • 181+ • Semester - unpaid extensions of student fees #5

Year End Reporting • Allowance recorded (Business Affairs) • Departmental account is charged • List of A/R as of June 30 to Business Affairs • Aging of A/R must accompany list #4,5

Returned Checks • Automatically debited to University bank account. • The checks are returned to Business Affairs • Appropriate accounts receivable returned checks fund is charged #6

Returned Checks • Detailed record maintained • If transferred for collection, the responsible office must obtain and keep a transfer receipt #7

Returned Checks - Collected • Official receipt written • Separate receipt book for high volume areas • Deposited to the university's bank account • Credited to A/R initially charged • $30.00 minimum service charge • Service charges credited to an income fund #8,9,10,11

Returned Checks • Reconcile checks on hand to amount on university official records • Appendix A - sample reconciliation sheet • Write off uncollectible returned checks • Keep returned checks even if person presents other payment #12.13, 20

Uncollectible Accounts • After above collections efforts • Department head ensures due diligence is collecting A/R • Department head requests write off #14, 15

Documentation Initiating Write Off • Documentation of collection activity • Copies of invoices • Special collection letters • Notes from telephone contacts • Returned Mail #15, 20

Submit to Business Affairs • T-35 Form completed by Department head • Request form includes justification • Itemized list of uncollectible accounts • Original returned check, if applicable

Writing Off A/R • Chief business officer (or designee) signs FORM T-35 andforwards to Controller's Office • Copy is returned to department for files • The Controller's Office records journal entry

Writing Off A/R • The Controller's Office prepares annual summary of write-offs for treasurer, Audit and Consulting Services, chief financial officer, and the TN Dept. of Finance and Administration. • Audit and Consulting Services will use this summary to perform periodic audit of accounts receivable write-offs.

Justification for Write-off • NOT accounts of students currently enrolled • Collection agency returns as uncollectible. • Bankruptcy of debtor legally declared • Credit balances under $50 & inactive for year • Over 3 years old & billed regularly • Owed by companies no longer in business • Judgments over six months old. 16

Justification for Write-off • Under $50 and over 6 mos. old and either • Returned for incorrect address (or) • Billed at least 3 times. (Generally, the third billing should include a special collection notice. ) • Amounts under $2 (DR or CR) of any age • regardless of whether from a student who is currently enrolled. • Other reasons considered - case-by-case basis #16

Bankruptcy of Debtors • Notification from bankruptcy court that debtor filed for bankruptcy- immediately cease all collection efforts • Send all bankruptcy forms to Business Affairs

Bankruptcy of Debtors • Student loans or other debts representing an obligation to repay amounts received or credited for educational purposes are not dischargeable in bankruptcy unless the court finds that exception from discharge will impose an undue hardship on the debtor. #19

Bankruptcy of Debtors • Parking and library fines are not dischargeable by the court under either Chapter 7 or Chapter 13. • If a discharge notice is received from the bankruptcy court, the debtor is no longer liable and the debt should be cleared from the debtor's record. However, for nondischargeable debts as described, collection efforts may resume after the debtor's discharge in bankruptcy. • Collection efforts may also resume if the case is dismissed. #19

Bankruptcy of Debtors Business Affairs handles all bankruptcies.