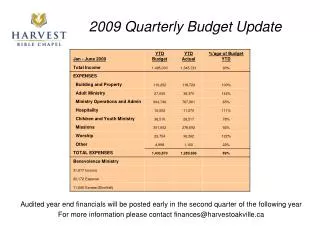

Download

1 / 19

190 likes | 274 Views

Indonesia Economic Quarterly Update Continuity amidst volatility. Shubham Chaudhuri Lead Economist World Bank 23 June 2010 Jakarta Indonesia. What I’ll be talking about. CONTINUITY: Indonesia’s economy continues to perform well…

E N D

Indonesia Economic Quarterly Update Continuity amidst volatility ShubhamChaudhuri Lead Economist World Bank 23 June 2010 Jakarta Indonesia

What I’ll be talking about • CONTINUITY: Indonesia’s economy continues to perform well… • Quarterly GDP growth has continued in line with decade-averages • Inflation continues to be subdued • …and the fiscal position continues to be strong • …AMIDST VOLATILITY: • Financial markets have been more volatile because of developments in Europe • …and commodity prices have continued to be volatile • …AND THE CONTINUING CHALLENGES this implies • Indonesia is more exposed than many other economies to global financial market and commodity price volatility • Commodity price movements matter for Indonesia • Understanding Indonesia’s high lending rates, interest spreads and NIMs

Continuity…GDP growth remains robust… • Indonesia’s economy continued to grow at a trend rate in Q1, driven by strong investment growth • Economy expanded by 1.3% QoQ in Q1, or by 5.7% YoY • A record drop in government consumption was offset by strong investment and private demand growth • Indonesia’s major trading partners also continued to recover in Q1 Indonesian GDP growth Major Trading Partner GDP growth Sources: BPS via CEIC, World Bank

Continuity……and domestic indicators remain strong • Other economic indicators have remained stable at high levels • Consumer indicators are near record highs • Industrial indicators are strong Sources: CEIC, World Bank

Continuity……and mainly based on consumption and services • Private consumption and services continued to contribute the most to GDP growth… Sources: BPS via CEIC, World Bank

Continuity…...as has been the case over the last decade • …Private consumption and services continued to contribute the most to GDP growth Sources: BPS via CEIC, World Bank

Continuity…Inflation continues to track historic lows… • Though headline inflation picked up slightly in May to 4.2% YoY… • …core inflation remained near decade lows, at 3.8% in the year to May • The rise in headline inflation was mainly driven by food prices, which were the only component of CPI to grow above historical averages in the first 5 months of 2010… • …while core inflation remained low due to low capacity utilization levels and appreciation of the rupiah, which limited imported inflation • Inflation is expected to pick up in the 2nd half of 2010, as demand and credit growthcontinue to recover, and administered prices are moved closer to economic costs Source: BPS

Continuity……and the fiscal position remains strong • …with Indonesia continuing to set a global record pace in reducing its public debt-to-GDP ratio

Continuity……with continuing modest budget deficits… • The revised 2010 budget approved by the DPR targets a deficit of 2.1% of GDP Sources: BPS via CEIC, World Bank

Continuity……which may come in even lower than targeted… • Alternative projections of revenue and projected weaker disbursement suggest the budget deficit will be significantly smaller than current government projections, about 1.0% of GDP in 2010 and as low as 0.4% in 2011 • The pickup in commodity prices is likely to support slightly stronger government revenue growth in 2010 • The choice of price measure for nominal growth (deflator versus CPI) has a significant impact on revenue projections • By the end of Q1 2010, only 5 percent of allocated capital expenditure has been spent compared with 10 percent in 2009 Sources: BPS via CEIC, World Bank

Continuity……if we use the GDP deflator as a price gauge • Nominal GDP calculated using the GDP deflator instead of CPI leads to significant reductions in the budget deficit • The national accounts implicit price deflators offer a broader measure of prices than the CPI • The relationship between the CPI and economy-wide prices in Indonesia weakened after 2004, largely due to an acceleration in investment prices that was not captured by the CPI… • …but was captured by the GDP deflator, which as a result has a closer correlation with overall prices in Indonesia • As a result, using the GDP deflator rather than CPI improves the forecast of government tax revenues

Continuity….The outlook remains broadly positive • Outlook remains for gradual pick-up in growth • Continued strong private domestic demand and investment are expected to drive growth, offsetting any drag from imports outpacing exports • A slowdown in major trading partner growth should not impact Indonesia too much • Inflation is expected to accelerate in second half of 2010 on solid domestic demand, credit growth, a more stable exchange rate and rising commodity prices Sources: BPS, CEIC, World Bank. World Bank projections

…amidst volatilityDownside Risks have Increased • External factors have increased risks to the outlook… • Weak demand from OECD economies due to debt crisis could slow down recovery in Indonesia’s MTPs • Increased risk aversion due to debt crisis could increase financial market volatility and capital outflows • Ongoing commodity price volatility could affect real economy forecasts and the budget • …some of which call for the immediate attention of policy makers: • Addressing large capital inflows and outflows • Implementing policies to reduce vulnerability to commodity price shocks

…amidst volatilityCapital outflows pushed markets down in May • Indonesian equities and bonds weakened in May due to large capital outflows that also put the rupiah under pressure • Increased risk aversion due to European events triggered $5.7bn of net foreign capital outflows in May, 90% of this in SBI sales • The JCI fell by 5.5% on the month, yields on five year IDR sovereigns rose by 50 basis points, and Indonesian EMBI USD bond spreads widened by 100 basis points. • The rupiah weakened by 1.8% against the USD

…amidst volatilityFinancial markets vulnerable to capital outflows • After a record month of $4bn of net capital inflows in April, May’s $5.7bn in net capital outflows demonstrated Indonesia’s vulnerability to volatile capital flows • Compared to late 2008, Indonesia’s financial markets are more exposed now to a sudden reversal of capital flows due to the high percentage of foreign holdings of equities, bonds and SBIs • Reserves fell by $4bn in May as BI bought rupiah to smooth out exchange rate volatility caused by capital outflows • 90% of the outflows were SBI sales; new BI policies may help stem some of this going forward

…and some challenges this implies Indonesia particularly exposed to global volatility • Open capital account, relatively large presence of non-resident investors in local financial markets • Importance of commodity prices for Indonesia’s economy Share (%) of commodities in exports

…and some policy challenges Real economy, budget vulnerable to commodity price shocks • Volatility of commodity prices affects real economy and price forecasts in Indonesia as well as budget projections • consider 3 scenarios of commodity price shocks on the economy (+30%, +15% and -15%) • We found commodity price movements have a large impact on prices, and a more subdued impact on the real economy • The poverty rate declined slightly with an increase in commodity prices Sources: World Bank

…and some policy challengesHigh lending rates, NIMs may stifle investment • Indonesia has the highest NIMs in the region, driven by high lending rates • High deposit-side competition but low lending competition for banks in Indonesia leads to high deposit and lending rates, as well as NIMs • High and volatile historical inflation and bond yields increase the risk premium lenders charge on loans • Micro-level inefficiencies such as high operating costs combined with the non-competitive market structure may also contribute to higher NIMs • A deeper financial sector with a more competitive market structure, lower inflation volatility, improved corporate reporting, and higher bank-level efficiency could help reduce rates and NIMs going forward

Indonesia Economic Quarterly Update Continuity amidst volatility Shubham Chaudhuri Lead Economist World Bank 23 June 2010 Jakarta Indonesia