Download

1 / 28

280 likes | 413 Views

Controlled Capital Account Liberalization. Eswar Prasad & Raghuram Rajan IMF. Plan of Talk. Reserve accumulation—how much, why, and cost-benefit issues Approaches to sterilization Other approaches to dealing with inflows The Prasad-Rajan proposal

E N D

Controlled Capital Account Liberalization Eswar Prasad & Raghuram Rajan IMF

Plan of Talk • Reserve accumulation—how much, why, and cost-benefit issues • Approaches to sterilization • Other approaches to dealing with inflows • The Prasad-Rajan proposal • The proposal in the broader context of new literature on financial globalization • China and India as illustrations

Why the Build-up of Reserves? • Capital flows to emerging markets • Speculative inflows • Current account surpluses • Oil revenues

Benefits of Reserve Accumulation • Reduced vulnerability to crises • Mitigates real exchange rate appreciation • Lowers external borrowing costs

Costs of Reserve Accumulation • Complications for macroeconomic management • Adjustment may come through inflation • Opportunity cost of holding reserves • Quasi-fiscal costs of sterilization • Domestic policy distortions

Sterilization: Instruments/Methods • Repos, open market operations • Central Bank securities • Fx swaps • Government deposits at the Central Bank • Reserve requirements

What Are Countries Doing with Reserves? Actions and Proposals • U.S. bonds (Treasury and Agency) • Other industrial country treasury paper • Bank recapitalization (China) • Infrastructure investment (India) • Korea Investment Corporation

Improving Risk-Return Profile of Reserves • Diversify into non-U.S. $ denominated instruments, gold • Regional pooling of reserves—e.g., Asian Investment Corporation (Genberg et al.) • Invest reserves in broader range of instruments including foreign equities • Asset management by IMF and World Bank (Summers)

Other Policy Actions • Tighter controls on inflows • Liberalization of outflows: • Firms (retain fx earnings, borrow in fx) • Households • Institutional investors (QDII)

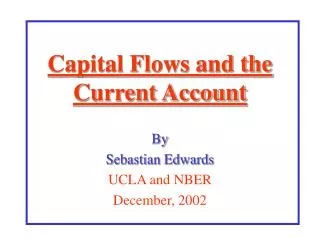

Is There a Way to Do Better? How to Achieve Multiple Objectives? • Get benefits of inflows • Reduce costs of sterilization and fx exposure of Central Banks • Lower risks of capital account liberalization The Prasad-Rajan Proposal

Inflows Reserves $ $ Central Bank RMB RMB Liquidity CB Bills

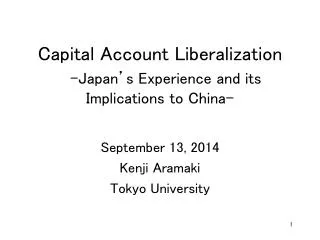

Inflows Investments $ $ $ Central Bank Closed-end Mutual Fund RMB Financial Market Development Controlled Outflows: Quantity + Timing International Portfolio Diversification Sterilization RMB RMB Liquidity Shares

Other Benefits • Provides breathing room for some macroeconomic reforms (fx flexibility) • Fx risk taken off Central Bank’s balance sheet • Securitizing inflows may facilitate reduction in external borrowing costs • Could complement other approaches such as QDII

Potential Concerns • Could delay more fundamental reforms • Governance problems • Multiple exchange rates • Rents to mutual funds if excess demand for securities • Fx risk transferred to households • No demand for securities if expectation of currency appreciation

The Macroeconomic Implications Of Financial Globalization:A Reappraisal And Synthesis The Proposal in a Broader Context Ayhan Kose, Eswar Prasad, Kenneth Rogoff, Shang-Jin Wei

The Traditional View More efficient international allocation of capital Financial Globalization GDP growth Csmn. volatility Capital deepening International risk sharing

A Different Perspective Financial market development Institutions, governance Macroeconomic discipline Competition Financial Globalization GDP growth Csmn. volatility Collateral Benefits

Factors that Influence Outcomes of Financial Integration: Threshold Effects • Financial Sector Development • Institutions, Governance • Macro Policies • Trade Openness • Exchange Rate Regime

TENSION !! • Financial integration helps developing countries to improve their financial markets, enhance governance, impose discipline on macro policies, break power of interest groups that block reforms, etc. • But, in the absence of a basic pre-existing level of these supporting conditions, financial integration can wreak havoc

What’s a Country to Do? • Trade integration to begin with; but often results in de facto financial integration. Works okay, but not ideal substitute • Collateral benefits perspective can guide country-specific sequencing of capital account opening • Controlled capital account liberalization if experiencing inflows, external circumstances favorable