Chapter Five

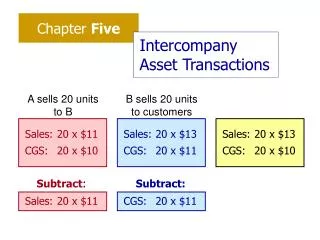

Chapter Five. Intercompany Asset Transactions. A sells 20 units to B. B sells 20 units to customers. Sales: 20 x $11 CGS: 20 x $10. Sales: 20 x $13 CGS: 20 x $11. Sales: 20 x $13 CGS: 20 x $10. Subtract :. Subtract:. Sales: 20 x $11. CGS: 20 x $11. A sells 20 units to B.

Chapter Five

E N D

Presentation Transcript

Chapter Five Intercompany Asset Transactions A sells 20 units to B B sells 20 units to customers Sales: 20 x $11 CGS: 20 x $10 Sales: 20 x $13 CGS: 20 x $11 Sales: 20 x $13 CGS: 20 x $10 Subtract: Subtract: Sales: 20 x $11 CGS: 20 x $11

A sells 20 units to B B sells 15 units to customers Sales: 20 x $11 CGS: 20 x $10 Sales: 15 x $13 CGS: 15 x $11 Invnt: 5 x $11 Sales: 15 x $13 CGS: 15 x $10 Invnt: 5 x $10 Subtract: Subtract: Sales: 20 x $11 CGS: 5 x $11 CGS: 15 x $11 Add: Subtract: CGS: 5 x $1 Invnt: 5 x $1

Prob 5-32 Excess Annual Cost Amortization Equipment $ 70,000 10 yrs $ 7,000 Buildings 40,000 20 yrs 2,000 Database 60,000 30 yrs 2,000 Total $170,000 $11,000 60% How Tall calculates equity earnings of Short: Reported income - Short $ 40,000 Recog prior yr unreal gain 5,000 Defer current yr unreal gain (10,000) Total $ 35,000 Parent’s share (60%) $21,000 Extra amortiz (11,000) Equity earnings of Short $10,000

Entry (*G) R/E, 1/1/04 5,000 CGS 5,000 To recognize unrealized gain in beginning inventory. Entry (S) R/E, 1/1/04 (adj) 345,000 Common Stock 90,000 Add Pd-in cap 60,000 Invst in Short 297,000 NC int sub 1/1/04 198,000

Entry (A) Equipment 56,000 Buildings 36,000 Database 56,000 Invst in Short 148,000 Equipment 70,000 – 2 x 7,000 Buildings 40,000 – 2 x 2,000 Database 60,000 – 2 x 2,000 60%

Entry (I) Equity earn of Short 10,000 Invst in Short 10,000 Entry (D) Invst in Short 15,000 Dividends Paid 15,000

Entry (E) Oper Exp (deprec) 9,000 Amortiz Expense 2,000 Equipment 7,000 Buildings 2,000 Database 2,000 Entry (P) Liabilities 30,000 Receivables 30,000

Entry (TI) Revenues 140,000 CGS 140,000 To eliminate intercompany inventory transfers (as if all of it had been sold). Entry (G) CGS 10,000 Inventory 10,000 To eliminate unrealized gain in ending inventory.

Noncontrolling Interest Entry NCint in Short Income 14,000 NC int Short 1/1/04 198,000 Dividends Paid 10,000 NC int in Short 12/31 202,000 40% x $35,000 Reported income - Short $ 40,000 Recog – prior yr unreal gain 5,000 Defer current yr unreal gain (10,000) Total $ 35,000

Upstream Sale Downstream Sale • Entry *G adjusts sub’s beginning R/E. • Entry S reflects this adjustment. • Entries G & *G adjusts sub’s current income. • Entries *C, I, and NCI reflect this adjustment. • Entry *G adjusts parent’s beginning R/E. • Entry S is unaffected. • Entries G & *G adjusts parent’s current income. • Entries *C, I, and NCI are unaffected.

Downstream 5,000 5,000 Entry (*G) Upstream R/E, 1/1/04 5,000 CGS 5,000 Beg R/E of subsidiary. Beg R/E of parent. NOTE: For purposes of this class, assume *G is always this entry.

Downstream 350,000 90,000 60,000 300,000 200,000 Entry (S) Upsteam R/E, 1/1/04 345,000 Common Stock 90,000 Add Pd-in cap 60,000 Invst in Short 297,000 NC int sub 1/1/04 198,000 When sale is upstream, beg R/E of sub reflects adjustment.

Downstream 13,000 13,000 Entry (I) Upstream Equity earn of Short 10,000 Invst in Short 10,000 Reported income - Short $ 40,000 Recog prior yr unreal gain 5,000 Defer current yr unreal gain (10,000) Total $ 35,000 Parent’s share (60%) $21,000 Extra amortiz (11,000) Equity earnings of Short $10,000 $ 40,000 . $ 40,000 $24,000 (11,000) $13,000 NOTE: There are different approaches to recording unrealized gains on downstream sales. Regardless of approach, consolidated totals will be the same.

Downstream 16,000 200,000 10,000 206,000 Noncontrolling Interest Entry Upstream NCint in Short inc. 14,000 NCint Short 1/1/04 198,000 Dividends Paid 10,000 NCint Short 12/31 202,000 40% x $35,000 40% x $40,000 Reported income - Short $ 40,000 Recog – prior yr unreal gain 5,000 Defer current yr unreal gain (10,000) Total $ 35,000

Intercompany Transfer of Depreciable Assets Prob 5-25 Sale of Building Individual Consolid Worksheet Records Perspect Adjustments Asset Transfer Equipment $ 50,000 $70,000 $ 20,000 Accum Deprec0 (40,000) (40,000) Gain on Sale(20,000) 0 20,000 Entry (TA) Equipment 20,000 Gain on Sale - Equip 20,000 Accum Deprec 40,000 Affects sub income on upstream sale.

Individual Consolid Worksheet Records Perspect Adjustments During 2003 Accum Deprec(10,000) (6,000) 4,000 Deprec Exp 10,000 6,000 (4,000) Entry (ED) Accum Deprec 4,000 Deprec Exp. 4,000 Affects sub income on downstream sale.

Individual Consolid Worksheet Records Perspect Adjustments Start of 2004 Equipment $ 50,000 $70,000 $ 20,000 Accum Deprec(10,000) (46,000) (36,000) R/E effect - seller(20,000) 0 20,000 R/E effect - buyer10,000 6,000 (4,000) Entry (*TA) Equipment 20,000 R/E, 1/1 (seller) 20,000 R/E, 1/1 (buyer) 4,000 Accum Deprec 36,000 One of these will affect Entry (S).

Individual Consolid Worksheet Records Perspect Adjustments Start of 2004 Equipment $ 50,000 $70,000 $ 20,000 Accum Deprec(10,000) (46,000) (36,000) R/E effect - seller(20,000) 0 20,000 R/E effect - buyer10,000 6,000 (4,000) Start of 2005 Equipment $ 50,000 $70,000 $ 20,000 Accum Deprec(20,000) (52,000) (32,000) R/E effect - seller(20,000) 0 20,000 R/E effect - buyer20,000 12,000 (8,000)

Individual Consolid Worksheet Records Perspect Adjustments During 2004 Accum Deprec(10,000) (6,000) 4,000 Deprec Exp 10,000 6,000 (4,000) Entry (ED) Accum Deprec 4,000 Deprec Exp. 4,000