Download

1 / 0

0 likes | 114 Views

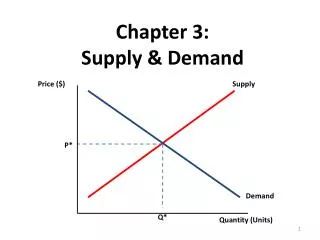

Explore the relationship between price and quantity demanded in economics, as defined by the Law of Demand. Learn how consumers' willingness and ability to purchase goods change with varying prices.

E N D