Download

1 / 45

560 likes | 771 Views

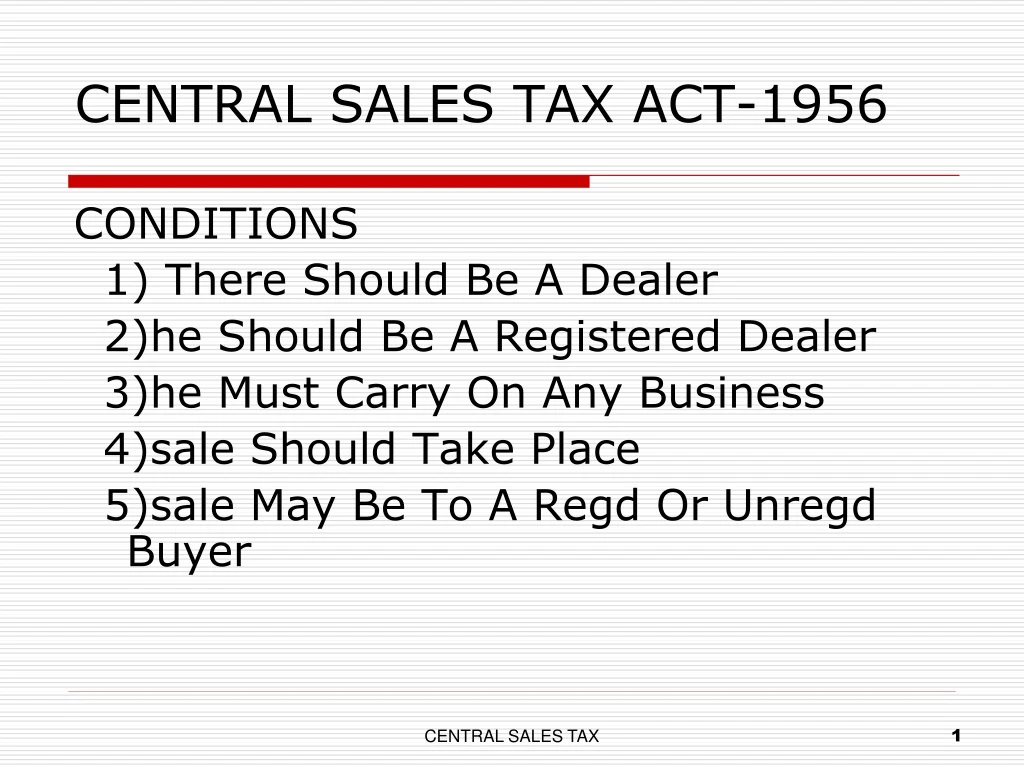

CENTRAL SALES TAX ACT-1956. CONDITIONS 1) There Should Be A Dealer 2)he Should Be A Registered Dealer 3)he Must Carry On Any Business 4)sale Should Take Place 5)sale May Be To A Regd Or Unregd Buyer. The Sale Should Be Of Goods.

E N D

CENTRAL SALES TAX ACT-1956 CONDITIONS 1) There Should Be A Dealer 2)he Should Be A Registered Dealer 3)he Must Carry On Any Business 4)sale Should Take Place 5)sale May Be To A Regd Or Unregd Buyer CENTRAL SALES TAX

The Sale Should Be Of Goods. • The Sale Can Be Of Also Declared Goods (Goods Of Specific Importance) • The Sale Should Take Place In Course Of Inter State • The Sales Should Not Be Within The Same State. • The Sale Should Not Be Outside India CENTRAL SALES TAX

DEFINITIONS DEALER U/S 2(b). He Is A Person One Who Is Involved In The Activities Of Buying ,Selling ,Distributing The Goods Directly Or Indirectly Either For Cash Or For Deferred Payment ,For Commission ,Brokerage Etc CENTRAL SALES TAX

continued Dealer Includes 1)local Authorities ,Co-operative Societies, A Company,HUF, Association Of Persons,firms.. 2)suppliers, Broker, Del Creder Commissioner,etc 3) An Auctioneer (govt ,Agent,etc) CENTRAL SALES TAX

REGISTERED DEALER SEC 7 A PERSON SHOULD REGISTER HIMSELF U/S 7 THE REGISTRATION MAY BE 1)VOLUNTARY REGISTRATION OR 2)COMPULSORY REGISTRATION, CENTRAL SALES TAX

Compulsory Registration • As per section 7(1), every dealer liable to pay Central Sales Tax has to register himself with sales tax authority. • As per section 6(1) of CST Act, every dealer effecting sale in the course of Inter State trade or commerce is liable to pay CST. • Thus, only those dealers who ‘effect’ inter state sales are required to register under CST Act. • Thus, registration under CST Act is done by State Sales Tax authorities who are authorised for the purpose

Voluntary Registration • A dealer registered with State sales tax authorities may voluntarily apply for registration under CST Act even if he is not liable to pay Central Sales Tax [section 7(2) of CST Act]. • He is entitled to apply for registration even if goods sold or purchased by him are exempt under State sales tax law. • This application for registration can be made any time. This provision is mainly useful when the dealer makes purchases in Inter State but all his sales are within the State. • Thus, he is not liable for payment of any CST. However, he can make purchases in Inter State at concessional rate only if he is registered. Hence, he can register even if he is not liable to pay any CST.

Application for registration • Application for registration should be made in prescribed form ‘A’ within 30 days from the date when dealer becomes liable to CST. • Application fee of Rs. 25 • Application has to be signed by • (a) proprietor of business • (b) one of the partners in case of firm • (c) Karta or Manager of HUF • (d) director or principal officer of Company • (e) principal officer in case of association of individuals or

Other documents required at time of registration • Normally, following are asked for – • (a) Particulars of Directors/ partners • (b) Copies of articles of association, memorandum in case of company and partnership deed if applicant is a firm • (c) Copies of rent agreements • (d) Nominations as Manager • (e) List of places of business, godown • (f) Details of machinery • (g) Details of bankers • (h) Photographs of directors / partners.

Certificate of Registration under CST • The registering authority will ensure that application is in conformity with provisions of CST Act. He can make necessary enquiries e.g. • (a) particulars given are correct • (b) Materials requested for registration are eligible for inclusion and the goods are in fact needed for the business. • After he is satisfied and after obtaining required security, the dealer will be issued a Certificate of Registration in prescribed form ‘B’. • A copy of the same will be issued for every additional place of business in the State. This certificate should be kept at principal place of business and a copy of the certificate should be kept at each additional place of business in the State.

BUSINESS 2(aa) BIZ INCLUDES 1)TRADE,COMMERCE ,MFG AND ADVENTURE IN NATURE OF TRADE COMMERCE AND MFG ANY INCIDENTAL AND ANCILLIARY ACTIVITIES RELATED TO MAIN BUSINESS SHOULD ALSO BE CONSIDERED AS BUSINESS CENTRAL SALES TAX

POINTS TO BE REMEMBERED THE PROFIT MOTIVE IS NOT COMPULSORY FOR THE SALES TAX PURPOSE THE TAX IS LEVIED ON SALES NOT ON PROFIT CENTRAL SALES TAX

SALE -2(G) SALE INCLUDES A TRANSFER OF GOODS FOR MONEY TRANSFER OF GOODS FOR MONEY’S WORTH TRANSFER OF GOODS ON AN AGREEMENT TO PAY ON DEFERRED SYSTEM HIRE PURCHASE SYSTEM AND INSTALLMENT SYSTEM . CENTRAL SALES TAX

SALE MAY BE TO A REGISTERED BUYER OR UNREGISTERED BUYER. ELEMENT OF PRICE IS ESSENTIAL. FREE SUPPLY IS NOT SALE. QUANTITY DISCOUNT IS NOT A SALE. MORTGAGE IS NOT A SALE. DEPOT TRANSFER IS NOT A SALE. POINTS TO BE REMEMBERED CENTRAL SALES TAX

GOODS-2(d) GOODS MEANS ANY ARTICLE ,THING, COMMODITY,AND WHICH IS MOVABLE ,HOWEVER GOODS DOES NOT INCLUDE NEWSPAPERS,ACTIONABLE CLAIMS,STOCKS, SHARES, SECURITIES. CENTRAL SALES TAX

POINTS TO BE REMEMBERED NEWS PAPERS WHEN NEWS PAPERS ARE SOLD AS NEWSPAPERS EITHER NEW OR OLD, IS TO BE TREATED AS NOT A GOODS. WHEN OLD PAPERS ARE SOLD AS OLD NEWSPAPERS THEN TO BE TREATED AS GOODS. CENTRAL SALES TAX

FEW EXAMPLES OF SALE SALE OF STEAM, packaged SOFT WARE, ELECTRICAL ENERGY ANIMALS AND BIRDS, UPROOTED TREES, SECOND HAND GOODS, REGECTED GOODS, SIM CARD, TRADE MARK, LOTTERY TICKETS. CENTRAL SALES TAX

DECLARED GOODS –SEC2(C) Declared Goods Includes Cereals ,Pulses, Coal Including Coke But Not Charcoal, Cotton Waste , Hand Made Garments,tobacco, Raw Tobacco, Cheroots Of Tobacco ,Jute, Oil Seeds, Cotton In Unmanufactured Form ,Crude Oil,sugar,khandsare Sugar, Aviation Turbine Fuel,refused Tobacco, Cigars ,Hides And Skins, Woven Fabrics Of Wool. CENTRAL SALES TAX

POINTS TO BE REMEMBERED DECLARED GOODS ARE GOODS OF SPECIAL IMPORTANCE.IF DECLARED GOODS ARE SOLD THERE ARE CERTAIN BENEFITS WHICH CAN BE OBTAINED BY THE DEALER ,WHICH IS NOT AVAILABLE FOR THE ORDINARY GOODS. CENTRAL SALES TAX

TAX ON INTER STATE SALE OF GOODS - • Sale is Inter-State when • (a) sale occasions movement of goods from one State to another • or • (b) is effected by transfer of documents during their movement from one State to another.

INTER STATE SALE-SEC 3 ONCE THE GOODS ARE TAKEN OUT OF DEALERS PLACE THEN FINAL DESTINATION SHOULD BE TAKEN INTO CONSIDERATION AND NOT THE ROUTE THROUGH WHICH GOODS ARE TRANSFERRED. CENTRAL SALES TAX

Temporary movement through another State is not Inter State sale - • Explanation 2 to section 3 states that if movement of goods starts from one State and ends in the same State, it will not be deemed to be movement of goods during ‘inter State sale’; even if during transit goods pass through other State.

What is ‘Sale outside a State’ • - CST Act defines 'sale outside a State • This definition is important as 'sale outside a State' cannot be taxed by State Government. • Section 4(1) defines ‘Sale Outside a State’ in a round about way. • The section states that ‘subject to provisions of section 3, when a sale or purchase is inside a State as per section 4(2), such sale or purchase will be outside all other States’.

Sale inside a State • Section 4(2) states that a sale or purchase of goods shall be deemed to take place inside a State if the goods are within the State • (a) in the case of specific or ascertained goods, at the time the contract of sale is made and • (b) in the case of un-ascertained or future goods, at the time of their appropriation to the contract of sale by the seller or by the buyer, whether assent of the other party is prior or subsequent to such appropriation. • Explanation to this section states that where there is a single contract of sale or purchase of goods situated at more than one place, provisions of section 4(2) shall apply as if there were separate contracts at each of such places.

EXAMPLES IN CASE OF DEPOT SALE HEAD OFFICE------------KARNATAKA DEPOT OFFICE ----------DELHI IF ORDER IS TAKEN FROM CUSTOMER IN DELHI AND GOODS ARE TRANSFERRED TO DELHI FIRST AND THEN SALE IS MADE-INTER STATE SALE CENTRAL SALES TAX

CONTD. IF FIRST GOODS ARE TRANSFERRED TO DELHI DEPOT AND THEN SALE IS MADE – IT IS SALE WITHIN DELHI AND HENCE INTRA STATE SALE.THEN NO CST IS APPLICABLE . BUT FORM F SHOULD BE GIVEN . CENTRAL SALES TAX

INSPECTION CUSTOMER FROM DELHI COMES TO KARNATAKA AND INSPECTS THE GOODS ,THIS IS INTER STATE SALE,. IF PURCHASE IS ALSO MADE ALONG WITH INSPECTION THEN IT IS INTRA STATE SALE. CENTRAL SALES TAX

SUBSEQUENT SALE WHEN THE GOODS ARE IN TRANSIT THEN IF BUYER RE DIRECTS THE GOODS TO SOME OTHER CUSTOMER OF OTHER STATE , IT IS CALLED AS SUBSEQUENT SALE AND SHOULD BE TREATED AS INTER STATE SALE. CENTRAL SALES TAX

What is ‘Sale in course of Export’ Section • A sale or purchase of goods is deemed to be in course of export of the goods out of the territory of India, only if • (a) the sale or purchase either occasions such export or • (b) is effected by a transfer of documents of title to goods after the goods have crossed the customs frontiers of India.

Section 5(3) states that notwithstanding provisions of section 5(1), last sale or purchase of goods preceding the sale or purchase occasioning the export of those goods out of territory of India shall also be deemed to be in the course of such export, if such last sale or purchase took place after, and was for the purpose of complying with, the arrangement or order for or in relation to such export. • Sale should occasion the export - Occasion means ‘to be immediate cause of’. Sale and Export should constitute part of an integrated activity. Unless such sale occasions export, it is not a sale in course of export.

Sale or purchase in the course of import. • A sale or purchase of goods is deemed to be in course of import of the goods into the territory of India, only if (a) the sale or purchase either occasions such import or (b) is effected by a transfer of documents of title to goods before the goods have crossed the customs frontiers of India [section 5(2) of CST Act].

BASIS OF CHARGE WHEN ALL THESE CONDITIONS ARE SATISFIED THEN CST WILL BE LEVIED AT SPECIFIED RATE ON TAXABLETURNOVER WHICH WILL BE BASED ON SALES AND NOT ON PROFITS. CENTRAL SALES TAX

SPECIFIED RATES FOR THE PURPOSE OF SPECIFIED RATES BUYERS ARE CLASSIFIED INTO THREE GOVERNMENT BUYER(FORM D) REGISTERED BUYER(FORM C) UN REGISTERED BUYER(NO FORMS) CENTRAL SALES TAX

For Registered Buyers LOCAL SALES TAX RATE OR 2% WHICH EVER IS LESS IF LST IS NIL –CST WILL BE NIL IF LST IS < 2%-THEN CST WILL BE SAME IF LST IS >= THAN 2%-THEN CST WILL BE 2%. CENTRAL SALES TAX

FOR UNREGISTERED BUYER Same as LST CENTRAL SALES TAX

TURN OVER.-2( j ) TURNOVER IS AGGREGATE OF THE SALE PRICES RECIEIVED AND RECEIVABLE BY THE DEALER IN RESPECT OF SALES OF ANY GOODS IN THE COURSE OF INTER STATE TRADE,MADE DURING THE PRESCRIBED PERIOD.(USUALLY QUARTERLY),LESS CST. CENTRAL SALES TAX

FORMULA TURNOVER = 100*SALEPRICE . 100 +RATE. TAX PAYABLE= SALEPRICE *RATE . 100 +RATE. CENTRAL SALES TAX

SALE PRICE –SEC 2( h ) Sale Price Means The Amount Payable To A Dealer As Consideration For The Goods, Less Any Sum Allowed As Cash Discount According To The Practice Prevailing In The Trade,but Inclusive Of Any Sum Charged For Anything Done By The Dealer In Respect Of The Goods At The Time Of Or Before The Delivery Thereof, Other Than Cost Of Freight, Or Delivery Or The Cost Of Installation In Cases Where Such Cost Is Separately Charged. CENTRAL SALES TAX

SALE PRICE SEC-2 ( h ) INCLUDES CONSIDERATION FOR SALE EXCISE DUTY SALES TAX PAYABLE BY THE DEALER SUM CHARGE FOR ANYTHING DONE BY THE DEALER IN RESPECT OF GOODS AT THE TIME OF DELIVERY OR BEFORE THE DELIVERY. FREIGHT (IF INCLUDED IN SALE PRICE) INSURNCE (IF INCLUDED IN SALE PRICE) CENTRAL SALES TAX

CONTD COST OF INSTALLATION (IF INCLUDED IN SALE PRICE) COST OF PACKING MATERIALS AND PACKING CHARGES. BONUS OR INCENTIVE FOR ATTAINING SALES TARGET. DESIGN FEES CHARGED INRESPECT OF GOODS MFGD AS PER THE DESIGN GIVEN BY THE BUYER. CENTRAL SALES TAX

WHAT IS NOT INCLUDED IN SALE PRICE CASH DISCOUNT OR TRADE DISCOUNT OR QUANITITY DISCOUNT, COST OF FREIGHT(IF CHARGED SEPERATELY) COST OF INSURANCE(IF CHARGED SEPERATELY) DEPOSITS FOR RETURNABLE CONTAINER. CENTRAL SALES TAX

CONTD COST OF INSTALLATION (IF CHARGED SEPERATELY) TAX AND FEES STATUTORILY RECOVERABLE FROM BUYER.(OTHER TAXES) SUBSIDY PAID BY GOVERNMENT NOT PART OF TURNOVER SALE PRICE OF THE GOODS RETURNED BY THE BUYER WITHIN 6 MONTHS SALE PRICE OF GOODS REJECTED BY THE BUYER. CENTRAL SALES TAX

FORMS TO BE ISSUED FORM C - REGISTERED BUYER FORM E1/ E2 SUBSEQUENT SALE FORM F - STOCK TRANSFER(DEPOT) FORM H - SALE TO EXPORTER FORM I - SALE TO SEZ Form J Certificate to be issued by foreign diplomatic mission or consulate in India or the UN Agency CENTRAL SALES TAX

SUBSEQUENT SALE IF SUBSEQUENT SALE IS MADE TO REGISTERED AND GOVERNMENT DEALER IT IS EXEMPTED However relevant forms to be obtained (E1&E2) IF SUBSEQUENT SALE IS MADE TO UNREGISTERED DEALER THEN IT IS TAXABLE CENTRAL SALES TAX