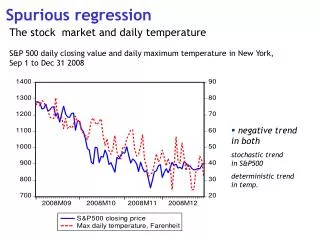

Understanding Spurious Regression Through Simulated Data Generation Processes

This example illustrates a data generation process demonstrating spurious regression. By generating two time series, Y and X, using autoregressive relationships and random noise, we reveal how these series can appear correlated despite lacking a causal link. The procedure involves iterating through time points, applying defined parameters (alpha, beta), and outputting results for analysis. Knowing this phenomenon is vital for correctly interpreting statistical relationships in time series data.

Understanding Spurious Regression Through Simulated Data Generation Processes

E N D

Presentation Transcript

Data Generation Process • new; • format /m1 /rd 9,3; • apha=3; beta=1; • T=100; • Y=zeros(T,1); • X=zeros(T,1); • e1=Rndn(T,1); • e2=Rndn(T,1); • @ Data Generation Process @ • Y[1,1]=0; X[1,1]=0; • i=2; • do until i>T; • Y[i,1]=apha+beta*Y[i-1,1]+4*e1[i,1]; • X[i,1]=apha+beta*X[i-1,1]+2*e2[i,1];

i=i+1; • endo; • Output file=d:\Enclass\Spus\level.out reset; • Y~X; • Output off; • Output file=d:\Enclass\Spus\Diff.out reset; • (Y[2:100,1]-Y[1:99,1])~(X[2:100,1]-X[1:99,1]); • Output off;