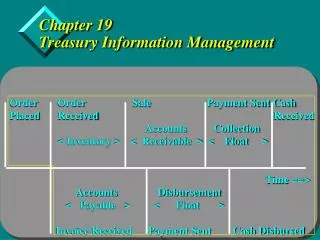

Treasury Management

Carolinas Cash Adventure 2011. Cash Forecasting Versus Predictive Modeling. Treasury Management. May 17, 2011. Craig S. (“Sandy”) Saxer Senior Vice President PNC Bank. Cash Forecasting. Forecasting is a process where businesses adjust future expectations based on recent actual

Treasury Management

E N D

Presentation Transcript

Carolinas Cash Adventure 2011 Cash Forecasting Versus Predictive Modeling Treasury Management May 17, 2011 Craig S. (“Sandy”) Saxer Senior Vice President PNC Bank

Cash Forecasting Forecasting is a process where businesses adjust future expectations based on recent actual performance and conditions.

Cash Forecasting • “Show me the money…! • How much is reasonably achievable? • Lack of accuracy and predictive assessment • Economic instability increases demand for better cash forecasts for better executive decisions, but at the same time makes accuracy more elusive • Required incremental investment versus results… a slippery slope! • Limited treasury resources and recent events force new views of cash forecasting to include visibility and variability… • Hence Predictive Modeling… a method to manage around the target without having to achieve perfection, but producing a high degree of accuracy for decision-making purposes

The Current State of Cash Forecasting • Importance of current and expected liquidity • Availability of short term funding, and • Funding costs • Managing internal working capital • Traditional Reliance on stable trading patterns and historic partner actions is suspect in the new economic climate • Other systemic changes have been creeping into forecasts for some time… • USPS first class mail delivery changes • Acceleration of Consumer electronic payments • Image Exchange • Card usage • Global business perspective • Most Corporate Treasuries use spreadsheets and other fragmented, non-integrated tools • Accounting systems focus on “book” versus “available in the bank”… • International balances often lack current visibility • Effective cash forecast horizons are limited • Limited treasury resources are available… 20+ years of corporate restructuring have taken their toll!!

Why Better Cash Forecasting? • Focus on agility and the need to build confidence for strategic decisions • Best-in-Class (top 20%) cash forecasts have 36% better forecasting accuracy than laggard (bottom 30%) companies (1) • Top performing companies surveyed made 20% gains in profitability through better forecasting (1) • Identify and Control Risk • Dynamically account for change • Linking forecasts with strategic and tactical plans to provide competitive advantage (1) Financial Planning Budgeting & Forecasting, Aberdeen Group, February 2010

Treasury Technology for Modeling • Interest in ERP and Treasury Workstations has “morphed” from cash flow accounting to visibility and improved forecasting • New challenges like “XBRL” and International Financial Accounting Standards are increasing the demand for automation and access to information for dynamic decisioning • Use of Spreadsheets (90%) • Stand-alone applications (45%) • Invest in applications that provide flexibility and visibility to forecasts • Dynamic planning is enabled through process, organization, knowledge management, technology and performance management • Example vendors: Amdocs (Clarify), PeopleSoft CRM, SAS, Teradata CRM, Unica Affinium

Methods of Cash Forecasting • Direct Cash Forecast…Detailed build-up… e.g. ERP approach using automation • Indirect Cash Forecast… FAS 95 … work from net operating income and adjust for non-cash items • 80-20% Rule (Pareto’s Law)… efficiency is gained by eliminating transaction bulk for significance… D. McCann, “For Good Forecasts, Use the 80-20 Rule”, CFO.com, June, 2009 • The “Bucket” Theory… segments cash flows by relative impact and predictability • Exponential Smoothing- “periodicity” … M. Hunstad, PhD “Cash Flow Forecasting” AFP Exchange, January February 2010 • Predictive Modeling- agility

Uses ERP details that are subject to auditing and review Historical basis Ties to books and records Provides details for analysis Can be used to provide comparative analysis… forecast versus actual experience Promotes standardization of forecasting methodology Complex; treasury staff- intensive Not readily adaptive in the event of changes Reflects book, not banking system cash Requires costly integration and external data input Forecast Reporting is often fixed in format and information Can not be easily programmed to “learn” from prior variances Limited ability to vary assumptions and create scenarios Detailed Build-Up Approach Pro Con

Uses reported Net Operating Income Actual basis Adjusts for non-cash and working capital changes Often uses business unit input Useful for mid- to long term planning horizons Provides standardization of forecasting methodology Relatively straight-forward; not treasury staff- intensive Not readily adaptive in the event of changes Reflects book, not banking system cash Limited predictive value Does not provide detail and is more difficult to roll forward Can not be easily programmed to “learn” from prior variances Requires assumptions Indirect Cash Flow- Accounting Method Pro Con

Focus on top 80% of cash forecast drivers Avoid costly attempts to achieve perfection Apply scarce treasury resources to maximum advantage Emphasis on comparative analysis Elimination of detail- avoid “forest for the trees” syndrome Improve communication and participation through a simpler, more readily understood process Less precision= less confidence Obtaining cooperative interaction Dependency on timely and accurate communications Increased risk of missed trend, especially in smaller components of the business Less suited to multiple entities Still requires a great deal of real time data 80-20 Rule Approach Pro Con

The “Bucket” Theory Alternative to Forecasting A Hybrid… Items > $50,000 Specific ID, Tracking Items $5-$50,000 Aggregates of Sub groups Items <$5,000 Statistical Smoothing

Exponential Smoothing- Periodicity Final Forecast Periodic Components Raw Cash Flow data Forecast of Residential Components Residential Components Source: M. Hunstad, PhD “Cash Flow Forecasting” AFP Exchange, January February 2010

Adding to the Complexities • Policy Issues of Greatest Concern • Sources: Estimates based on Various News and Articles

The Case for Predictive Modeling • Market volatility creates the need to dynamically account for change • More decision-makers must be involved in the process • Ability to re-forecast as conditions move • Capability to perform “what-if” scenarios • Gaining the planning process involvement of those accountable for the delivery of performance • Communication and integration of forecasts with budgets and other plans • Ability to model impacts of assumptions made • Development of “best” and “worse” case alternatives

Perspective: Components of Forecasting Information Sources and uses Direct data and its use Model Data- assumptions and validation People Roles and problems Automation What it does well What it does not do well Degree of accuracy desired versus required- expectations! Liquidity, Liquidity Achieving a balanced approach: Best Expected Worst

Build Your Effective Cash Forecasting Process • Understand the uses and Users of your forecasts • Identify and dedicate resources to your cash forecasting process • Identify enterprise cash flows and who manages them • Schedule known, non-daily cash flows (e.g. maturities, payroll, tax settlements, etc) • Establish control over outflows… making prediction a “reality” • Perform Regular variance analysis • Use weighting as a form of “smoothing” • Forecasting Agility… use assumptions with dynamic qualities to adjust and change quickly • Manage data around an accuracy target- set expectations of reasonable accuracy among the users of the forecast • Simplify structural components affecting your forecasts

Summary • Working capital management is a vital and growing aspect of Treasury • Liquidity and counterparty risk assessment are wide-spread terms now – what plans has your treasury function for this? • Determine what will change your forecasts as well as what drives your forecast • Prepare “Best” and “Worst” case scenarios in addition to the “Norm” • Be sure to perform periodic comparative analysis… and “stress test” your assumptions! • Tighter Cash Forecasting is the buzz… perhaps we should more carefully consider the strategic notions linking data analysis and scenario modeling for the future… hence Predictive Modeling!

Questions? PNC Financial Services Group