Download

1 / 51

510 likes | 1.03k Views

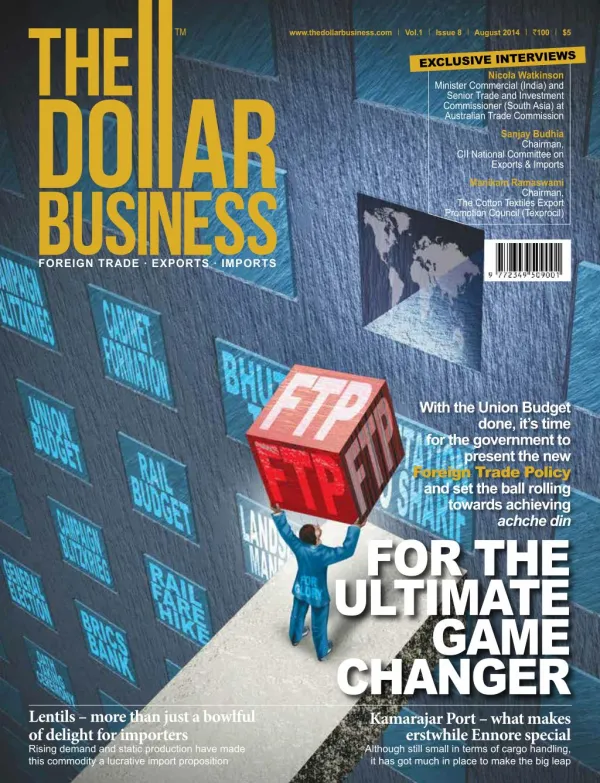

Cover Story – FTP – What the industry wants?<br>With the new Foreign Trade Policy scheduled to be announced this month, we give you a 360 degree round-up of what the industry feels should be done to achieve those elusive ache din... Read More at https://www.thedollarbusiness.com/magazine/archives

E N D

www.thedollarbusiness.com Vol.1 Issue 8 August 2014 100 $5 EXCLUSIVE INTERVIEWS Nicola Watkinson Minister Commercial (India) and Senior Trade and Investment Commissioner (South Asia) at Australian Trade Commission Sanjay Budhia Chairman, CII National Committee on Exports & Imports Manikam Ramaswami Chairman, The Cotton Textiles Export Promotion Council (Texprocil) FOREIGN TRADE . EXPORTS . IMPORTS With the Union Budget done, it’s time for the government to present the new Foreign Trade Policy and set the ball rolling towards achieving FOR THE ULTIMATE GAME CHANGER Kamarajar Port – what makes erstwhile Ennore special Although still small in terms of cargo handling, it has got much in place to make the big leap achche din Lentils – more than just a bowlful of delight for importers Rising demand and static production have made this commodity a lucrative import proposition

LETTER FROM THE EDITOR–IN–CHIEF THE LAST FTP WAS A ‘PASS’. IT SCORED 40%! B Policies cannot be judged unequivocally by outcomes. Under such ambiguity, let us say that in many-a-case, failure becomes the twin of a noble impulse, and criticism is the out- come of bold decisions at a macro-level. But there is an indicative measuring rod. A number that has a soul to appraise performance vis-a-vis promise. When FTP 2009-14 was released, the-then policymakers had set a target of crossing the $500 billion mark in India’s exports by FY2014. The target therefore called for $315 billion in incremental annual exports. By FY2012, it had become profoundly certain that India’s FTP lacked punch – perhaps some real big incentives in the form of credit scrips or drawbacks or even interest rate subven- tions. Our exports that year touched $306 billion, and the utopian expectation of achieving close to $200 billion more in two years seemed unreasonable. During that time, a voice from one of the government chambers claimed thus: “We are well on course to achieve the target to touch the $500 billion mark by 2014...” Minus the ego trip of making an argument to a favoured audience, the claim was hollow. What ensued from the FTP was that India’s total exports in each of the two years following this statement hardly budged. As compared to a target of $500 billion, our exports just about managed to vault past the $313 billion level. Conclusion: Instead of a $315 billion jump that was promised, India’s annual export saw an annual addition of only $128 billion – 40.75% of the desired increase. Going by what we’ve traditionally been taught in school, that meant a pass percentage. But that isn’t enough. What we expect from the new FTP is simple: some bold moves. There are many issues that can be addressed by the new FTP – the strange co-existence of Advance Authorisation and Duty Free Import Authorisation scheme (in the absence of transferability of duty credit scrips), non-accountability of individual States (a five year State-level export policy should be made mandatory), question over the continuation of interest rate subvention schemes (playfully extending such schemes year-on-year isn’t a healthy idea), ineligibility of Service Exports from FMS (Service exports of India brought in $153 billion in forex earnings in 2013; why should we put one sector at a disadvantage to give advantage to another – and what’ the methodology of choosing “select” names in this category?), high transaction costs for exporters (just implementing e-payment systems will not help)...and many more. Real incentives will mean spiritual joy for the exporter community. An exports target of $500 billion in five years (that we missed in 2009-14) could either be a proof of the difficulty of forecasting, or that there is much change that can be incorporated in the new FTP. Whatever that can be done should be done to ensure that the next time we compare the elephant and the dragon in global trade, we get more respect. Forget China, we are behind countries like Mexico and Belgium in exports! An ambitious target isn’t the issue. It’s the policy that has to trigger the onward march beyond borders. A bold, redrafted FTP that can achieve more than just passing percentage when reviewed five years later is what India needs. And that’s not an illogical ask. Or is it? y the time you lay your hands on this issue, expectations from the new Foreign Trade Policy (FTP) would have grown. You are bound to come across pundits conjecturing without evidence, or communities quietly wishing that their trade, swaddled with much suffering turns joyful under the moonlight of true courage on the policymaking front. For the export-import community in India, this is the real union budget, one that will choreograph India’s folk dance in an age of globalisation. This is one foreign policy document that India should care about. When FTP 2009-14 was re- leased, the-then policymak- ers had set a target of cross- ing the $500 billion mark in India’s exports by FY2014. In FY2014, our exports just about managed to vault past the $313 billion level! Steven Philip Warner Editor-in-Chief, The Dollar Business steven@thedollarbusiness.com @SPWarner www.thedollarbusiness/blogs/steven AUGUST 2014 II THE DOLLAR BUSINESS 1

Volume: 01 Issue: 08 August 2014 www.thedollarbusiness.com facebook.com/tdbIndia twitter.com/TheDollarBiz in.linkedin.com/in/thedollarbusiness/ EDITORIAL & RESEARCH Editor-in-Chief: Steven Philip Warner Editor: Manish K. Pandey Executive Editor: Shakti Shankar Patra Deputy Editor (Online): Bidhu Bhushan Palo Senior Editors: Jayashankar Menon, Satyapal Menon Assistant Editor: Sisir Kumar Pradhan Special Correspondent: Neha Dewan Principal Correspondent: Sachin Manawaria Senior Correspondent: Purba Das Editorial Coordinatior: Deepa Pandey EDITORIAL CONSULTING BOARD Founder & Editor: Anil Goyal Publisher: Avnish Goyal Chief Consulting Editor: Dr. A. K. Sengupta (Former Dean, IIFT) RENDEZVOUS SANJAY BUDHIA, CHAIRMAN, CII NATIONAL COMMITTEE ON EXPORT & IMPORT On what the near term holds for India’s exports 94 18 OVERSEAS TALK NICOLA WATKINSON, MINISTER COMMERCIAL (INDIA), AUSTRALIAN TRADE COMMISSION What really matters is the expansion of trade relations and not necessarily who has a surplus and who runs a deficit BRAND ACTIVATION & RESPONSE Vice-President (North and East): Aninda Mondal Manager (West and South): Manish Y. Naik ART & PHOTOGRAPHY Art Director: Sujesh Kumar G. Senior Designer: Sonia Kholgade Photographer : Dileep Kumar THE DOLLAR BUSINESS ONLINE Senior Web Developer: Bhanu Prakash Web Developer: K. Naveen, Web Designer: S. Vamshi Krishna Associate (Web & Network): C. Dileep Reddy DOCKYARD KAMARAJAR PORT LTD India’s only corporate major port is also a ‘landlord’ 70 CIRCULATION & DISTRIBUTION General Manager: S.S. Sudesh Asst. Manager: M. Vinay Kumar, Buddhisagar Pandey, Sanjeev Jain Senior Executive: G. Madhan Rao GLOBAL TRADE THIS MONTH From China becoming the biggest trader to Yemen joining the WTO 06 EXCLUSIVE INTERVIEW FINANCE & LOGISTICS Manager: Parchuri Jhansi Associate: Raj Jarikote 34 COVER STORY 48 PRINTER Kala Jyothi Process Pvt. Ltd., 1-1-60/5, RTC Cross Road, Musheerabad, Hyderabad, Telangana 500020, IN INDIA TRADE THIS MONTH Govt flip-flop on MEP, covert trade war with China and much more 10 ANISH GOEL, MANAGING DIRECTOR, VICTORINOX INDIA FTP - WHAT THE INDUSTRY WANTS? With the new Foreign Trade Policy scheduled to be announced this month, we give you a 360 degree round-up of what the industry feels should be done to achieve those elusive ache din BIG IDEA INDONESIA Shouldn’t we learn from our ancient mariners? 28 PUBLISHED AT 5-2-198/4, Distillery Road, Ranigunj, Secunderabad, Telangana 500003, IN Why you can’t just make up the all powerful ‘Swiss Made’ SPOTLIGHT RUSSIA Has Putin bitten more than he can chew or is the Russian economy reviving © Copyright 2014 No part of this magazine may be reproduced in whole or in part without an ex- pressed permission of the publisher. The information on this magazine is for infor- mation purpose only. The Editor-in-Chief & Editor are responsible for the selection of news and content under PRB Act. Vimbri Media Pvt. Ltd. assumes no liability or responsibility for any inaccurate, delayed or incomplete information, or for any actions taken in reliance thereon. The information contained about each individual, event or organisation has been provided by such individual, event organisers or or- ganisation without verification by us. All disputes are subject to exclusive jurisdiction of competent courts and forums in Hyderabad, Telangana. Printed and published by Avnish Goyal for Vimbri Media Pvt. Ltd. Published at 5-2- 198/4, Distillery Road, Ranigunj, Secunderabad - 500 003, Telangana. 16 SECRET INGREDIENT T-SHIRTS How a small town in South India is dressing up the world 36 FOCUS AND PROMOTION - Not only do we need to focus in right earnest, we need to be cautious about what we promote EXEMPTIONS AND REMISSIONS - Why we shouldn’t tinker with drawbacks every other day EPCG - What do you do when a scheme is very successful but is a monitoring nightmare? EXPORT PROMOTION ZONES - Time for another wave; but then how long can hand-holding continue? SERVICES - Suffering from the taxmen’s inability to understand even services can be exported DEEMED EXPORTS - If we deem them as exports, shouldn’t we also treat them as exports? 80 M. RAMASWAMI, CHAIRMAN, TEXPROCIL On Chinese INFOGRAPHIC LIVE ANIMALS Billions of dollars exchange hands every year, but it’s still ignored 22 IMPORT’ONOMICS LENTILS When satisfying the taste buds is profitable as well 42 policy Printed at: Kala Jyothi Process Pvt. Ltd., 1-1-60/5, RTC Cross Roads, Musheerabad, Hyderabad - 500 020, Telangana. changes and everything else cotton FOR EDITORIAL/CONTENT QUERIES Email: editorial@thedollarbusiness.com . Tel: +91-40-6677 0766 GLOBETROTTER BAJAJ AUTO Time to learn from the past and transform again 24 PRIME FOCUS FREIGHT TRANSPORTATION Clogged arteries & the road ahead NEW-GEN NEWSMAKER Rajen Shah, Managing Director, Arihant Industrial Corporation Ltd. 82 90 FOR ADVERTISEMENT QUERIES Email: ads@thedollarbusiness.com . Tel: +91-40-6677 0765 FOR SUBSCRIPTION QUERIES Email:subscription@thedollarbusiness.com . Tel: +91-40-6677 0765 2 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 3

inbox editorial@thedollarbusiness.com WE VALUE YOUR FEEDBACK, WHETHER CRITICISM OR APPRECIATION. AND HERE ARE A FEW THAT HIT OUR MAILBOXES IN JULY 2014 www.thedollarbusiness.com Vol.1 Issue 7 July 2014 100 $5 Y are the lifeblood of any thriving economy and this should be an excellent focused magazine. Best of luck! RAJESH GARG Global CFO & Member of the Board, Cipla Limited, Mumbai our magazine seems like a great idea to fill a crucial gap for Indian business. Exports EXCLUSIVE INSIDE COLUMN: Arthur C. Wheaton Director, WNY Labour and Env. Programs, Cornell University INTERVIEWS: Dr. Alok Bharadwaj Executive Vice President, Canon India R. Ramesh Kumar Executive Director, Council for Leather Exports Yaduvendra Mathur Chairman & Managing Director, FOREIGN TRADE DECODED EXIM Bank Marie-Josée Charbonneau Counsellor & Head, High Commission of Canada in India DESTINATION BRAZIL Is this booming Latin American market a delight for Indian exporters? Pectin – bet you haven’t heard about it A great example of the direct correlation between information asymmetry and rate of return Is India’s darling port losing its sheen? Many claim that all is not well at Kandla, India’s No.1 major port. Can it silence its critics? For Indian brides & foreign buyers With 80% of the world’s total turmeric being produced in India, this spice can work wonders for exporters How SFIS ‘almost’ became famous The objective of the “Served From India Scheme” was to boost exports of services from India. But has it, really? A commodities and areas for exports! It is the best available reference point for exporters and import- ers in the country. A must read for every stakehold- er in the arena of global trade. Aptly described as ‘Foreign Trade Decoded’! AREEJ AFTAB Assistant Professor, Indian Institute of Foreign Trade (IIFT), New Delhi great initiative, abundance of information, in-depth analysis, holistic coverage of thrust R 2014). I think it is really interesting how cycle ex- porters make money only due to incentives that the government provides. Looking at the glass half empty, should we not expect the government to give greater incentives to encourage such brave industry players? ARVIND MATHUR Chartered Accountant, New Delhi efer to The Midas Touch “Pedal your way to health and fortune” (The Dollar Business, July I ASHISH NANDA Director, Indian Institute of Management, Ahmedabad look forward to reading The Dollar Business with interest. Wish you the very best in this enterprise. T Canada’s commitment to increase trade ties with India. We really appreciate the profes- sionalism that you all work with and the final coverage is indeed impressive. We are indeed grateful to you for your willingness for choos- ing to cover Canada. It’s really encouraging for us when we witness the receptiveness of Can- ada’s efforts in strengthening bilateral relation- ship with India by a platform like yours. We are honored to be recognized for this, and we look forward to work with you in future endeavours. HIGH COMMISSION OF CANADA New Delhi he report published in the inaugural is- sue has provided a positive exposure for I you and your team for shaping it well for new age entrepreneurs who have the passion to go global in terms of reach and diversity. DR. K. SRINIVASA RAO General Manager – Strategic Planning, Bank of Baroda, Mumbai had the opportunity to go through a couple of is- sues of The Dollar Business. Congratulations to 4 THE DOLLAR BUSINESS II AUGUST 2014

GLOBAL TRADE THIS MONTH News & Analyses REPUBLIC OF THE PHILIPPINES RICE IMPORTS In the name of protection After winning approval of other WTO nations to extend (quantitative) re- striction on rice imports, Philippines has agreed to increase the WTO min- imum access volume (MAV) from 350,000 tonne to 805,200 tonne per year and lower the import duty on rice under the MAV limits from 40% to 35%. Rice imports outside of the MAV will continue to have a 50% tariff. The Philippines will allocate 755,200 tonne of rice imports under country specific quotas (which is likely to include China, India, Pakistan, Thailand and Vietnam), while any WTO member can supply the remaining 50,000 tonne. According to the Philippines Department of Agriculture (DA), milled rice production in the country increased by around 1.6 million tonne during CY2010 and CY2013. Howev- er, rice consumption in the country is higher than production and the country is expected to import around 1.6-2 million tonne of rice this year. The Philippines government is keen to protect local farmers from imports as rice from India, Thailand and other Asian exporters is substantially cheaper than local rice. Changes in the MAV for rice is part of the negotiations Philippines is involved in to seek a five-year extension of the WTO Quantitative Re- striction (QR) that expired in June 2012. KINGDOM OF SAUDI ARABIA NON-OIL EXPORTS Putting eggs in different baskets YEMEN REPUBLIC JOINING WTO Integrating with the new world order Yemen has become the 160th country and the 35th Least Developed Country (LDC) to join the World Trade Organisation (WTO). The entry will help Yemen gain preferential (sometimes duty-free) access to markets in several rich coun- tries. Yemen will also get technical assistance and capacity building from WTO to boost its trade. Yemen’s WTO commitments include granting trading rights in a non-discriminatory and non-discretionary manner by December 31, 2014, and opening market for goods and services. For goods, Yemen has committed to limit its tariffs to an average of 21.1% for all products – 24.9% on average for agricultural products and 20.5% for oth- er products. The country will also open its markets to 11 core services sectors: business services, communication services, construction and related engineering services, distribution services, educational and environmental services, financial services, health services, tourism and travel, recreational, cultural and sporting services and transport services. Yemen’s entry is expected to boost its trade with UAE, China, Netherlands, Saudi Arabia, Switzerland, Kuwait, India, Japan, Brazil, Turkey and USA – some countries with which it already has bilateral agreements signed. Expectations are that India’s exports to Yemen that fell y-o-y by 11.4% to about $1.3 billion in FY2014, will also get a boost with curbs on many imports removed. Saudi Arabia’s non-oil exports have in- creased significantly from last year due to increasing focus on economic diver- sification. According to official sourc- es, the value of Saudi Arabia’s non-oil exports in Q1 CY2014 stood at about $14.62 billion, up 18.7% y-o-y. The coun- try’s Minister of Commerce and Industry Dr. Tawfiq Bin Fawzan Al-Rabiah claims continued growth of non-oil exports will help economic diversification over the coming years. Its non-oil exports include plastics and metal goods. Wheat being harvested Saudi Arabia’s exports Total exports of $356 billion in CY2013 CROP PRICES ON A DECLINE Not a secular trend According to UN’s Food and Agricul- ture Organisation (FAO) and OECD, the recent decline in prices of major crops in the international market is likely to continue for another two years, when prices are likely to stabilise at pre-2008 levels. The FAO Food Price index stood at 161 in 2007, but surged about 25% to 201 points the next year. It peaked at 230 in 2011, but has declined since to around 206 as of June 2014. The reason for this decline has been higher produc- tion, which have pushed stocks to all- time highs. OECD Secretary-General Angel Gurría feels crop prices were un- usually high earlier and that agriculture markets are returning to more settled conditions now. FAO also feels another reason for a de- cline in crop prices is the change in food patterns across the world, with people consuming more protein, sugar and fats due to urbanisation. However, cereals are expected to continue to be the major staple in the next decade, with most of the production taking place in Asia and Latin America. “Developing regions will account for more than 75% of the addi- tional agricultural output over the next decade,” FAO says. A rice mill process production line 3% Traditional architecture in Sanaa, Yemen. Inhabited for more than 2.500 years, the Old City of Sanaa is a UNESCO World Heritage City 1% Philippines’ rice imports Import restrictions have ensured a massive fall in rice imports in recent years 1% 4% 5% 2,000 1,500 86% 1,000 500 0 Mineral Fuels Plastic and articles of plastic Organic Chemicals Fertilisers Inorganic Chemicals Other CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 Source: International Trade Centre; figures in $ million Source: International Trade Centre; Breakup for CY2013 Yemen’s global trade Yemen’s total trade has never crossed even $20 billion UNTIED STATES’ INDEPENDENCE DAY CHINESE FIREWORKS Chinese crackers light up US skies Chinese fireworks industry got another feather on its cap as it dominated the US Independence Day celebrations. Most of the fireworks (estimated at millions of dollars) that brightened American skies on July 4 this year are believed to have been imported from China. China already controls the fireworks import market in US with imports from the dragon nation stand- ing at $203.6 million in CY2013. This is about 95% of the total fireworks im- ports by US during the year. Industry insiders claim that Chinese fireworks imports are likely to increase due to the product’s improving quality. They also claim that ‘Made in China’ fireworks are almost 10 times less expensive as compared to those made in US. 12 10 8 6 4 2 0 CY2004 CY2005 CY2006 CY2007 CY2008 CY2009 CY2010 CY2011 CY2012 Imports Exports Source: International Trade Centre; $ billion AUGUST 2014 II THE DOLLAR BUSINESS 7 6 THE DOLLAR BUSINESS II AUGUST 2014

GLOBAL TRADE THIS MONTH News & Analysis News & Analysis In the fifth review of the trade policies and practices of China during 2012- 2014, WTO said that China has become the world’s largest trader (excluding in- tra-EU trade) but needs to rebalance its economy and boost consumption in the country to maintain the growth. According to WTO, China’s merchan- dise trade stood at $4.16 trillion in CY2013, which included $2.21 trillion of exports and $1.95 trillion of im- ports. Manufactured products (mostly office machines, telecommunication equipment and textiles) accounted for around 94% of total exports by China in CY2013, while machines, chemicals, fuels, mining products and agricultural products accounted for most of the na- tion’s imports. WTO members say China’s growth model hinges largely on investment (FDI) and directed credit availability. China should rebalance its economic growth through policies to promote consumption and push for further liberalisation of the domestic market. WTO members have also urged Chi- na to have a transparent global trading system. It’s worth noting that China became a WTO Member in December 2001, almost seven years after India joined the WTO in January 1995. PEOPLE’S REPUBLIC OF CHINA LARGEST TRADER A dragon, in need of a rebalancing act ISLAMIC REPUBLIC OF PAKISTAN THRUST ON EXPORTS Waking up to economic reality CAMEL IMPORTS BAN SAUDI ARABIA-SOMALIA An economy left to survive on piracy? The Pakistan government is planning an overhaul of its trading model and of the Trade Development Authority of Pakistan (TDAP) as it aims to more than double its exports from the current $23.1 billion to over $50 billion per year. Pakistan’s Commerce Minister has said he has constituted a committee that will oversee the major transition. He said there is an urgent need to transform TDAP to boost exports. The minister has also asked the committee members to prepare a model that emulates the success of export-based East Asian economies. This is the first time TDAP has been targeted since it was established in 2006 under a presidential ordinance during Pervez Musharraf’s rule. In- dustry insiders claim the move will please several trade bodies and associ- ations in Pakistan that have accused TDAP of creating hurdles in exports and of monopolising exports in the name of quality restrictions. When Somalia got a federal government in mid-2012 after a fragile transition, many saw hope that the Horn of Africa had the best chance, in two decades, to survive and achieve stability. However, the country’s future is at stake due to both rebels and from a proposed ban of camel imports from the country by Sau- di Arabia. Somalia’s GDP per capita and human development indices are among the lowest in the world. Livestock still conststitutes the bulk of the country’s economy. According to the World Bank, livestock supports about 60% of Soma- lia’s jobs, 40% of its GDP and account for 80% of its exports. Almost 70% of Somalia’s livestock ex- ports find a destination in Saudi Arabia. Although camels account for a small share of the 4.5-5 million animals that Somalia exports to Saudi Arabia ev- ery year, experts feel any ban on camel imports by Saudi Arabia could have a cascading effect and devastate Soma- lia’s economy like it happened in 2000. About 14 years ago, Saudi Arabia had banned livestock imports from Somalia over quarantine concerns regarding the spread of rinderpest and Rift Valley fe- ver. This time, Saudi Arabia health offi- cials suspect Somali camels could be car- rying the deadly MERS virus, which has reportedly killed nearly 300 people and infected many more. China is also by far the world’s largest exporter of apparels with exports worth over $12 billion in CY2013 BRICS NEW DEVELOPMENT BANK A new threat to the IMF and the World Bank? Leaders of the BRICS have launched a $100 billion New Development Bank (NDB), which will be based in Shanghai. The first President of NDB will be from India. NDB will have an initial authorised capital of $100 billion and the initial subscribed capi- tal will be $50 billion, which will be equally shared among the founding members. NDB will aim to address financial constraints that BRICS nations and other developing econo- mies face. In a joint declaration, the BRICS members said, “We continue to face signif- icant financing constraints to address infra- structure gaps and sustainable development needs. With this in mind, we are pleased to announce the signing of the agreement establishing the New Development Bank (NDB), with the purpose of mobilising re- sources for infrastructure and sustainable development projects in BRICS and other emerging and developing economies.” BRICS has also launched a Contingent Reserve Ar- rangement (CRA), with an initial size of $100 billion, to help member nations manage cur- rency fluctuations and economic volatility. BRICS represents around 19.8% of global GDP and 16.9% of global trade. Total exports by the five member countries have grown over 500% in the last decade. In the four years between 2008 and 2012, BRICS’ inter- national trade increased almost 42%, from $4.3 trillion to $6.1 trillion. THE WORLD TRADE ORGANISATION (WTO) TRADE PROMOTION One way ticket to fame and glory The World Trade Organisation (WTO) has launched a ‘trade stories’ sel- fie competition, which will allow an individual to share one’s trade story with the world. The competition is a part of the run-up to WTO’s Public Forum that will take place during October. The theme this year is “Why trade matters to everyone” and the aim is to bring out the human angle behind trade. Do you think you can do it? Why not send your entry to WTO at selfie4trade@wto.org. Remember, the last day for entries is the 1st of Sep- tember. If you are selected, your selfie will be displayed at the Public Fo- rum, posted on the WTO website and its social media channels and of course flashed on news channels and newspapers worldwide. Livestock is the main occupation of the local population in Hargeisa, Somalia’s second largest city Xi Jinping President, China 8 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 9

INDIA TRADE THIS MONTH News & Analysis News & Analysis JUTE INDUSTRY REVIVAL ATTEMPTS For a greener world The Indian government is trying to revive the domestic jute in- dustry that has been on a decline due to dropping demand for jute products and lack of modernisation. Although India is by far the world’s largest producer and consumer of jute products, increasing popularity of plastic substitutes and lack of mod- ernisation has hurt its jute industry. In the last 10 years, five units of National Jute Manufacturers Corporation Ltd. (NJMC) have been declared sick and jute prices have plunged close to the minimum support prices (MSP). In order to revive the sagging fortunes of the industry, the government recently approved Rs.1,562.98 crore, which in- cludes financial restructuring and grant for Voluntary Retire- ment Schemes (VRS) of mills under NJMC. The government has also launched the Jute Technology Mission (JTM) under which a subsidy of Rs.104.36 crore has been provided to help jute mills install new machinery. Experts say demand for envi- ronmental friendly products is growing all over the world and the jute industry in India and Bangladesh (the world’s largest exporter of jute products) should grab this opportunity. CHINESE MILK EXTENSION OF BAN Need Operation Flood 2.0 The Directorate General of Foreign Trade (DGFT) has extended the ban on imports of milk and dairy products from China until June 22, 2015 over concerns of melamine contamination. The ban covers chocolates, chocolate products, candies, confectionery and food preparations made with milk or milk solids. It’s worth noting that milk production in India – the world’s largest producer – increased by about 7.6 million tonne to about 140 million tonne in FY2014. However, consumption is rising at a much faster pace and is expected to reach around 200 million tonne by 2024. In fact, India’s Minister for Agriculture recently said, “India may have to import milk in the future if production does not grow by 6 million tons per year for the next 10 years.” Jute fiber being dehydrated after retting, alongside a road in Howrah Indo-Bangladesh trade Bangladesh’s exports to India is yet to cross $1 billion in a year INDIA-BANGLADESH TRADE TRADE DYNAMICS Too skewed for comfort The Confederation of Indian Industry (CII) claims India-Ban- gladesh trade could double to over $10 billion by FY2018 if Non-Tariff Barriers (NTBs) and infrastructure related con- cerns are addressed on both sides. At present, trade between the two countries is heavily tilt- ed in favour of India. According to CII, two-way trade be- tween India and Bangladesh stood at FY2014 with India’s exports at $6.1 and imports at a mere $462 mil- Decline in exports to India poses rious challenge for the Bangladeshi government and might trigger pro- tectionist measures in future. While revving up imports from Bangladesh may be difficult, CII suggests the skewed trade dynam- ics between the two nations could be redressed with greater investment participation of Indian companies in Bangladesh. Indian investments in Bangladesh stood at $2.5 billion in FY2013, and have surged in the last three years. “This can grow further,” says CII. CII suggests addressing NTBs such as harmonisation and non-recognition of technical standards can help. In addition, resolving CHINESE GELATINE DEMAND FOR BAN A matter of life and death India’s pharmaceutical industry has urged the Drugs Controller General of India (DCGI) to ban gelatine imports from China due to excessive presence of chro- mium. Gelatine is used by pharmaceutical companies to make the outer covering of some capsules. However, Indian pharmaceutical companies claim that in China gelatine is made out of the waste from leather factories and contain harmful levels of chromium. According to the US Food and Drug Administration (USFDA), numerous companies in China use industri- al-grade gelatine to make pharmaceutical-grade gela- tine capsules. “This industrial-grade gelatine contains more chromium than the edible gelatine that firms should have used,” it says. Indian pharma companies claim that although the Chinese Food and Drug Ad- ministration (CFDA) shut down certain factories man- ufacturing pharmaceutical-grade gelatine in China in 2012, the Indian government is yet to ban imports of chromium-tainted gelatine, which is cheap but harmful. It’s worth noting that in a recent report, the Asso- ciated Chambers of Commerce and Industry of India (ASSOCHAM) observed that while India is a leader in pharmaceutical exports with exports to over 200 coun- tries, it is heavily dependent on imports from China for many essential and large volume drugs. 7 6 5 4 3 2 $6.6 billion in billion 1 0 lion. a se- FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Exports from India Exports from Bangladesh Source: Ministry of Commerce, GoI; figures in $ billion infrastructure problems, and improving the investment process in Bangladesh with sin- gle window clearances, upgrading the tax holi- day system and improving connectivity can help bolster economic partnership between the two nations. As per CII, some potential sectors for investment in Bangladesh include electrical machinery and equipment, vegetable/roots and tubers, agro-processing, automobiles, textile (including home textile), organic chemicals and light engineering. In the ser- vices sector, ICT, pharmaceuticals, hospital & medical equipment, tourism and profes- sional services offer good opportunities. India’s imports of empty gelatine capsules Empty gelatine capsule imports saw a big surge in FY2010 20 18 16 14 12 10 8 6 4 2 0 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Source: Ministry of Commerce, GoI; figures in $ million 10 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 11

INDIA TRADE THIS MONTH News & Analysis News & Analysis HEALTH SUPPLEMENTS COURT VERDICT For freer markets Hearing the petition of Vital Neutraceutical, a Mumbai-based food business operator (FBO) and Indian Drug Manufacturers Association (IDMA), the Bombay High Court has quashed an advisory issued by the Food Safety and Standards Association of India (FSSAI), which had made prior product approval mandatory for dietary food and health supplements already licensed and existing in the market. The Court called the Product Approval (PA) adviso- ries issued by the FSSAI unlawful. According to the Advisory, manufacturers were required to take approval for a spectrum of food products including “novel foods, functional foods, food supplements, irradiated foods and genetically modified foods.” Clause 22 of the FSS Act/Rules & Regulations states that food business operators (FBOs), who are the manufac- turers of proprietary foods, genetically modified articles of food, functional foods, health supplements or nutraceuticals are required to apply for the product approval with the central licensing authority. ESSENTIAL ITEMS LIST ONION & POTATO No clear vision The Cabinet Committee on Economic Affairs (CCEA) has put onion and potato under the purview of stock holding limits under the Essential Commodities Act, 1955 to control pric- es and check hoarding. Prices of onion and potato increased sharply in May-June, with a 40% increase in wholesale prices of potato just in May. The government has already set a min- imum export price (MEP) of $450 per ton (about Rs.27 per kilogram) on potato which is expected to reduce exports. The government has also increased the MEP on onion to $500 per ton (about Rs.30 per kilogram) after the MEP of $300 per ton (about Rs.18 per kilogram) set in June failed to have any im- pact on onion exports and domestic prices. BHUBANESWAR WTC BRANCH It’s time to reach out to the world The World Trade Centre (WTC) has opened its new branch in Bhubaneswar, Odisha, making the state a part of the WTC network of 343 branches in 100 countries. The facility is the fifth WTC branch in India. Odisha’s Chief Minister Naveen Patnaik has promised that the branch will move into its own building within three years. The new WTC is expected to help boost trade in the state and act a as a bridge between local com- panies and global businesses. WTC Bhubaneswar will have top-end facilities to spur trade, including a convention centre and a 1.7-km skywalk to connect it with hotels. Odisha aims to increase exports from the state to Rs.29,693 crore in 10 years, for which exports must grow at a CAGR of 10% from its FY2013 level of Rs.11,448 crore. The state government has iden- tified minerals & metallurgical products, engineer- ing, chemical and allied products, marine products, electronics & software, agricultural products, hand- loom, textiles & handicrafts and tourism as sectors with vast potential for exports. To boost exports, Odisha plans to set a B2B exchange facility, a district level export promotion committee, and incentives like exporter’s green card for seamless passage of ex- port consignments. Naveen Patnaik Chief Minister, Odisha Indian onion and potato exports Last year India exported over $500 million worth of onions NORTH-EASTERN STATES FLORICULTURE EXPORTS Lure of the yen The Agricultural and Processed Food Products Export Development Au- thority (APEDA) is fast-tracking the development of a road map that will enable flower exports from North-Eastern states to countries with high demand like Japan. India’s floriculture exports grew strongly to about Rs.455.9 crore in FY2014, which is about 25% higher than that of FY2013. The floriculture sector in India is very fragmented, with most of the com- mercial cultivation in West Bengal (32%), Karnataka (12%) Maharashtra (10%) and almost half of the export units based in Karnataka, Andhra Pradesh and Tamil Nadu. In recent years, flower production in several states have declined due to warm weather conditions. However, experts feel the temperate cool weather in the North East is more suitable for flo- riculture and encouraging exports can act as a game changer for the do- mestic economy of the region. 600 500 400 300 200 100 0 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Onion Potato Source: Ministry of Commerce, GoI; figures in $ million Industry insiders feel flower exports to Japan can be a game changer for North Eastern states RESERVE BANK OF INDIA INCREASE IN CREDIT PERIOD Diamonds shine back The Reserve Bank of India (RBI) has extended the credit period given by a foreign supplier to Indian buyers of rough, cut and polished diamonds to 180 days. Until now, the same was 90 days. According to the RBI, “Credit given by a foreign supplier to its Indian customer/ buyer, without any Letter of Credit (Suppliers’ Credit)/Letter of Undertaking (Buyers’ Credit)/Fixed Deposits from any Indian financial in- stitution for import of rough, cut and polished dia- monds, may be permitted for a period not exceeding 180 days from the date of shipment.” The RBI took the decision after considering proposals received from diamond importers and GJEPC. GJPEC has welcomed the move saying, “Supplier’s credit limit of 90 days was ‘severely ham- pering’ the business cycle and had become an im- pediment for export of cut and polished diamonds.” ORGANIC SUGAR EXPORTS CEILING REMOVED Sugar-coat the bitter pill The Directorate General of Foreign Trade (DGFT) has removed the ceiling of 10,000 tonne when it comes to the export of organic sugar, provided the export is registered with DGFT and certified by Agricul- tural and Processed Food Products Export Development Authority (APEDA). The move is aimed to help improve exports of sugar and allow more funds into an industry that hasn’t paid for a long time now. In FY2014, India’s sugar production stood at around 242.27 lakh tonne – down 4% y-o-y – of which 240 lakh tonne is expected to be consumed domestically. The surplus stock is estimated at 2.27 lakh tonne, which will push overall stocks to around 67.4 lakh tonne. However, industry insiders feel the removal of the quantitative ceil- ing on sugar exports is cosmetic because of the ‘organic’ rider as very few sugar mills in India have the certification. The certification pro- cess for organic sugar is also very lengthy. The sugar sector in India has been a political hot potato and sees policy changes very often Sacks of potato waiting to be loaded to a ship before being exported 12 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 13

OVERSEAS TALK NICOLA WATKINSON, AUSTRALIAN TRADE COMMISSION, INDIA “WE BELIEVE INDUSTRIES GROW BETTER WHEN THEY ARE LESS PROTECTED” Indo-Australian trade ties haven’t really benefitted from the cricketing connect, with Australia not featuring even in the list of top 20 trading partners of India. To understand what is affecting the bilateral trade and what actually can be done to improve the situation, The Dollar Business sat down with Nicola Watkinson, Minister Commercial (India) and Senior Trade & Investment Commissioner (South Asia) at the Australian Trade Commission in New Delhi. Excerpts from the conversation: Indian exports to Australia Very little and fragmented 13% 11% 57% 8% BY NEHA DEWAN 6% 5% Gems and Jewellery Automobile and Accessories Pharmaceutical Products Mineral Fuels Textiles Other Nicola Watkinson Minister Commercial (India) and Senior Trade and Investment Commissioner (South Asia) at the Australian Trade Commission at New Delhi, India TDB: Bilateral trade between India and Australia is about $12.45 billion, with India having a trade deficit of close to $8 billion. Do you think India needs to be concerned about this trend? Nicola Watkinson (NW): A large chunk of our exports to India are energy relat- ed products. Given the strong focus that India has on energy security, this should not be a cause of concern and I am sure the Indian government has recognised Australia as a stable, long-term and re- liable partner. Also, a large number of Indian companies are integrating their operations in Australia. So, a lot of ener- gy related products that are coming from Australia, are actually coming from In- dian companies. We have enormous in- vestments from companies such as GVK and the Adani Group in our coal sector. I see this as a very positive development in our relationship. Another area which can be developed over time is Liquefied Natural Gas (LNG) as India looks at al- ternative fuels. Gas is probably one of the areas where we will be able to extend our relationship further. Australian exports to India Much about coal and copper! 23% 46% 3% 4% TDB: India’s bilateral trade deficit that we are referring to – is it here to stay? NW: I think the main focus should be on the overall growth of trade between the two economies. I see strong oppor- tunities for Indian companies who are looking to tap the Australian market. We have already seen very strong growth in 10% 14% Coking Coal Copper Ores Unwrought Gold Calcined Alumina Other Coal Other Source: Ministry of Commerce, GoI; Breakup for FY14 18 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 19

OVERSEAS TALK NICOLA WATKINSON, AUSTRALIAN TRADE COMMISSION, INDIA TDB: How protected do Australian manufacturers feel then? Isn’t it dis- couraging for them to an extent be- cause you do not protect them while most countries – including US, espe- cially post-2008 – shield their manu- facturing corporations? NW: Of course, people have always asked for protection. But we have seen that companies in Australia have been able to work in an environment with lit- tle protection for them and at the same time, are globally competitive. They are born global. So, if they can compete against Indian or Chinese or Korean suppliers at home, they will be able to compete with them in their countries as well. We believe that if we actually want to have genuine global trade, we have to be prepared to play the game ourselves. Our textile industry is a great example of this. We do not have companies that produce low-quality products because we can get that more economically from India or Bangladesh. Therefore, the tex- tile industry in Australia is focused just on producing high-end sportswear, lei- surewear and bridal-wear. Australia offers world-class service solu- tions in age care. So, we would be very interested in offering our services in In- dia. It is a trend that I think is set to grow. the IT sector. Australia has been one of the top three global markets for Indian IT companies and they have been one of the largest sources of employment in Australia. They are certainly picking up large contracts in Australia, bringing the work back here. I believe this is an important export, which we shouldn’t ignore. Wellness products, particularly Ayurvedic products, are also seeing ris- ing demand from Australian consumers. THERE ARE PROGRAMMES THAT AUSTRALIA USES TO SUPPORT ITS NEW EXPORTERS. BUT THOSE ARE NOT SUBSIDIES TDB: Does the Australian govern- ment give any incentive to its services and manufacturing sectors that India needs to emulate? Does it provide extra incentives to its exporters? NW: There are a couple of programmes that Australia uses to support its new exporters. But those are not subsidies. They are supports to help them explore new markets or help produce market- ing material that will be specific for one particular market such as, say, China or Mexico. We just did a survey with 4,000 Australian exporters and asked them what makes it difficult for them to come to India. The answer is not subsidies; it is information and access to advice. TDB: India’s auto and auto component manufacturers have not been able to make inroads into Australia. What do you think is the reason? NW: The Australian automobile indus- try is going through a transition. A num- ber of auto manufacturers will be scaling down their manufacturing operations in Australia in the coming years. While they all have come a long way, they still have challenges in the level of innovation that they have in their companies. I think the growth of the global automotive sec- tor will not be in countries such as Aus- tralia – which has just 23 million people – but in high-growth and more populat- ed markets like India, China, Indonesia and Malaysia. readily understand. It will tell you the region, the vineyard and the year. In Australia, we realised that we need to tell people what kind of grape it is made out of. Telling them so will help them understand its flavour. We also tell the buyers what to do with it. We tell them what goes best with a particular wine. I think this is what really works in the In- dian market, which is still an emerging market for wine. The little information make our wine brands more approach- able. Another factor is new vinification (winemaking) techniques. We have tak- en our young wine makers to France for them to better understand vinification techniques. Our Minister for Tourism plans to bring a delegation of Australian wine makers to India to work with In- dian wine producers who are interested in partnering with us. We will be shar- ing some of our winemaking knowledge with our Indian counterparts that will help them improve quality, range and productivity. TDB: Australia is a huge consumer market. So, besides services, which are the other sectors or industries that In- dian exporters should focus on? NW: Australia is one of the most open economies in the world. It is ranked 11th in the world for ease of doing business. If you have a product in India that you are looking to export to a developed economy, which provides easy access and offers higher margins, then Austra- lia should certainly be on top of your mind. Also, in one of my recent interac- tions with the Federation of Indian Ex- port Organisations (FIEO), I learnt that they were looking to send a delegation to a large trade show in Australia, which is scheduled to happen in November this year. Moreover, import duties are very attractive for international companies looking at the Australian market. Hence, there is no reason why Indian exporters shouldn’t go to Australia. We have a phi- losophy that industries grow better when they are less protected. Our companies are more globalised because they are not shielded by subsidies or tariff barriers. Coal being loaded into a ship at Newcastle in Australia. Newcastle is the south hemisphere’s largest port for coal exports TDB: Australia’s Jacob Creek is one of the most widely imported wines in India. It’s more popular than even top French and Italian brands. Can you tell us the secret of the success of Austra- lian wine in India? NW: I think Australia has taken a very different approach towards marketing wine. If you look at French wine labels, it will not give you information that you tralia has signed a Free Trade Agreement with Korea, Japan and we are working very hard for a deal with China. We are definitely looking at creating stronger multilateral trade deals. With both coun- tries having new governments, I believe, now is a good time to look at how we can re-establish the CECA negotiations. panies are looking at opportunities to do business globally and entering markets that have an open working environment. TDB: Indian duty on wine imports is one of the highest in the world. What’s your view on this? NW: From an Australian perspective, we face the same wine tariff as some- one from US or France. So, this is not a competitiveness issue. The ones who are most affected by the high tariffs are the Indian consumers, who end up paying a lot for a bottle of wine. TDB: Education has been Australia’s dominant export to India. Do you see any other sector having the potential to scale up to those levels? NW: At the moment, the traditional business in education has been to attract Indians to study in Australia. We have reaped really good economic dividends from this business model. But now our focus is more on diversification and to increase the range of courses that they undertake. The other opportunity that I see is skill development and vocational training, which is altogether a different model. Apart from skill development and vocational training, there’s much opportunity in areas such as age care. It is still in a nascent stage in India while Indo-Australian merchandise trade India has almost always run a trade deficit with Australia TDB: What would be your message to Indian exporters who are looking at Australia as a potential market? NW: My message would be simple. Aus- tralia is open to doing business. It has one of the most stable and open economies in the world. It has good, solid growth. There are already a number of support mechanisms for exporters in Australia. There is a large Indian community that they can tap into. Just do some prepara- tion about what works in the market. TDB: In most countries, including In- dia, we see only big trading houses ben- efitting from these trade agreements. Don’t you think it is discouraging for small entrepreneurs as they are not really given a fair chance to compete against the big players? NW: What we are trying to do is bring together benefits for both large and small companies. The Australian economy comprises of largely small and medium enterprises. We do not really have any big MNC as such. Small and mid-size com- 18,000 16,000 14,000 12,000 10,000 TDB: The proposed Comprehensive Economic Cooperation Agreement (CECA) between India and Australia is yet to be signed. Can you tell us when the agreement will come into effect? NW: Australia is a very strong believer in multilateral and bilateral trade agree- ments. The current government in Aus- 8,000 6,000 4,000 2,000 0 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 India’s exports to Australia India’s imports from Australia neha@thedollarbusiness.com Source: Ministry of Commerce, GoI; figures in $ million 20 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 21

Global live animals trade Breakup of India’s live animals exports 25 20 15 GOATS ..........................................................................84.0% POULTRY ......................................................................4.0% WEIGHING > 185 GM POULTRY ......................................................................5.0% WEIGHING <= 185 GM OTHER BIRDS............................................................2.0% PARROTS ......................................................................1.0% OTHER ............................................................................4.0% 10 5 Source: Ministry of Commerce, GoI; Breakup for FY2013 0 `FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 Exports Imports Source: International Trade Centre; figures in $ billion India’s live animals exports is dominated by the export of goats, with most of them being exported to its neighbour Nepal For the last three years, live animals worth over $20 billion have been traded globally. (Note: Minor differences between exports and imports arise due to certain non-reporting countries) Breakup of India’s live animals imports India’s live animals trade PURE BRED BREEDING HORSES ................6.8% OTHER HORSES ....................................................30.3% POULTRY WEIGHING .........................................21.9% <= 185 GM OTHER MAMMALS ..................................................1.5% HORSES FOR POLO ...............................................0.7% OTHER ..........................................................................38.8% 18 16 14 12 10 Source: Ministry of Commerce, GoI; Breakup for FY2013 8 6 4 2 0 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Exports from India Imports to India Horses are India’s main live animals imports, with close to $4 million worth of horses imported in FY2014. Most of them are imported from UK and US Source: Ministry of Commerce, GoI; figures in $ million India is a very small player in the global live animals trade, with just over $11 million worth of exports and $10 million worth of imports during the last fiscal Bovine animals account for over a third of global live animals trade, which also witnesses millions of dollars worth of trade in camels, horses, rabbits, reptiles and birds. Interestingly, even live bees worth over $35 million were traded in CY2013 11% HORSES, ASSES, MULES, HINNIES 9% OTHERS 5% SHEEP & GOATS Source: International Trade Centre; Breakup for CY2013 AUGUST 2014 II THE DOLLAR BUSINESS 23

GLOBETROTER BAJAJ AUTO STILL INDIA’S ‘CAR ON TWO WHEELS’? Geographical spread of exports Within Africa, Nigeria is the top destination Category-wise break up of exports Boxer is manufactured solely for exports KTM Discover Performance (Pulsar) Platina Boxer & CT100 Africa South Asia & Middle East ASEAN Latin America Rarely has a company chronicled the history of a country the way Bajaj Auto has done in the case of India. Right from the days of founder Jamnalal Bajaj – such an ardent follower of Mahatma Gandhi that the latter had adopted him as his son – the company has been a proxy to everything that is India. But having realised that the company had lived for far too long just on nostalgia, current Managing Director Rajiv Bajaj is a man on a mission to transform the very way the world looks at Bajaj Auto. Is he on the right track? The Dollar Business investigates 14% 19% 7% 46% 18% 2% 63% 28% 3% Source: Bajaj Auto; FY2014 Annual Report BY JAYASHANKAR MENON BY JAYASHANKAR MENON E ding, to a carrier of an entire family of four...Bajaj scooters used to be socialist India’s aspiration. It was India’s car on two-wheels! In fact, when in 2008, Ratan Tata spoke about the need for an ultra-low cost car for the “three-four family mem- bers on a scooter with a kid standing in the front, the guy driving and his wife sitting side saddle holding a little kid,” he was essentially, referring to his school buddy Rahul Bajaj’s company and how millions of his compatriots had virtually grown up on one of the gazillion scoot- ers manufactured by it. However, after reading these lines, if the same millenni- al rushes out to see what this so-called Bajaj scooter looked like, he/she would struggle. It doesn’t matter if the person lived in South Mumbai or rural Bihar. The transition – from start to comple- tion – from scooters to motorcycles hap- pened in a matter of just nine years. Bajaj Auto stopped manufacturing scooters in 2005. Today, its ‘brand new’ scooters have vanished from Indian streets. You might of course find one in an automo- bile museum. Just what happened in these few years? What actually caused India’s aspiration to change suddenly? xplaining what a Bajaj scooter meant to middle-class India to someone born after the mid- 1980s can be a daunting task. From being the default dowry at a wed- The transformation of Bajaj Auto from a geared scooter company to a motorcycle seller, with a focus on exports, is remarkable LUCRATIVE EXPORT INCENTIVES ENSURE THAT BAJAJ AUTO HAS THE HIGHEST OPM AMONG TWO WHEELER MAKERS IN INDIA FALLING IN LINE However, strange it might sound, it in- deed was a fact that in the 60s and the 70s, one had to wait for a decade to get one’s hand on a Bajaj scooter. The rea- son: India’s dreaded License Permit Raj. However, starting the late 80s, the wind changed direction around the world. The iron curtain lifted. The Berlin wall crum- bled. India too, although very hesitating- ly, opened up to market forces. Free market is not just about market, it is about the free human spirit. It’s about a kid learning to say no to his father – no, I won’t stand in front of your scooter. And despite having fought tooth and nail, the then Manmohan Singh-led govern- ment’s plan to open up the economy in 1991, the visionary in Rahul Bajaj, who served as the MD of Bajaj Auto for 35 years before giving it up in 2005, could read the writing on the wall. He could sense that Bajaj Auto’s bread and butter – the geared scooter – will have no place in 24 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 25

GLOBETROTER BAJAJ AUTO torcycles. In the FY2001 letter, he said, “The Company’s motorcycle manufac- turing capacity has expanded to 50,000 per month.” A few months later in No- vember 2001, Bajaj Auto launched what was going to be a game changer – the Pulsar. By the end of FY2002, the un- thinkable had happened – Bajaj Auto had sold more motorcycles in the year than geared scooters! And the beat was actually a landslide. Motorcycle sales in FY2002 had beaten scooter sales by 60%. After this, it was just a matter of time. In FY2004, the company got a new sportier, younger-looking logo. In FY2005, Bajaj Auto sold close to 15x more motorcycles than scooters and by the end of the year, the last scooters were rolling out. Segment-wise total sales of Bajaj Auto Bajaj Auto stopped scooter manufacturing on December 31, 2005 FY2001 FY2002 FY2003 Motorcycles Geared Scooters Rest FY2004 FY2005 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Source: Bajaj Auto Annual Reports ple – focus on exports. And the results were there for everyone to see. In the decade between FY2005 and FY2014, Bajaj Auto’s exports as a percentage of sales, surged from about 10% to over 40%. This meant that while its net sales in the same period went up over three- fold, they were overshadowed by ex- ports that surged by over 11x. This also meant higher margins what with the government providing tons of export in- centives. For example, in FY2014, Bajaj Auto reported Rs.335.94 crore as export incentives. Currently, Bajaj Auto exports to al- most 60 countries. It claims to be the No. 1 or No. 2 in 17 of them and is by far, In- dia’s top exporter of motorcycles. In fact, in FY2014, Bajaj Auto exported over 1.3 million motorcycles – more than 2/3rd of India’s total motorcycle exports. In terms of geographies, Africa in general and Nigeria in particular, seems to have taken a special liking for Bajaj motorcycles. According to Ashwin Pa- til of LKP Securities, “Nigeria accounts for almost 50% of Bajaj Auto’s motorcy- cle exports to Africa, and thanks to the popularity of the Boxer, the company’s pricing power in the Nigerian market is also very high.” Patil’s estimates suggest that Bajaj Auto’s margins in Nigeria are at least 6-7 percentage points higher than its overall margins. Does this mean all’s hunky dory with Bajaj Auto? Not actually. a 3.9% growth – third straight year with over 10 million in sales. It also meant that Bajaj Auto now has just a 20% share in the domestic motorcycle market and has recently been relegated to No. 4 in the overall two-wheeler market as an old quandary comes back to haunt it. “Every 4th two-wheeler sold is a scoot- er,” read the headline of a leading news- paper a few weeks before this issue went to print. The transition of India from an ‘Only-scooter’ two-wheeler market until the early 90s to ‘What’s a scooter’ two-wheeler market in the first decade of the new century, has now turned full circle. While domestic motorcycle sales rose 3.9% in FY14, scooter sales surged by 23% as Indians lapped up new-age scooters from Honda, Piaggio, TVS, Hero Moto and even Suzuki and Mahin- dra. What must be worrisome for Bajaj Auto is the fact that this is not an aber- ration but a trend as scooter sales as a percentage of total two-wheeler sales has consistently risen from 14 in FY2008 to 25 in FY2014, while that for motorcy- cles have dipped from 79 to 70 during the same period. This has not gone un- noticed by Dalal Street as shares of Bajaj Auto have been forced to trade at a dis- count to those of rival Hero MotoCorp, which continues to focus on India. IN FY2014, BAJAJ AUTO’S EXPORT INCENTIVES FELL TO RS.335.94 CRORE VS RS.416.75 CRORE Y-O-Y DUE TO LOWER DUTY DRAWBACKS Bajaj scooters have been life long companions for even many affluent Indians like Ameet Singh, a Voice Over professional based in GREENER PASTURES If one thought with the passing of the baton to Rajiv Bajaj from the ‘scooterwa- la’ father and manufacturing of geared scooters getting relegated to history books, Bajaj Auto’s transformation was complete, one couldn’t have been more wrong. For, things were just warming up. It was a time when the Indian economy was on a tear and the Sensex on fire. The ‘India Growth Story’ had worshipers all around the world. Money was pouring into the country at a rate of knots. The rupee was appreciating on a daily basis and auto sales were hitting the roof. Ra- jiv Bajaj, however, contrary to popular wisdom, was looking at foreign shores as Bajaj Auto’s exports crossed the quarter million mark in FY2006. From thereon, the strategy was sim- Hyderabad free-market India. He knew it was time for a transition. But he perhaps didn’t know what to do. Luckily for Rahul Bajaj, the transition of India’s two-wheeler market took a few years and gave him the breathing space to build capacities. But by the turn of the century, the market had turned on its head. Rahul Bajaj noted in his annual let- ter to shareholders in the year 2000, “The structure of the two-wheeler market is changing at a rapid pace. Younger peo- ple and those with significantly greater purchasing power now constitute an im- with geared scooters? Observers claim that time seems to have run out for Ba- jaj Auto. According to Patil, “Setting up a 30,000/month scooter manufacturing unit will cost close to Rs.1,000-1,200 crore but more importantly, the com- missioning will take at least 24 months.” Bajaj Auto has lived India’s change. A look at its TVCs (from those popular jingles of the 80s trying to create an emo- tional bond with the buyer to the current ones that are more about specification) confirm this. And one would do well not betting against a company that has re-in- vented itself over and over again. Does it mean a new chapter is being quietly scripted in the corner office at the Bajaj Auto headquarters? The future of Bajaj Auto could be different. It could be about ‘also scoot- ers’. As much as we know Rajiv, he loves yoga and wants to grow his company in- side-out. We also know that he led the re- making story of Bajaj a decade back. No reason to believe therefore why he can’t adopt a top-down, organic approach to making change occur in Bajaj Auto’s build-and-sell strategy again. Only issue is, he doesn’t have nine years to decide and act. Not this time. portant segment of the market. The writ- ing is on the wall. Over the last five years, we have faced a stagnant, even declining market for our mainstay – the tradition- al, metal bodied, side-engine mounted, kick-start scooters.” However, not the one to throw in the towel, he ended the letter promising “rapid ramping up of ca- pacities for motorcycles...” THE TRANSITION Over the next five years, in every sin- gle annual letter to shareholders, Rahul Bajaj was seen pressing his case for mo- Growth rate of exports and net sales (%) Bajaj’s exports have risen almost 12x in the last 10 years Export as a percentage of sales Bajaj Auto’s total exports were worth Rs.8,199 crore in FY2014 45 12 40 10 35 RECONCILING AGAIN While Rajiv Bajaj continues to bet on motorcycles and seem to have turned his back on scooters forever, he would do well to learn from what his father did in the 90s and early part of the last de- cade. Can we even imagine what would have happened if Rahul Bajaj had not reconciled to the changing dynamics of the market in the 90s and continued 30 8 25 6 20 15 4 SCOOTER HAUNT With almost its entire focus on exports, Bajaj Auto is losing domestic market share by the day. Its domestic motorcy- cle sales fell by almost 15% in FY2014. This, when the motorcycle industry saw 10 2 5 0 0 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Net Sales Value of Exports Volume Value jay@thedollarbusiness.com Source: Bajaj Auto Annual Reports Source: Bajaj Auto Annual Reports 26 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 27

BIG IDEA WHAT? WHERE? WHY? BIG IDEA WHAT? WHERE? WHY? TIME TO LEARN FROM ANCIENT MARINERS Recent political turmoil notwithstanding, Indonesia has been an economic success story over the past couple of decades. Early to embrace liberalisation and foreign capital, the country was badly bruised during the East Asian Financial Crisis. However, since then this archipelago of 13,466 islands has seen a very stable but high growth rate. If that doesn’t make Indonesia an attractive destination for Indian exporters, millennia old trade ties and the in the last two years, Indonesia has turned a net importer (from almost always running a trade surplus) surely do BY DR. A. K. SENGUPTA Pura Ulun Danu Bratan, or Pura Bratan, located at the edge of Lake Bratan, is a famous Hindu and water temple in Bali, Indonesia. Several such temples in Indonesia are a testimony to the 2000-year-old India-In- donesia bilateral trade and cultural relationship 28 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 29

BIG IDEA WHAT? WHERE? WHY? I Europeans arrived in Indonesia in the 16th century seeking to monopolise the commercial trade of commodities like spices. It was initially the Dutch in 1602, who established “The Dutch East India Company” and became the dominant European power in the region. The Jap- anese invasion and subsequent occupa- tion of the island nation during World War II ended the Dutch rule. The Japa- nese surrender in 1945 and subsequent developments heralded Indonesia’s in- dependence and national leaders like President Sukarno and General Suharto chartered a new course of economic and trade policies designed to help the island nation develop its true potential. It was in fact the dispensation of the “New Or- der Administration” policy brought into force by General Suharto that spurred investment from the Western nations and brought into focus the role of foreign investment as an engine of economic ad- vancement of the country. The late 1990s, however, witnessed a major setback to the rapidly growing In- donesian economy when it was hit hard by the escalating East Asian Financial Crisis. In the aftermath of the crisis, the government took custody of a significant portion of private sector assets through Indonesian merchandise trade The country posted trade deficit for the first time in CY2012 India-Indonesia trade India’s trade deficit with Indonesia widens as coal imports rise ndonesia comprises a group of is- lands stretching along the equator in South East Asia. The country’s strategic location fosters both in- ter-island and international trade. The acquisition of non-performing bank loans and corporate assets through debt re-structuring processes. Since 1998, the economy has seen an upswing, with sta- ble growth of 4-6%. ico, Indonesia, Nigeria and Turkey – it is an attractive investment destination due to favourable demographics. 250 16,000 14,000 INDUSTRIAL INDONESIA The industrial sector contributes 47% to the GDP of Indonesia. The two most important sub-sectors of the Industry in the country are mining and manufactur- ing – two pillars of the nation’s economy since the 1970s and the major engines of economic change and development during Suharto’s ‘New Order’ regime. Al- though the manufacturing sector seems to have lost its momentum after the Asian Crisis, it still is the most popular sub-sector in terms of attracting FDI and is followed by mining. Indonesia’s min- ing and manufacturing products include coal, oil, gold, automobiles, electronics, footwear, textile products, paper prod- ucts and furniture items. The first decade after the Asian cri- sis saw the industrial sector go through multiple periods of recession as foreign investors stayed away. However, success- ful navigation through the GFC saw for- eign investors regaining their confidence due to robust domestic demand spurred 200 12,000 10,000 THROUGH THE FLU Although Indonesia is regarded as a market economy, the government owns significant amount of the industrial base following the 1997 financial crisis. In fact, the successful structural reform, which followed the 1997 crisis, helped Indonesia escape the 2008 GFC (global financial crisis) almost unscathed. Since peaking in 2005, Indonesia’s unemploy- ment rate has also seen a perceptible de- cline. Concerns about runaway inflation have also ebbed, with inflation rate run- ning at around 4-5%. The nation’s debt- to-GDP ratio has also steadily declined from 83% in 2001 to less than 26% by the end of 2013 – the lowest among ASEAN countries, apart from Singapore, which has no government debt. Indonesia’s GDP per capita has risen almost five-fold in the past 50 years. Foreign trade has played an important role in this remark- able achievement. In the past 25 years, trade as a share of GDP has increased specifically, partly due to the country’s outward-oriented development strategy. Already ranked among the larger econo- mies in the world, Indonesia offers enor- mous promise for global investors. An integral component of the MINT – Mex- 150 8,000 100 6,000 4,000 50 2,000 0 0 CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Exports Imports Exports Imports Source: International Trade Centre; figures in $ billion Source: Ministry of Commerce, GoI; figures in $ million by a growing middle-class, low wages and a promising future. decline. The creation of the ASEAN Free Trade Area (AFTA), which encourages trade within the Asian region, is another factor that has given a directional shift to Indonesia’s trade patterns. Indonesia has almost always had a trade surplus in merchandise trade, with large exports to China, Japan, Singapore, Malaysia and US. But rising consumer- ism, thanks to a burgeoning middle class with high disposable incomes, has en- sured that Indonesia has recorded trade deficits to the tune of $1.63 billion and $4.06 billion in CY2012 and CY2013 respectively from an average surplus of $25.8 billion in the preceding five years. TRADE TRANSITION Till the 1970s, Japan was Indonesia’s dominant trade partner accounting for over 40% of its exports (mainly petro- leum) and 25% of imports. Although Ja- pan still remains a major partner, other nations have emerged in recent years. However, trade with Netherlands, which was of primary importance in colonial years when Indonesia was known as the Dutch East Indies, has shown a steady AS OLD AS THE EPICS Every year in the eastern Indian state of Odisha, a unique festival called ‘Baliya- tra’ or ‘Boita Bandano’ is celebrated with great spirit and fervour. Literally meaning ‘Voyage to Bali’, the festival is celebrated to mark the day when ancient Odia mar- iners would set sail to Bali, Java, Sumatra and Borneo (all in Indonesia). Similarly, in Bali, ‘Masakapan Ke Tukad’ festival is celebrated and like what is done in Odi- Top imports by Indonesia from India Mineral fuels, chemicals and cereals are Indonesia’s main imports from India 700 600 500 400 300 Porters unloading sacks of cement at a beach on Gili Trawan- gan island, a small island just off the north- west coast of Lombok, Indonesia. It’s an ideal destination for tourists looking for a remote island experience 200 100 0 A* B C D E F G H I J FY2013 FY2014 A) Mineral Fuels, Oils, Waxes; B) Organic Chemicals; C) Cereals; D) Nuclear Reactors, Boilers, Machinery; E) Oil Seeds, Medicinal Plant, Straw & Fodder; F) Auto & Auto Ancillary; G) Iron & Steel; H) Cotton; I) Electrical Machinery & Equipment; J) Residues and Waste from Food Industry Source: Ministry of Commerce, GoI; Imports of $1.49 billion in FY2013 vs. $1.54 billion in FY2014; Other figures in $ million 30 THE DOLLAR BUSINESS II AUGUST 2014 AUGUST 2014 II THE DOLLAR BUSINESS 31