Download

1 / 21

210 likes | 349 Views

Supplier Cost Assessment. By Dave Reuss B.Sc, M.Sc, C.Eng, F-ACostE. Background. When a customer (an OEM) sends out ‘Requests for Quotation’ to Suppliers, rather than relying on three-quote system, how many of them use ‘Quotation Analysis Forms’?

E N D

Supplier Cost Assessment By Dave Reuss B.Sc, M.Sc, C.Eng, F-ACostE

Background • When a customer (an OEM) sends out ‘Requests for Quotation’ to Suppliers, rather than relying on three-quote system, how many of them use ‘Quotation Analysis Forms’? • Do they understand the power it can give to the Buying team, assisting negotiation? • How many first tier Suppliers flow the principal of the QAF onto their supply-chains? • Clearly there is an aversion by some, in disclosing such detailed breakdown of their costs. Trouble is that these are often the suppliers who either do not understand their own true costs or who are blind to recognising the benefits of working collaboratively with their business partners in this way. • Benchmarking exercises have often shown that those who join-in and learn, benefit far more in the long run than those who choose not to take part. • This presentation will show examples of Quotation Analysis Forms from a generic point of view and discuss the benefits of their use.

Supplier Cost Analysis “Getting the right deal involves more than simply asking a supplier to quote. The quotation has to be properly understood” Sourcing Decision Support Inc. “Its about getting Best value for money” Common sense

Quotation Analysis Form… >8 different user’s form seen over years • Component Cost Breakdown… x1 • Proposal Submission Sheet… x1 • Component Cost Worksheet… x1 Essentially all doing the same thing !

What a QAF is! • … “Quotation Analysis Form” – what the Supplier fills in. • Customer’s preferred pro-forma when receiving Supplier bids on Parts, Assemblies, or Services. • Helps Customers to compare bids from different sources. • ‘Supplier Selection’ aide. • Helps Buyers to get to the ‘True’ cost drivers: • Commercial and Technical… by looking in ‘detail’ • Helps Vendors to explain why parts cost what they do. • Helps both parties understand and communicate. What a QAF is not: • It’s not a project costing tool, or LCC tool, • Not high level Parametric algorithm based (more ABC) • It’s not the only tool in the box,

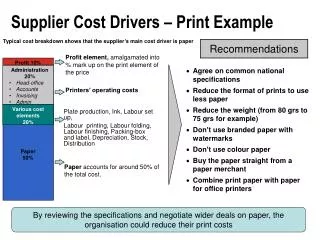

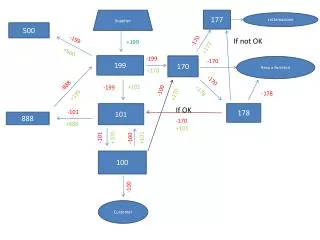

Logistics costs SG&A + Profit Manufacturing Process Costs Summary: Recurring, NRC, Profit & History Purchased Parts & Materials Non-Recurring Costs So what does one look like? • Typically spread-sheet based, • Summary sheet, • Supplier name, • Part description & P/No. • Listing of: • Procured parts, • Raw Materials, • Processing costs, • Tooling costs, • Other costs & Margin (profit), • Logistics costs. • Assumptions (validity, PO qty)

generic So what do others look like? • Reviewed a reasonable number of different QAF’s as applied within Automotive and Aerospace manuf’g industry. • Conclusion: • They all do about the same, • Only one from seven was different. • In very similar format, • Very similar terminology, • Virtually same content and scope.

Wheel of Transparency No trust Trusting Collaborative Confrontational Strategic Transactional • Some insist that a Supplier QAF be completed prior to all contract negotiations. • Some only want them being tabled at the negotiation. • Others believe it essential that you have your own solid estimation available before entering any negotiation: • Establishing their own view on what is value for money, or • Working out what their most desirable out-come (MDO). • Not everyone uses QAF’s: • They may have supplier agreed models in place, • Others because they have yet to here of them or understand their benefits

Logic check • Have all pages of the QAF been completed? • Is the correct Part Number & Issue level being quoted? • Is the manufacturing process descried to expectation? • If reference to Tooling is made, have separate Tooling QAF’s been completed? • Is there an economic level and stability period quoted? • What minimum order quantities have been quoted (why)? Although these points are obvious, errors and omissions do occur

Procured Parts (BOF) - interrogation • Procured (BoF) parts information should be subject to in-depth study. • Are sub-tier supplier details available? • Have VA/VE activities been explored? • Have sub-tier costs been interrogated? • Are all sub-tier mark-ups, overheads, logistics costs etc justifiable? • Where high value parts are procured - are they covered by separate QAF?

Raw Materials - interrogation • Who are the suppliers? • Are there any price escalators / exchange rate controls in place? • Is the material price in-line with market prices or other quotations obtained? • Are quoted supply volumes optimised? • Have VA / VE activities been explored? • What is the reclaim strategy?

Manufacturing Process - interrogation • Have ‘Non-Added Value’ activities been eliminated? • Are Set-up times optimised? & well apportioned over Batch sizes? • Is the processing equipment over-specified? • Is the process flow logical & well defined? • Have existing processes been used? • Are parts per hour (cycle times) acceptable? • Are manning levels acceptable (multi-machine manning)? • What are the machine / man-power Utilisation? • How was the process time calculated?

Scrap & Rework - interrogation • What is considered to be Scrap? • How is scrap measured / calculated? • Can scrap be recovered / reprocessed / sold? • Has waste been included as scrap? • Has the timing of where scrap typically occurs been correlated to Purchases? • What ideas exist to make process capability improvements? • The should be no mark-ups on scrap! • What is considered to be rework? • How is rework calculated? • Is rework cost-effective?

Cost Rates (recovery rates) - interrogation • What’s included in the Labour Rate? • How is the Labour Rate calculated? • How are consumable costs recovered? • What shift pattern is the quote based on? • Is manual vs. automated operation optimised? • How is manufacturing overhead calculated? • Are machine tool / equipment depreciation cost realistic? • Do recovery rates reflect industry norms?

Logistics costs - interrogation • Is the supply condition quoted ‘as required’? • What packaging has been costed? • What dispatch quantities have been quoted? • What shift pattern is the quote based upon? • Do the delivery rates reflect industry norms?

Profit Margin - interrogation • Is there double accounting on Profits? • Do quoted profits reflect industry norms? • Are there any unjustified costs that will add to supplier profits? • No profits should be made on material costs; • suffice for reasonable Handling Charge. • No profit should be made on Scrap or Handling Charge. • Waste should be included within gross material content. • Check on how Profit was calculated: • Return-on-Sales calculated profit yields higher returns than Return-on-Costs.

Tooling - interrogation Whilst the previously mentioned questions can also relate to Tooling QAF’s, the following also apply: • Does the Tooling quoted reflect the identified process? • What assumptions were made in the Tooling cost build-up? • Is there an anticipated Tooling life? • Have the sustained costs associated with long life Tooling been catered for? • Is it possible to reduce the number of Tools / inserts? • Does the Tool design incorporate Poke-Yoke principals? • Is the Tooling interchangeable with other Users? • Do the Tool costs reflect industry norms?

Comparative Analysis – method: • List elements of comparators on a spreadsheet / whiteboard. • Perform a logic check against previous known cost breakdowns for similar parts. • In participation with Supplier, use questions identified above (in this .ppt) to question any anomalies. • Gather support from multi-disciplined team (e.g. Cost Engineers, Estimators, Manufacturing Engineers, Design Engineers, Laboratory process experts, QAE and even Purchasing)

Key Points • Ensure you have a sufficiently detailed elemental breakdown of the quotation before you attempt to analyse; otherwise you will end up wasting time guessing at blank figures to justify breakdown. • If in doubt – ask! • Challenge all submitted costs, ask for evidence. • If still in doubt, visit production site to validate claimed costs. • During supplier discussions, record all supplier actions for re-costing of identified elements. • Review revised QAF’s to ensure all actions have been addressed satisfactorily – and establish if further opportunities exist.

Summary • Purchasing must take responsibility for the value chain. • Open and collaborative partnerships need to exist with a number of set suppliers. • Product development will be assisted by healthy supplier relations – providing the benefit of supplier knowledge. • Purchasing need to be commercially challenging / astute. • Buyers need to draw upon skill-sets of Cost Engineers / Analysts and Estimators to help accelerate this process of Supplier Cost Assessment. • Don’t forget, ACostE EMC have built a generic QAF – free for anyone to use, accessible via: • ACostE web site, and • On free 1Gb pen drives. • Thank you.

Acknowledgements • John Henson (Westland Helicopters) • John Paskin (Stadco) • Alan Caddy (Ford Motor Company) • Rolls-Royce plc (SupplierManager-Online) • David Greves (ESA) • Graham Bailey (Lotus Cars) • Greg Maidwell (Eaton Aerospace) • Permission was obtained from Stadco to show their QAF during the actual presentation. Permission obtained did not cover copying it, hence it not being visible within this distributed pack. • Like-wise, Rolls-Royce’s CCW has not been copied into this pack, although it is currently accessible over the internet (and so is in the public domain) via: http://www.suppliermanager-online.com/sabre/topics/bus_req.html#bus_req