Download

1 / 17

170 likes | 303 Views

Logic – the study of arguments. "the tool for distinguishing between the true and the false ;“ "the Science, as well as the Art, of reasoning” inductive reasoning : drawing general conclusions from specific examples/ analysis : from object to its components

E N D

Logic– the study of arguments • "the tool for distinguishing between the true and the false;“ • "the Science, as well as the Art, of reasoning” • inductive reasoning: drawing general conclusions from specific examples/ analysis : from object to its components • deductive reasoning: drawing logical conclusions from definitions and axioms/ synthesis: how parts can be combined to form a whole.

Chapter 25 Options and corporate securities

Chapter Outline • Options: The Basics • Option Payoffs • Employee Stock Options • Equity as a Call Option on the Firm’s Assets • Warrants • Convertible Bonds • Reasons For Issuing Warrants and Convertibles • Other Options

Options: The Basics Option – a contract that gives its owner the right to buy or sell some asset at a fixed price on or before a given date • Put option – the right to sell some asset • Call option – the right to buy some asset • American vs. European options

Option Payoffs – Calls • The value of the call at expiration is the intrinsic value • C1 = Max(0, S1 - E) • If S1<E, then the payoff is 0 • If S1>E, then the payoff is S1 – E • Assume that the exercise price is $35

Option Payoffs - Puts • The value of a put at expiration is the intrinsic value • P1 = Max (0, E – S1) • If S1<E, then the payoff is E-S1 • If S1>E, then the payoff is 0 • Assume that the exercise price is $35

Employee Stock Options • Options that are given to employees as part of their benefits package • Often used as a bonus or incentive • Designed to align employee interests with stockholder interests and reduce agency problems • Empirical evidence suggests that they don’t work as well as anticipated due to the lack of diversification introduced into the employees’ portfolios • The stock just isn’t worth as much to the employee as it is to an outside investor

Equity: a Call Option • Equity can be viewed as a call option on the company’s assets when the firm is leveraged • The exercise price is the value of the debt • If the assets are worth more than the debt when it comes due, the option will be exercised and the stockholders retain ownership • If the assets are worth less than the debt, the stockholders will let the option expire and the assets will belong to the bondholders

Warrants • A security that gives the holder the right to purchase shares of stock at a fixed price over a given period of time • It is a call option issued by corporations in conjunction with other securities to reduce the yield • Usually included with a new debt or preferred shares issue as a sweetener or equity kicker

Differences between warrants and traditional call options • Warrants are generally very long term • They are written by the company and exercise results in additional shares outstanding • The exercise price is paid to the company and generates cash for the firm • Warrants can be detached from the original securities and sold separately

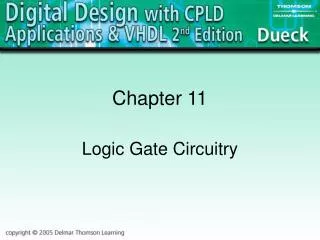

Convertibles • Convertible bonds (or preferred stock) may be converted into a specified number of common shares at the option of the security holder • The conversion price is the effective price paid for the stock • The conversion ratio is the number of shares received when the bond is converted • Convertible bonds will be worth at least as much as the straight bond value or the conversion value, whichever is greater

Minimum value of a convertible bond versus the value of the stock for a given interest rate

Valuing Convertibles • Suppose you have a 10% bond that pays semi-annual coupons and will mature in 15 years. The face value is $1,000 and the yield to maturity on similar bonds is 9%. The bond is also convertible with a conversion price of $100. The stock is currently selling for $110. What is the minimum price of the bond? • Straight bond value • Conversion ratio • Conversion value • Minimum price

Reasons for Issuing Warrants and Convertibles • They allow companies to issue cheap bonds by attaching sweeteners to the new bond issue. Coupon rates can then be set at below market rate for straight bonds • They give companies the chance to issue common stock in the future at a premium over current prices

Other Options • Call provision on a bond • Allows the company to repurchase the bond prior to maturity at a specified price that is generally higher than the face value • Increases the required yield on the bond – this is effectively how the company pays for the option • Put bond • Gives the bondholder the right to require the company to repurchase the bond prior to maturity at a fixed price

Other Options continued • Over allotment option • Underwriters have the right to purchase additional shares from a firm in an IPO • Insurance and Loan Guarantees • These are essentially put options • Managerial options