Download

1 / 25

250 likes | 574 Views

Withdrawals from IRAs: When owner is between 59 ½ & 70 ½ ; & When owner turns 70 ½ MontGuide 200309 Marsha A. Goetting, MSU Kristen G. Juras, School of Law, University of Montana. Revised 2003. Marsha A. Goetting MSU Extension Family Economics Specialist. P. O. Box 172800

E N D

Withdrawals from IRAs: When owner is between 59 ½ & 70 ½; & When owner turns 70 ½MontGuide 200309Marsha A. Goetting, MSUKristen G. Juras, School of Law, University of Montana Revised 2003

Marsha A. GoettingMSU Extension Family Economics Specialist P. O. Box 172800 Montana State University Bozeman, MT 59717 406-994-5695

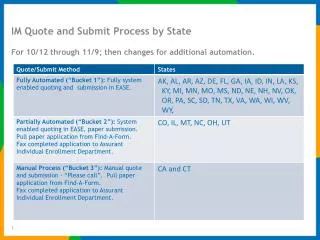

6 MontGuides • Individual Retirement Accounts • Shopping for an IRA • Withdrawals from IRAs • When owner is under 59 ½ • When owner is between 59 ½ & 70 ½; turns 70 ½ • Inheriting an IRA: Planning techniques • Primary beneficiaries • Successor beneficiaries

Individual Retirement Accounts www.montana.edu Search: Individual Retirement Accounts

IRA Tax Law Changes • Economic Growth & Tax Relief Reconciliation Act of 2001

Withdrawals • Between age 59 ½ & 70 ½ • No penalty • Subject to state & federal income tax

IRA Withdrawal • Bruce’s income $29,000 • Withdraws +$15,000 • Taxable income = $44,000 • Withdrawal “Lost” to taxes = $3,450

70 ½ Withdrawals • Age 70 ½ • Required Minimum Distributions (RMD)

Required Beginning Date • April 1 • Following year in which IRA owner reaches 70 ½

Born June 30, 1933 • Reaches 70 ½ • December 30, 2003 • RMD for 2003 • By April 1, 2004 • RMD for 2004 • By December 31, 2004

RMD Based upon • Owner’s age • Beneficiary designation • Account balance

Uniform Life Table • Used to compute IRA owner’s RMD yearly • Page 3 Table 1

Uniform Life Table • Based on: • Joint life expectancy • Recalculated each year • Hypothetical beneficiary • 10 years younger

Uniform Life Table • Page 3, Table 1 • Age Distribution Period • 70 27.4 • 75 22.9 • 80 18.7 • 85 14.8

Bob, age 70 • IRA balance • $176,000 • Distribution period • 27.4 (Table 1, page 3) • RMD • $176,000 27.4 = $6,423

Recalculated each yr • Age Balance Factor • 71 IRA $$$ ÷ 26.5 • 72 IRA $$$ ÷ 25.6 • 73 IRA $$$ ÷ 24.7 • 74 IRA $$$ ÷ 23.8 • 75 IRA $$$ ÷ 22.9

What if beneficiary is more than 10 years younger than IRA owner? • Doesn’t matter!!!!! • Uniform Lifetime Table for withdrawal calculations must be used

What if spousal beneficiary is more than 10 years younger? • Different Table

Joint Life & Last Survivor Table • Based on • Owner’s Age • Beneficiary’s Age • Page 4, Table 2

Hersh (78) & Mary (67) • IRA balance • $40,000 • Distribution period • 21.0 (Table 2, page 4) • RMD • $40,000 21.0 = $1,905

Recalculated each yr • Hersh & Mary • Ages Balance Factor • 79 & 68 IRA $$$ 20.1 • 80 & 69 IRA $$$ 19.3

Why important to correctly calculate RMD? • 50% penalty

Question #9 • What was the median $$$$ withdrawal from Traditional IRAs in tax year 2002?

Answer: #9 • Median Traditional IRA withdrawal in 2002 • $7,800

Withdrawals from IRAs: When owner is between 59 ½ & 70 ½; & When owner turns 70 ½MontGuide 200309Marsha A. Goetting, MSUKristen G. Juras, School of Law, University of Montana Revised 2003