Treasury Organisation

Treasury Organisation. Treasury Organisation. Agenda Centralised vs Decentralised Payment factories Collection factories Re-invoicing centre Factoring centre In House Bank Shared service centre. Treasury Organisation. Move towards centralisation of Treasury

Treasury Organisation

E N D

Presentation Transcript

Treasury Organisation • Agenda • Centralised vs Decentralised • Payment factories • Collection factories • Re-invoicing centre • Factoring centre • In House Bank • Shared service centre

Treasury Organisation • Move towards centralisation of Treasury • Developments in technology, ERP and TMS • Regulatory environment and good governance • Different levels Geographic Product line or business division Customer type, e.g. corporate/consumer Policy making

Treasury OrganisationInfluencing Factors • Size of company • Industry norms e.g. retail sales distribution vs decentralised manufacturing • Nature of cash flows e.g. electronic vs paper • Geographic distribution, time zones, communications

Treasury OrganisationInfluencing Factors • Business culture e.g. active acquirers • Use of technology • Location of expertise • Need for control

Treasury Organisation Disadvantages of a decentralised organisation • Inability to leverage economies of scale • Duplication of functions • Many different systems to support • Cash management activities e.g. netting, interco lending etc may not be possible • Loss of visibility of information resulting in delayed or incomplete reporting • Lack of control for risk and liquidity management Recommended reading: The pros and cons of Treasury Centralisation, Gtnews Feb, 2010

Treasury Organisation Disadvantages of a centralised organisation • Loss of autonomy and ownership of results by business units • Local vendor and bank relationships will suffer locally • Need for increased communication and coordination with head office • Lower morale/lack of interest in operating units due to reduced responsibilities and concerns about job losses

Treasury Organisation • Central policy, local execution • Centralised execution • Regionalised execution, central policy

Treasury OrganisationRegional • Why manage in the region? • Time zones/contact time/cut-off times • Same day value • Local expertise • FX markets/environment • Potential tax savings • Better pricing • Lower staff costs

Treasury OrganisationPayment Factories • Central facility set up to handle a group’s payment orders. Accounts payables function may continue to be handled at local level. • Gather payment instructions into one file • Single electronic gateway • Covers central bank reporting • Handles inter-company transactions • Receives all account and transaction information from the bank(s) and distributes to subs for reconciliation.

Treasury OrganisationPayment Factory • Significant cost savings from reduction in number of banks • Reduction in overall cost of payments • Centralised handling of FCY payments • Cross border payments can be re routed and re formatted as domestic • Use of lower cost ACH • For subs, new business does not necessarily mean new bank accounts • Better security and more accurate cash flow forecasting • Central information can lead to better liquidity and risk management

Treasury OrganisationCollection Factory • Same concept as Payment Factory applied to collections BUT • May or may not give the same benefits • Will depend on nature of the accounts receivable and location of accounts. Think about small value, high volume cross border. May be issues for customers paying into accounts not owned by the payee.

Treasury OrganisationRe-invoicing Centre • Subsidiaries buy and sell in their own currency from the central treasury or in house bank • FX risk is transferred to the re-invoicing centre • Enables leading of payments to cash poor subsidiaries

Treasury OrganisationFactoring • Subsidiary sells to sister company (or third party) • Sells invoice to in house factoring company • Allows subsidiary to fund itself and removes FX risk to centre • Payment due is made direct to factoring centre

In House BankIHB • An IHB is a vehicle where group treasury acts as the primary source of all banking services to operating units at arms length • Transacts aggregated business with ‘real’ banks • May be part of centralised or decentralised structure

IHBAdvantages • Economies of scale • Reduces bank margins and costs • Cash Management techniques e.g. netting, cash pooling, intra group funding • Reduces number of bank transactions • Treasury professionals • Profit centre?

IHBDisadvantages • Group still reliant on local staff • Cash forecasts to identify future surpluses and deficits • To identify currency exposures • To ‘play the game’ • To actually carry out transactions • Reduces local involvement and commitment • Local banks lose business

IHBFunctions • Liquidity management • Cash pooling • Netting (cashless) • Inter-company loans and deposits • In house factoring • Re-invoicing • Risk management (matching) • Advice and consultancy • Long term funding and investments

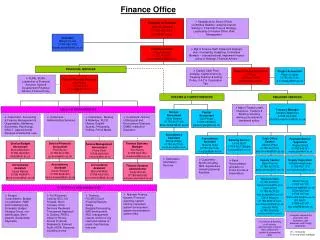

IHBTypical Structure Sub-accounts for subsidiaries Sub-accounts for subsidiaries Belgium HK UK USA Belgium HK UK USA - Control - Bookeeping - Interest calcs - Statements Sub-accounts for subsidiaries Sub-accounts for subsidiaries Belgium HK UK USA Belgium HK UK USA IHB EUR A/c In Brussels IHB HKD A/c in Hong Kong Central Treasury IHB USD A/c In New York IHB GBP A/c In London

Shared Service Centre • Shared service centre acts as a single business unit that performs common finance and administrative functions • Delivers services to subs or other business units regulated by service level agreements

Shared Service CentreFunctions • Human resources • Facilities management • Procurement • Internal audit • marketing • Travel arrangements • Tax and so on and so on

Shared Service CentreCash Management Functions • Bulk payments, especially international • Local in country paper collections • E-commerce applications e.g. einvoicing • Foreign exchange processing • Account reconciliation • Trade finance • Tax