Download

1 / 38

380 likes | 836 Views

International Investment Position (IIP) Presentation for Data Producers and Users Workshop May 8-9, 2006 SBP LRC Karachi Naseer Ahmad Joint Director Statistics State Bank of Pakistan Ph: 021 921 2571 E-mail: naseer.ahmed@sbp.org.pk INTRODUCTION What is the IIP? Why is it important?

E N D

International Investment Position (IIP)Presentation forData Producers and Users WorkshopMay 8-9, 2006SBP LRC Karachi Naseer Ahmad Joint Director Statistics State Bank of Pakistan Ph: 021 921 2571 E-mail: naseer.ahmed@sbp.org.pk

INTRODUCTION • What is the IIP? • Why is it important? • Who should compile it? • Periodicity? • Data Sources? • How is it compiled? Compilation Methodologies? • Dissemination process & practices • Improvement plans? • Questions or suggestions?

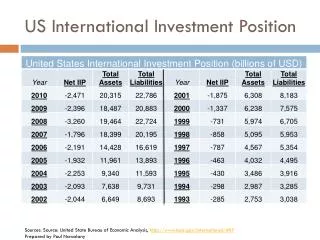

What is the IIP? • It is a balance sheet • It is snapshot of the stocks • At a specific point of time i.e. end of period • Only for external financial assetsand liabilities • First time introduced in Pakistan • IIP mirrors the financial account in the balance of payments

Why is it important? Scope • Assess economic relations with the rest of the world • Monitor developments in external relations between countries • Measure degree of financial openness • Monitor foreign external debt • Indicator of external debt sustainability • Indicator of financial stability • International investment treaties

Who Should Compile it? • IIP is an encouraged element for GDDS • IIP is a prescribed element for SDDS • Most commonly • the central bank • the central statistical office • a foreign exchange control body • a ministry (ministry of finance, economic affairs, or international relations) • More than one agency may collect and compile data • Crucial for these agencies to coordinate among themselves

Who Should Compile it? • Centralizing the tasks of balance of payments and IIP compilation in one agency • simplifies cross-checking of the external flow and position data • enhances overall consistency of the two datasets

Who Should Compile it? • If different agencies produce external debt and IIP • close cooperation required • data on the external debt position can be considered as a subset of the IIP • both sets of statistics need to be consistent • Coordinate the reporting requirements for respondents • avoid having respondents report the same data to different agencies

Periodicity and Timeliness • Started with compilation of data on IIP showing stock positions as on 31 December 2003 and 31 December 2004 on yearly periodicity • International Standards -Yearly periodicity is required; • Quarterly is encouraged • Recommended timeliness is one year

Data Sources Domestic Statistical Sources: • Banks' External Assets and Liabilities • Monetary Authorities’ External Assets and Liabilities • General Government External Debt • Surveys • Balance of Payments Statement Domestic Non-statistical Sources • Financial Statements • Foreign Investment Approval • Financial Press

Assets Direct investment Portfolio investment Financial derivatives Other investment Reserve assets Liabilities Direct investment Portfolio investment Financial derivatives Other investment How is it compiled? International Investment Position As On_____ IIP (Net) = Asset - Liabilities

How is it compiled? • Opening Position • Transactions • Price changes • Exchange rate changes • Other adjustments (reclassifications, debt write-offs, etc.) = Closing Position

Residence and Time of recording Residence • Only those assets and liabilities of residents that represent claims on or liabilities to non-residents are recorded Time of recording • A country’s external financial condition as of a specific point in time (such as year-end). • Time of recording of financial items that constitute position governed by the principle of accrual accounting

Valuation In principle, all asset and liability positions should be measured at market value Assumes that such positions are continuously and regularly revalued

Functional Types of Investment • Financial instruments grouped according to the intent of the resident holders or issuers • Direct investment • Portfolio investment • Financial derivatives • Other investment • Reserve assets

Financial Assets and Liabilities • Most financial assets are financial claims • Represented by financial instruments • currency and deposits • loans • advances and other credits • securities - bills and bonds • Financial assets that are not financial claims • monetary gold • SDRs allocated by the IMF • shares in corporations • financial derivatives

Direct Investment • Objective - Resident in one economy (direct investor) obtaining a lasting interest in an enterprise resident in another economy (direct investment enterprise) • Implies long-term relationship between the direct investor and the direct investment enterprise • Implies significant degree of influence by the direct investor in the management of the enterprise.

Direct Investment • Sole criterion is ownership of 10 percent or more of the ordinary shares • Classified by direction of investment • Direct investment in reporting economy • Direct investment abroad • Includes the initial transaction establishing the FDI relationship and all subsequent capital transactions among affiliated enterprises

Direct Investment • Covers all financial claims and liabilities between direct investors and direct investment enterprises except: • Financial derivatives • Loan or debt guarantees provided by a direct investor or related direct investment enterprise • Transactions between affiliated financial intermediaries other than transactions in equity or permanent debt • Changes in insurance company technical reserves

Direct Investment Components • Current Account • Direct Investment income • Income on equity • Dividends and distributed branch profits • Reinvested earnings and undistributed branch profits • Income on debt (interest) • Financial Account • Equity capital • Reinvested earnings (counter entry to income item) • Other capital

Direct Investment Equity Capital • Equity in branches • Shares in subsidiaries and associates • Non-cash acquisitions of equity (for example, provision of capital equipment)

Direct Investment Reinvested Earnings and Distributed Branch Profits • The direct investor’s share • in proportion to equity held • of earnings that foreign subsidiaries and associated enterprises do not distribute as dividends and • earnings that branches and other unincorporated enterprises do not remit to direct investors

Direct Investment Other Capital Intercompany borrowing or lending of funds, include: • Loans • Debt securities • Suppliers’ (trade) credits • Financial leases* • Non-participating preferred shares *Financial Lease A contract in which the service provided by the lessor to the lessee is limited to financing equipment. All other responsibilities related to the possession of equipment, such as maintenance, insurance, and taxes, are borne by the lessee. A financial lease is usually noncancellable and must be fully paid out over its term.

Portfolio Investment • Financial instruments in the form of equity and debt securities • Usually traded (or tradable) in organized markets • Equity securities • Debt securities • Bonds and notes (long-term) • Money-market instruments (short-term)

Portfolio Investment • Further classified by institutional sector of resident holder for assets/resident issuer for liabilities: • monetary authorities • general government • banks • other sectors

Financial Derivatives* What is a financial derivative? Financial instrument linked to an underlying item such as: • Another financial instrument (currency) • An indicator (price index) • A commodity (silver) Through which financial risks such as: • Interest rate risk • Foreign exchange risk • Equity price risk • Commodity price risk or • Credit risk Can, in their own right, be traded in financial markets * To be covered in Session 3

Other Investment • Residual category • All financial instruments other than those classified as direct investment, portfolio investment, financial derivatives, or reserve assets • Primarily classified by instrument and secondarily by sectors • Recommend classification by original maturity (short and long term)

Other Investment Instruments include: • Trade credits • Loans • Currency and deposits • Other assets and liabilities • Miscellaneous accounts receivable and payable • Interest payments in arrears, loan payments in arrears, taxes outstanding, prepayments of insurance premiums • Capital subscriptions to nonmonetary international organizations • Household equity in life insurance and commercial pension funds

Reserve Assets External assets that are: • foreign currency claims on a nonresident • readily available to and under the effective control ofthe monetary authorities • to meet a balance of payments need

Reserve Assets Classification distinguishes • Monetary gold • SDRs • Reserve position in the IMF • Foreign exchange • Other claims

IIP- BOP • Closely inter-related • Changes that have occurred during the period • Current account – investment income • Payments and receipts on investment measured in the IIP • Financial account • Financial transactions that contributed to the change in positions

IIP- BOP Reconciliation Statement Opening Position • Transactions in Financial Account • Price changes • Exchange rate changes • Other adjustments (debt write-offs, reclassifications) = Closing Position

Factors Accounting for Change in the International Investment Position

Dissemination process & practices • Data are disseminated on SBP’s website • Published in SBP annual report

Improvement plans? • Improvements in enterprises data collection • Enhance frequency • Movement wise dissemination • Country wise compilation • Security wise compilation • Currency wise compilation

Tanks all of you