Download

1 / 19

190 likes | 198 Views

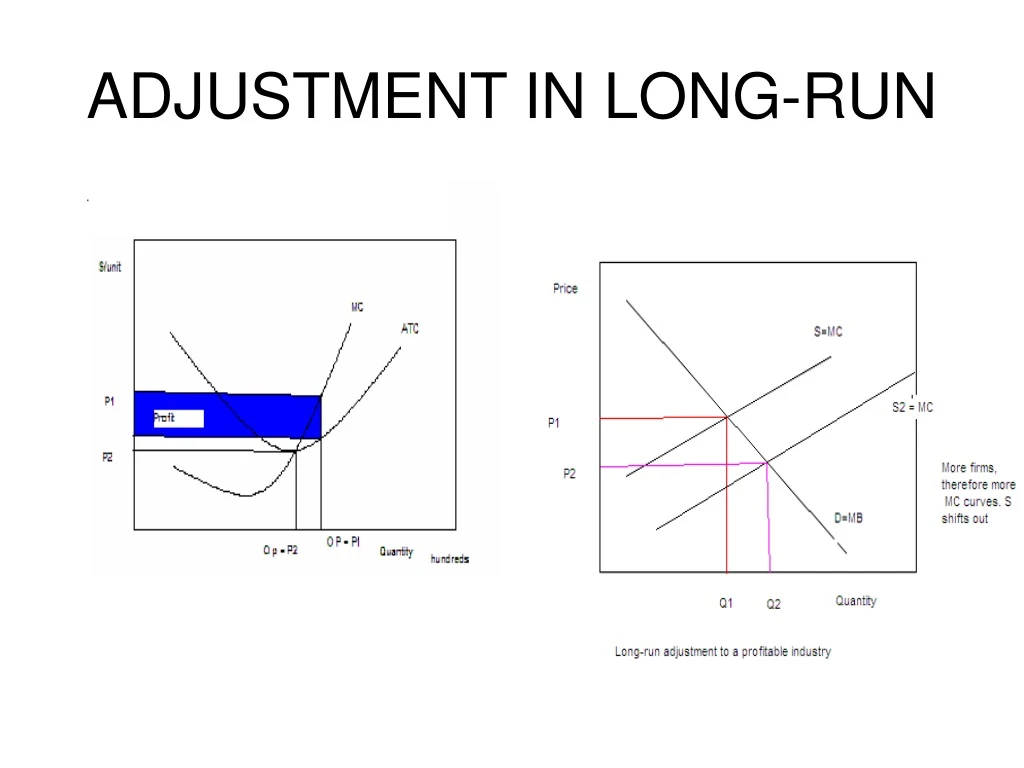

ADJUSTMENT IN LONG-RUN. ADJUSTMENT IN THE LONG-RUN. RISE IN DEMAND CAUSES INDUSTRY EXPANSION. LONG RUN ADJUSTMENT AFTER A PERMANENT RISE IN DEMAND. LONG RUN EQUILIBRIUM. EFFICIENCY. PRODUCTIVE EFFICIENCY.

E N D

EFFICIENCY • PRODUCTIVE EFFICIENCY. • In the long run the industry always returns to the equilibrium at which price equals minimum ATC, so costs are as low as possible. • ALLOCATIVE EFFICIENCY • Price (willingness to give up) always equals MC (what is necessary to give up).

Adjustment to technological change • If other firms do not have access to the technology because the technique is patented, the innovating firm can continue to make profits. However, the firm would likely make still more money selling the new technology to the other firms. • If other firms have access to the new technology, firms will adopt it in order to also make the extra profits. • As firms adopt the new technology they expand production and firms enter the industry because profits are possible with the new technology.

Long run adjustment to technological change • When the economy adjusts to the lower costs of the new technology, all firms in the industry are forced to use it. • If they fail to adopt the new technology, their costs will be too high and they will make losses. In the long-run they will go out of business.

SUMMATION OF ADVANTAGES • In a perfectly competitive industry, the right mix of goods are produced at the lowest possible price. • Firms earn all they need to stay in business, and no more. • Strong incentives exist to respond to changes in demand and to changes in technology. • Industry is dynamic and has a strong bias towards improving productivity

SUMMATION OF DISADVANTAGES • Only the costs that are paid by the firms are minimized. If the lowest cost technique causes harm to the environment, animals or workers, firms will be forced to adopt the technique or go out of business. • Benefits of the product not enjoyed by the consumer will also be ignored by the market.

Life is tough in competitive industries • Note that firms in competitive industries have to work hard to survive. They must always be on their toes. • In industries that hold a declining share of our economy – agriculture, for example – competitive markets will steadily force firms out of the industry. • Demand will tend to fall, relative prices will tend to fall, and firms will always be struggling, with many losing the battle. • Farmers have fallen from 40% to 2% of our population. They have been driven out of the market by falling relative prices. • The public benefits because now farmers kids and grand kids are the factory workers, computer technicians, doctors, lawyers, school teachers who produce goods we need more than we need more food. The farmers forced out of business are often pretty unhappy about it at the time.

Farmers have good press • Note that many farmers control very valuable land and capital. Some lose it through bankruptcy. Many others see that alternative opportunities are more attractive, sell their assets, and have a nice nest egg for starting a new life. • When we regulate industries such as dairy farms to give farmers a good income, we are often helping people with hundreds of thousands of dollars in assets while forcing the poor to pay much more for their kids’ milk than it costs to produce.

Regulation of the dairy industry • Canada imposes quotas on dairy production. Each farmer must own a quota to be able to produce milk. • The Dairy industry regulates the price of milk, so that the quantity demanded equals the quantity produced under quota.

Results for Farmers • Quotas can be bought and sold on unregulated markets. They are an artificial form of property. That is, they are an asset, like the farmer’s land or herd of cows, but they add nothing to the physical ability to produce milk. • In order to start farming, farmers must acquire quota. If they buy quota on the open market, they will find that the price is bid up until it reduces the profits created by regulation to zero. • These farmers will just break even, as if the industry was unregulated.

End Result • Many farmers have borrowed to acquire quota, or regard quota as an asset they will sell to provide an income in their retirement. • If the industry is deregulated (as the World Trade Organization or other pressures to free trade may require) quotas will have no value. • Farmers will either suffer severe economic loss, or the government will have to step in to buy up the quota, at a substantial cost to the tax payers.