Download

1 / 5

50 likes | 73 Views

<br>This Tax Alert summarizes the Delhi Tribunal Special Bench (SB) ruling dated 16 June 2017 in the case of Vireet Investment Pvt. Ltd.For more info visit:-<br><br>http://www.ey.com/in/en/services/ey-goods-and-services-tax-gst<br>

E N D

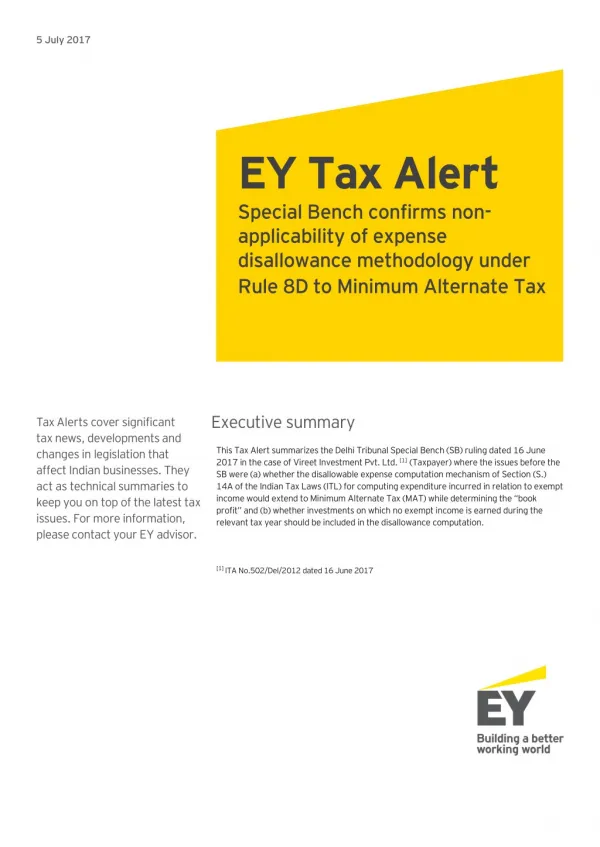

5 July 2017 EY Tax Alert Special Bench confirms non- applicability of expense disallowance methodology under Rule 8D to Minimum Alternate Tax Executive summary Tax Alerts cover significant tax news, developments and changes in legislation that affect Indian businesses. They act as technical summaries to keep you on top of the latest tax issues. For more information, please contact your EY advisor. This Tax Alert summarizes the Delhi Tribunal Special Bench (SB) ruling dated 16 June 2017 in the case of Vireet Investment Pvt. Ltd. [1] (Taxpayer) where the issues before the SB were (a) whether the disallowable expense computation mechanism of Section (S.) 14A of the Indian Tax Laws (ITL) for computing expenditure incurred in relation to exempt income would extend to Minimum Alternate Tax (MAT) while determining the “book profit” and (b) whether investments on which no exempt income is earned during the relevant tax year should be included in the disallowance computation. [1] ITA No.502/Del/2012 dated 16 June 2017

On the first issue relating to MAT, noticing the conflict of views expressed by the jurisdictional Delhi High Court (Delhi HC) in the earlier case of Goetze India Ltd. [2] (in favor of Tax Authority) and later in the case of Bhushan Steel[3] (in favor of taxpayer, but without noticing the earlier Goetze ruling), the SB preferred to follow the later ruling favoring the taxpayer. For this, the SB relied on the Supreme Court (SC) ruling in the case of Vegetable Products Ltd[4]. Accordingly, the SB held that while expenditure relatable to income that is exempt under both normal and MAT computation, needs to be added to “book profit”, the computation mechanism of S. 14A disallowance relevant to normal computation cannot be applied while computing book profit under MAT provisions. The MAT disallowance has to be based on expenditure debited to Profit & Loss Account (P&L). Background •The Finance Act, 2001 inserted S.14A in the ITL, with retrospective effect from 1 April 1962 i.e., from the date of inception of the ITL. The Section provides that, for the purposes of computing total income under Chapter IV of the ITL, no deduction shall be allowed in respect of expenditure incurred by a taxpayer, in relation to exempt income. •The Finance Act, 2006 further amended S.14A with effect from 1 April 2007 to provide that the amount of disallowance will be computed as per the prescribed methodology where the Tax Authority is not satisfied with the taxpayer’s claim or where the taxpayer claims that no expenditure has been incurred by it in relation to exempt income. The Central Board of Direct Taxes (CBDT) prescribed the methodology by inserting Rule 8D in the Income tax Rules with effect from 24 March 2008. On the second issue relating to normal tax computation, having regard to Delhi HC rulings in cases of Holcim India Pvt. Ltd. [5] and Cheminvest Ltd. [6] which held that disallowance under S.14A does not apply to investments on which no exempt income is earned during the tax year under reference, the SB held that such investments should also be excluded while computing disallowance as per the normative methodology prescribed in the Income Tax Rules. •Rule 8D[7], as applicable to the year under reference, prescribed the computation of disallowance under three limbs viz. (a) Direct expenditure (b) Indirect interest expenditure computed on pro-rata basis in proportion of average value of investments to the total assets and (c) 0.5% of the average value of investments. The investments which need to be considered for this purpose are those investments, income from which “does not” or “shall not” form part of total income. •The MAT provisions apply to a company and provide for taxation based on “book profit”. Taxation under MAT provisions is triggered when tax liability, computed at specified percentage[8] of “book profit” under MAT, is higher than tax liability under the normal computation. •The “book profit” is computed by adopting the net profit as per P&L prepared in compliance with the relevant provisions of the Companies Act and further adjusting it by additions and reductions as specified under the MAT provisions. The MAT provisions, inter alia, contain downward adjustment for specified exempt incomes[9] credited to P&L and upward adjustment for expenditure “relatable to” such exempt income debited to P&L. [7]Rule 8D has been amended w.e.f. 2 June 2016 and prescribes disallowance under two limbs viz. (a) Direct expenditure (b) 1% of the average value of investments and further that, the disallowance under both the limbs shall not exceed the total expenditure claimed by the taxpayer - Refer EY Tax Alert dated 8 June 2016 titled “CBDT notifies new method for computation of expenditure incurred for earning exempt income” [8]Currently 18.5% [9]Except long-term capital gains on securities which are liable to Securities Transaction Tax (STT) [2](2014) 361 ITR 505 (Del) [3]ITA No. 593/2015 dated 8 October 2016 [4](1973) 88 ITR 192 (SC) [5](2014) 272 CTR 282 (Del) [6](2015) 378 ITR 33 (Del) - Refer EY Tax Alert dated 8 September 2015 titled “Delhi HC rules no disallowance of interest expenditure absent exempt dividend income received during tax year”

Facts as exempt income and then again claiming deduction of expenses related to exempt income against the taxable income. •MAT provisions also require reduction of specified exempt incomes from “book profit” and addition of expenditure “relatable to” such exempt income. Although this is similar to disallowance in the normal computation, the computation methodology of normal computation cannot be imported into MAT provisions. •The Taxpayer was engaged in the business of finance and investment and thereby, making investments in shares and securities and advancing moneys and borrowing moneys to/from industrial enterprises. •For the tax year 2007-08, the Taxpayer earned exempt income viz. dividends, interest and long term capital gains. The Taxpayer offered expenditure relatable to exempt income for disallowance under the third limb of Rule 8D (@ 0.5% of average value of tax-free investments) but by including only those investments which actually yielded exempt income during the tax year under reference and excluding investments which did not yield any exempt income. While it is not clear from the ruling, it appears that the Taxpayer adopted similar methodology for computing disallowance under MAT provision. •It is legitimate and proper to read similar provisions in different parts of the statute in their own context having regard to the legislative intent of their incorporation. The legislative intent must be found out by reading the statute as a whole. •It cannot be disputed that addition of expenditure “relatable to” exempt income in MAT computation is in conformity with the matching principles of accounting whereby if income is excluded, the related expenditure should also be excluded. •The Tax Authority’s view that, while computing book profit, the reduction of expenditure “related to” exempt income should be the same as is considered in normal computation is supported by Delhi HC ruling in the case of Goetze India Ltd. (supra) .In Goetze’s case, the taxpayer’s counsel fairly conceded that disallowance under S.14A was required to be made while computing “book profit” in MAT computation. •The Tax Authority re-computed the disallowance by including the value of investments from which no exempt income was earned during the year. Moreover, the Tax Authority adopted the same computational methodology as per Rule 8D while determining “book profit” under MAT. •The First Appellate Authority upheld the Tax Authority’s view on the above issues. •However, the Taxpayer’s view is supported by another subsequent ruling in the case of Bhushan Steel (supra) where the HC held that disallowance under S.14A cannot be imported in MAT computation. Unfortunately, while delivering this ruling, the earlier adverse ruling in Goetze’s case, which had equal strength of judges, was not noticed. Hence, there arises a situation where there are two conflicting rulings of the same HC of equal strength but the later ruling has not noticed the earlier ruling. In such a situation, as per the Delhi HC ruling in the case of Bhika Ram v. UOI[10], the later ruling should be followed even if it did not consider the earlier ruling. •In this background, the following issues arose for consideration before the SB: •Whether the methodology of computing disallowance as per Rule 8D can be applied to MAT computation while determining “book profit”? •Whether investments on which no exempt income is earned during the relevant tax year should be included in disallowance computation? SB ruling •It is improper for a lower court to treat any decision of a higher court as incorrect. The proper course for the lower court is to follow the ratio of the SC ruling in the case of CIT v. Vegetable Products Ltd.[11] which held that if two reasonable constructions of a taxing provision are possible, the construction which favors the taxpayer must be adopted. In view of this decision, the present issue needs to be resolved in Taxpayers’ favor by holding that the computational provisions of disallowance under S.14A applicable to normal computation cannot be applied while computing “book profit” under MAT provisions. Non-applicability of computational methodology of S. 14A to MAT computation The SB ruled in Taxpayer’s favor and held that the computational methodology of S.14A as per Rule 8D cannot be applied to computation of “book profit” under MAT for the following reasons: •MAT taxation is a complete code in itself and was introduced with the object to rope in companies which were not paying any taxes to pay tax on the basis of “book profits” as per the deeming provisions contained therein. The starting point for computation is the net profit as per P&L followed by additions to and reduction of specified adjustments. [10](2000) 238 ITR 113 (Del) [11](1973) 88 ITR 192 (SC) •S. 14A was inserted to deny double deduction to taxpayers i.e., firstly by claiming the gross income

Exclusion of investments not giving rise to exempt income during the year under reference Comments The SB ruled in Taxpayer’s favor and held that the computational methodology of S.14A as per Rule 8D cannot be applied to computation of “book profit” under MAT for the following reasons: The SB ruling is beneficial for taxpayers as it confirms that computational provisions of S.14A applicable to normal computation cannot be applied to “book profit” computation under MAT which will need to be computed on an independent basis as per the expenses debited to P&L. On this issue, amidst the conflict between the two jurisdictional HC rulings of equal strength, the SB preferred to follow the view in favor of the Taxpayer. •Under the Constitution of India, the subordinate courts function under the supervisory jurisdiction of the Honourable High Court. It is well settled that the decisions rendered by a jurisdictional High Court are binding on all subordinate courts working within its jurisdiction. •The jurisdictional Delhi HC in the case Holcim India Pvt. Ltd.(supra) held that S. 14A could not be invoked if no dividend income was earned during the year under reference. Such is also the view expressed by other HCs in several cases. On the second issue also, the SB ruling favors the Taxpayer by holding that investments which have not yielded any exempt income during the year need to be excluded while computing the disallowance. This is in supersession of the earlier contrary view expressed by the SB in the case of Cheminvest Ltd.(supra) and is also against the view currently held by the Tax Authority through its Circular No. 21/2015 dated 10 December 2015. •The said ruling was followed by the ruling of the Delhi HC in the case of Cheminvest Ltd.(supra) after considering the ratio of the SC ruling in the case of Rajendra Prasad Moody which had held that it is not necessary that an expenditure should actually result in producing income in order to be eligible for deduction. The Delhi HC distinguished this ruling on the ground that it was concerned with the allowance of deduction for expenditure which does not yield any income whereas S.14A is concerned with allowability of expense which yields exempt income. Rajendra Prasad Moody’s ruling cannot be interpreted in reverse to infer that if no income is earned, the expenditure can be disallowed. As per judicial convention, SB ruling is binding on all other benches of the Tribunal. •It is true that Rule 8D also refers to those investments, income from which “shall not” form part of the total income. But there is uncertainty on whether a particular investment will always yield exempt income in future. This is because, as a result of amendments in laws, income may not remain exempt income; but may become taxable. •Hence, only those investments which yield exempt income during the year are to be considered for computing the average value of investment.

Ernst & Young LLP EY | Assurance | Tax | Transactions | Advisory Our offices About EY EY is a global leader in assurance, tax, transaction andadvisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promisesto all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. Ahmedabad 2nd floor, Shivalik IshaanNear C.N. Vidhyalaya Ambawadi Ahmedabad - 380 015 Tel: + 91 79 6608 3800 Fax: + 91 79 6608 3900 Bengaluru 6th, 12th & 13th floor “UB City”, Canberra BlockNo.24 Vittal Mallya Road Bengaluru - 560 001 Tel: + 91 80 4027 5000 + 91 80 6727 5000 + 91 80 2224 0696 Fax: + 91 80 2210 6000 Ground Floor, ‘A’ wingDivyasree Chambers # 11, O’Shaughnessy Road Langford GardensBengaluru - 560 025 Tel: +91 80 6727 5000 Fax: +91 80 2222 9914 Chandigarh 1st Floor, SCO: 166-167 Sector 9-C, Madhya Marg Chandigarh - 160 009 Tel: +91 172 331 7800 Fax: +91 172 331 7888 Chennai Tidel Park, 6th & 7th Floor A Block (Module 601,701-702) No.4, Rajiv Gandhi Salai Taramani, Chennai - 600 113 Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120 Delhi NCR Golf View Corporate Tower BSector 42, Sector Road Gurgaon - 122 002 Tel: + 91 124 464 4000 Fax: + 91 124 464 4050 3rd & 6th Floor, Worldmark-1 IGI Airport Hospitality District Aerocity, New Delhi - 110 037 Tel: + 91 11 6671 8000 Fax + 91 11 6671 9999 4th & 5th Floor, Plot No 2B Tower 2, Sector 126 NOIDA - 201 304 Gautam Budh Nagar, U.P. Tel: + 91 120 671 7000 Fax: + 91 120 671 7171 Hyderabad Oval Office, 18, iLabs Centre Hitech City, Madhapur Hyderabad - 500 081 Tel: + 91 40 6736 2000 Fax: + 91 40 6736 2200 Jamshedpur 1st Floor, Shantiniketan Building Holding No. 1, SB Shop Area Bistupur, Jamshedpur – 831 001 Tel: +91 657 663 1000 BSNL: +91 657 223 0441 Kochi 9th Floor, ABAD Nucleus NH-49, Maradu PO Kochi - 682 304 Tel: + 91 484 304 4000 Fax: + 91 484 270 5393 Kolkata 22 Camac Street 3rd Floor, Block ‘C’Kolkata - 700 016 Tel: + 91 33 6615 3400 Fax: + 91 33 2281 7750 Mumbai 14th Floor, The Ruby 29 Senapati Bapat Marg Dadar (W), Mumbai - 400 028 Tel: + 91 22 6192 0000 Fax: + 91 22 6192 1000 5th Floor, Block B-2 Nirlon Knowledge Park Off. Western Express Highway Goregaon (E) Mumbai - 400 063 Tel: + 91 22 6192 0000 Fax: + 91 22 6192 3000 Pune C-401, 4th floor Panchshil Tech Park Yerwada (Near Don Bosco School) Pune - 411 006 Tel: + 91 20 6603 6000 Fax: + 91 20 6601 5900 EY refers to the global organization, and may refer toone or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in. Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata - 700016 © 2017 Ernst & Young LLP. Published in India. All Rights Reserved. This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. Onany specific matter, reference should be made to the appropriate advisor. Join India Tax Insights from EY on EY refers to global organization, and/or one or more of the independent member firms of Ernst & Young Global Limited