Download

1 / 60

600 likes | 604 Views

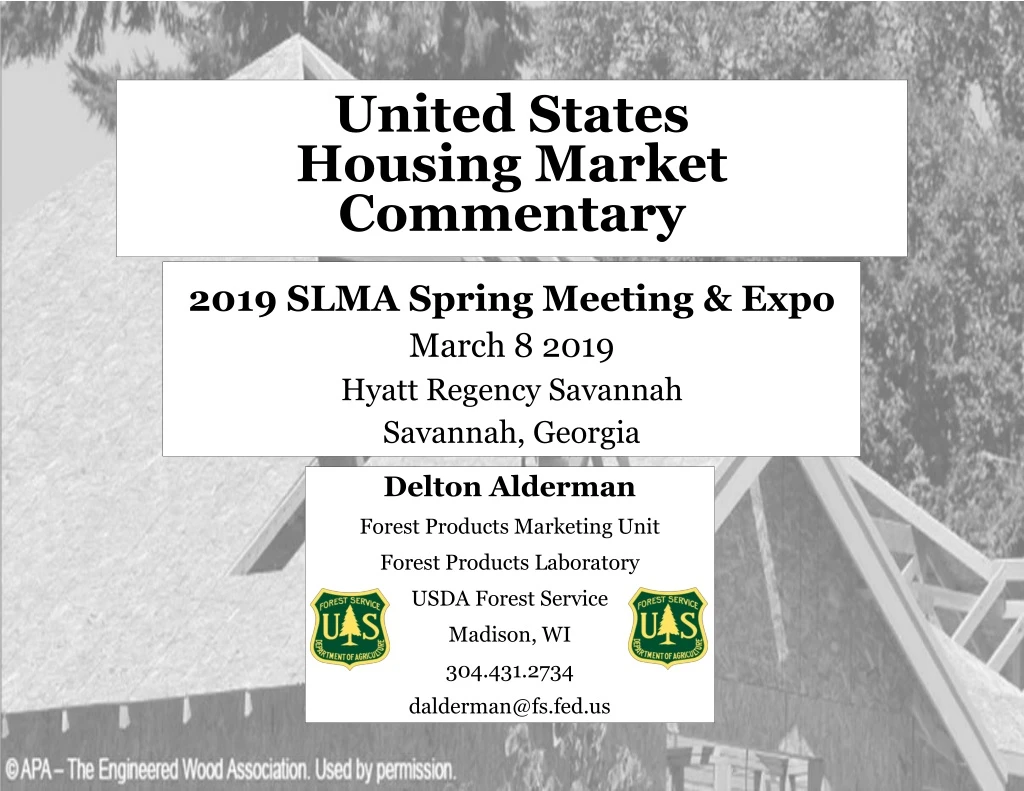

This commentary provides an analysis of the United States housing market, including an overview of housing demographics, the rise of modular/offsite housing, and an economic and financial outlook.

E N D

United States Housing Market Commentary 2019 SLMA Spring Meeting & Expo March 8 2019 Hyatt Regency Savannah Savannah, Georgia Delton Alderman Forest Products Marketing Unit Forest Products Laboratory USDA Forest Service Madison, WI 304.431.2734 dalderman@fs.fed.us

United States Housing United States Housing Demographics Modular/Offsite Housing Economics & Finance Outlook Conclusion

United States Housing: 1840-2018 Sources: Carliner (2010), U.S. Department of Commerce–Construction (2019), and Gottlieb (1964).

United States Housing: 1840-2018 U.S. population: 144 mil U.S. population: 326 mil Sources: Carliner (2010), U.S. Department of Commerce–Construction (2019), and Gottlieb (1964).

2019 Housing Forecasts* Total starts, range: 1,134 to 1,400 Median: 1,280 Single-family starts, range: 815 to 920 Median: 900 Multi-family starts, range: 319 to 480 New SF house sales, range: 618 to 688 Median: 638 * Thousands of units Sources: https://www.woodproducts.sbio.vt.edu/housing-report/ or http://pubs.ext.vt.edu/tags.resource.html/pubs_ext_vt_edu:wood-products

Home Ownership Source: https://www.census.gov/housing/hvs/index.html

Home Ownership Source: https://www.census.gov/housing/hvs/index.html

Home Ownership x Age Class Source: https://www.census.gov/housing/hvs/index.html

Pent-Up Demand? • Young Adults Living in Parents’ Basements • Causes and Consequences • “Share of young adults ages 25 to34 living with their parents increased from 11.9 percent in 2000 to 22.0 percent in 2017. • … more than 5.6 million additional young adults under their parents’ roofs between the two years. • This trend matches the decline in young adults’ marital rate (from 55.3 percent to 40.0 percent) during this period. • Increases in rents and student debt plays an important role in young adults’ decisions to stay with their parents. • Metropolitan statistical areas with higher unemployment rates experienced a greater increase in the share of young adults living under their parents’ roofs.” – Jung Choi, Jun Zhu, & Laurie Goodman; Urban Institute Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? • Young Adults Living in Parents’ Basements • Potential Consequences • “Young adults who stayed with their parents between ages 25 and 34 were less likely to form independent households and become homeowners 10-years later than those who made an earlier departure. • Even if they did ultimately buy a home, young adults who stayed with their parents longer did not buy more expensive homes or have lower mortgage debts than did young adults who moved out earlier, • suggesting that living with parents does not better position young adults for homeownership, a critical source of future wealth, • and may have negative long-term consequences for independent household formation.” – Jung Choi, Jun Zhu, & Laurie Goodman; Urban Institute Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? Source: https://www.urban.org/research/publication/young-adults-living-parents-basements/view/full_report/; 1/31/19

Pent-Up Demand? Source: https://blogs.wsj.com/dailyshot/2019/02/27/the-daily-shot-pent-up-demand-for-multifamily-housing/; 2/27/19

Pent-Up Demand & Student Debt Source: https://fred.stlouisfed.org/series/SLOAS/; 3/8/19

New SF Housing Starts Source: https://www.kansascityfed.org/publicat/econrev/pdf/13q4Rappaport.pdf; Q4 2013

New Housing Starts * All start data are presented at a seasonally adjusted annual rate (SAAR). ** US DOC does not report 2 to 4 multifamily starts directly, this is an estimation ((Total starts – (SF + 5 unit MF)). January 2019: Total: 1,230m SF: 926m MF: 304m Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

Total Housing Starts: Six-Month Average Total Starts SAAR; in thousands Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

SF Housing Starts: Six-Month Average SF Starts SAAR; in thousands Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

New SF Starts New SF starts adjusted for the US population From December 1959 to December 2007, the long-term ratio of new SF starts to the total US non-institutionalized population was 0.0066; in December 2018 it was 0.0029 – a decrease from November (0.0031). The long-term ratio of non-institutionalized population, aged 20 to 54 is 0.0103; in December 2018 was 0.0051 – also a decline from October (0.0055). From a population worldview, new SF construction is less than what is necessary for changes in population (i.e., under-building). Sources: http://www.census.gov/construction/nrc/pdf/newresconst.pdff and The Federal Reserve Bank of St. Louis; 2/26/19

New Housing Starts by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total starts. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

Total SF Housing Starts by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total starts. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

MF Housing Starts by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total starts. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

SF vs. MF Housing Starts (%) Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

New Housing Permits * All permit data are presented at a seasonally adjusted annual rate (SAAR). January 2019: Total: 1,345m SF: 812m MF: 533m Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

Total New Housing Permits SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total permits. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

Total Housing Permits by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total permits. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

SF Housing Permits by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total permits. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

MF Housing Permits by Region SAAR; in thousands NE = Northeast, MW = Midwest, S = South, W = West US DOC does not report 2 to 4 multi-family completions directly, this is an estimation (Total completions – SF completions). * Percentage of total permits. Source: http://www.census.gov/construction/nrc/pdf/newresconst.pdf; 2/26/19

Total New SF Sales • Source: https://www.census.gov/construction/nrs/index.html; 2/26/19

New SF Housing Sales: Six-month average & monthly SAAR; in thousands • Source: https://www.census.gov/construction/nrs/index.html; 2/26/19

New SF Sales by Region * Percentage of total permits. • Source: https://www.census.gov/construction/nrs/index.html; 2/26/19

New SF House Sales * Total new sales by price category and percent. • Source: https://www.census.gov/construction/nrs/index.html; 2/26/19

New SF House Sales New SF Sales: ≤ $ 200m and ≥ $500m: 2002 to December 2018 The number of ≤ $200 thousand plus SF houses has declined dramatically since 20021, 2. Subsequently, from 2012 onward, the ≥ $500 thousand class has soared (on a percentage basis) in contrast to the ≤ $200m class. One of the most oft mentioned reasons for this occurrence is builder net margins. Note: Sales values are not adjusted for inflation.

New SF House Sales • Source: https://www.census.gov/construction/nrs/index.html; 2/26/19

New SF House Sales by Square Feet of Floor Area in thousands of units; SAAR New SF Sales: ≤ 1,400 square feet and ≥ 4,000 square feet: 1999 to 2017 The number of SF houses sold (≥ 4,000 sq ft) has risen dramatically since 2010.. Some of the most oft mentioned reasons for this is builder net margins; regulations, and finance availability. Source: https://www.census.gov/construction/chars/pdf/soldsquarefeet.pdf; 11/28/18

December 2018 Construction Spending * billion. ** The US DOC does not report improvement spending directly, this is a monthly estimation: ((Total Private Spending – (SF spending + MF spending)). All data are SAARs and reported in nominal US$. Source: http://www.census.gov/construction/c30/pdf/privsa.pdf; 3/1/19

Total Construction Spending (adjusted): 1993-2018* SAAR; in millions of US dollars (adj.) Reported in adjusted US$: 1993 – 2017 (adjusted for inflation, BEA Table 1.1.9); *December 2018 to December 2018 reported in nominal US$. Source: http://www.census.gov/construction/c30/pdf/privsa.pd; 3/1/19

Construction Spending Shares: 1993 to December 2018 percent Total Residential Spending: 1993 through 2006 SF spending average: 69.2% MF spending average:7.5% Residential remodeling (RR) spending average: 23.3% (SAAR). Note: 1993 to 2017 (adjusted for inflation, BEA Table 1.1.9); Jan-December 2018 reported in nominal US$. Source: http://www.census.gov/construction/c30/pdf/privsa.pdf and http://www.bea.gov/iTable/iTable.cfm; 3/1/19

Adjusted Construction Spending: Y/Y Percentage Change, 1993 to December 2018 Nominal Residential Construction Spending: Y/Y percentage change, 1993 to December 2018 Presented above is the percentage change of inflation adjusted Y/Y construction spending. SF declined; MF and Remodeling expenditures were positive, on a percentage basis, year-over-year. Source: http://www.census.gov/construction/c30/pdf/privsa.pdf; 3/1/19

United States Housing Stock x Age Class 12.7% 4.9% 10.3% 10.6% 15.1% 13.4% 13.8% 13.9% 2.8% 2.5% • Source: https://factfinder.census.gov; 3/5/19

Remodeling Source: http://www.metrostudy.com/go/webinar2019remodeling/; 2/13/19

Remodeling Source: https://www.remodeling.hw.net/benchmarks/economic-outlook-rri/remodeling-outlook-remains-positive-for-2019-rri-finds_o; 2/19/19

Remodeling Source: http://www.metrostudy.com/go/webinar2019remodeling/; 2/13/19

Existing House Sales National Association of Realtors January 2019 sales: 4.940 thousand * All sales data: SAAR Source: https://fred.stlouisfed.org/series/EXHOSLUSM495S; 2/21/19

Existing House Sales SAAR; in thousands Source: https://fred.stlouisfed.org/series/EXHOSLUSM495S; 2/21/19

Offsite Manufacture • Prefab, Panelized, and Modular • Offsite Construction • “All modular homes are prefab homes, but not all prefab homes are modular” – Revolution Precrafted Properties • Prefab: Offsite factory-built construction • Modular Construction: Structure is assembled in cartridge units, typically six-sided boxes that are prefinished and structurally self-contained • Panelized: Walls of structure are built in a factory, then shipped to the construction site, and assembled • Trivia: Who was the first company to produce modular homes? • Hint: Began in 1895 • Source: https://www.builderonline.com/design/projects/prepping-for-prefab_o?; 6/25/18

Offsite Manufacture • Offsite Construction • Permanent modular construction increased by 2.1% to 23,286 units in 2017, according to the latest estimates by the Modular Building Institute (MBI). • The modular construction market is projected to grow at a compound annual growth rate of 6.9% from $112.4 billion today [2018] to $157 billion by 2023. • Some reasons for Off-Site: • Improved quality control • Vastly reduces construction waste? “Greener” building practices? • Skilled & unskilled labor shortages • Predictable project schedule – faster cycle times • Alleviate the Affordable-Housing Gap? • Reduce aggregate costs – can economies of scale be achieved? • Improved construction safety

Economic Overview Residential investment -10.6% Permanent-site -21.9% Manufactured homes 3.7% Improvements 3.0% • Atlanta Fed GDPNow™ • Latest forecast: 0.5 percent — March 6, 2019 • “The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2019 is 0.5 percent on March 6, up from 0.3 percent on March 4. …” – Pat Higgins, Economist, Federal Reserve Bank of Atlanta Source: https://www.frbatlanta.org/cqer/research/gdpnow.aspx; 3/6/19