Download

1 / 26

260 likes | 389 Views

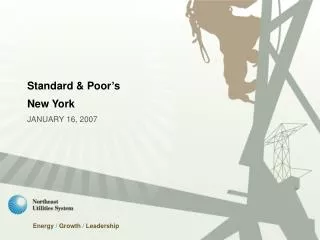

Standard & Poor’s New York JANUARY 16, 2007. Energy / Growth / Leadership. Northeast Utilities. Competitive. Regulated. Retail Sold 6/1/06. Electric Distribution. Wholesale New England Contracts Divested 12/31/05. Electric Transmission. Generation Sold 11/1/06. Gas

E N D

Standard & Poor’s New York JANUARY 16, 2007 Energy / Growth / Leadership

Northeast Utilities Competitive Regulated Retail Sold 6/1/06 Electric Distribution Wholesale New England Contracts Divested 12/31/05 Electric Transmission Generation Sold 11/1/06 Gas Distribution Services 5 of 6 Sold Regulated Generation Strategic Progress - Divestitures We are nearly complete transforming ourselves into a 100% regulated utility

Benefits Of Transformation We have: • Focused our business model and strategy • Reduced our business risk and improved financial flexibility • Capitalized on increasing valuation of generation • Enhanced our earnings visibility • Increased our focus on regulated infrastructure capital investment to meet customers needs Each reason provided a year ago has been validated

How About Generation? • CL&P • Owned about 5,500 MW before 1998-2002 restructuring • Barred by state law from owning generation • Sells output from old PURPA contracts into the market • Bids out 100% of power and capacity needs • Fully recovers costs • WMECO • Owned more than 1,000 MW before 1997-2001 restructuring • Barred by state law from owning generation • Bids out 100% of power and capacity needs • Fully recovers costs • PSNH • Sold nuclear ownership (Seabrook, Millstone 3, VT Yankee), but kept all fossil, hydro generation • Now generates about 70 percent of customer needs; other 30 percent bought through long-term, short-term procurements • Generation charge fully tracks costs and generates 9.62% ROE

Rates Reflect Status Of Each State’s Market 17.79 16.94 16.11 14.38 13.42 13.26 cents/kwh Other includes C&LM, DSM, Stranded Costs (a.k.a. CTA, SCRC or Transition), Consumption Tax, SBC, and Renewables.

Overview of Regulated Businesses In millions of dollars Number of retail customers in thousands as of 9/30/06 * *Includes regulated generation

NU Has Moved Into A Strong Capital Investment Cycle • Need to upgrade transmission system, particularly in SW Connecticut • Continued strong peak load growth • Inadequate generation built in Connecticut • New England generation construction frequently far from load centers • Need to upgrade distribution system • Continued strong peak load growth • Older system, particularly in urban, rural areas

Projected Distribution Capital Expenditures $ Millions

Projected Transmission Capital Expenditures $ Millions

2007-2011: Capital Expenditures and Depreciation *Includes approximately $18 million per year at corporate service companies Significant capital spending in 2007-2008

Projected Combined Rate Base Target Utility Capitalization Structure = 45% equity, 55% debt Recently FERC Authorized Transmission ROE = 11.4%-12.4% Projected PUC Authorized Cost of Capital Distribution ROE = 9% -10% Regulated Rate Base 2006-2011 CAGR of 12% $7,904 $7,437 $7,005 $6,586 $5,755 Projected Distribution & Generation Rate Base CAGR of 7% $4,537 Rate Base in Millions Transmission Rate Base 2006-2011 CAGR of 23% Supports EPS CAGR of 10-14%

Rate Base Composition 2005 Rate Base Composition Electricity Transmission 2005 Rate Base: $3.3 billion Rate Base: $605 million (Actual 2005) ’06-’11 Capex: $2.9 billion Electricity Distribution & Generation Rate Base: $2.25 billion (Actual 2005) ’06-’11 Capex: $2.5 billion 2011E Rate Base Composition 2011E Rate Base: $7.9 billion Gas LDC Rate Base: $463 million (Actual 2005) ’06-’11 Capex: $0.3 billion Transmission to comprise much larger share of total rate base

About Northeast Utilities Transmission… • Comparative Ranking of NU (miles) • Largest in New England • 4th largest in 11 northeast states • Nearly 2.4 million retail customers • About 280 miles of new transmission planned

The Next Five Years: Transmission Capital Expenditures Historic Forecast $1,062 Million Up To $2.4 Billion $1.1 Billion of major CT projects in 2007-2011 forecast period; $1.65 billion in total $ Millions SNETR family of projects estimated at $710 million during the 2007-2011 forecast period • The Southern New England Transmission Reinforcement family of projects is becoming more defined. • Over the next three years, a high level of capital spending is associated with projects that have already received siting approval.

Four Major SW Connecticut Projects – A $1.65 Billion Investment SWCT improvements have been a top priority in each of ISO-NE’s last four regional transmission expansion plans. Our four major projects there total about $1.65 billion in investment. COMPLETE Bethel-Norwalk 345 kV Underground & Overhead $350 Million • 21 miles 345kV (56% underground) • 10 miles 115kV (100% underground) • Completed October 2006 at a cost of $340 million 50% of CT Load Middletown-Norwalk 345 kV Underground & Overhead $1,047 Million (NU Share) Glenbrook Cables 115 kV underground $183 Million Long Island Cable 138 kV cross sound $72 Million (NU share) • 69 miles 345kV (35% underground) • 57 miles 115kV (1% underground) • Joint project with United Illuminating • Projected in-service date: 2009 • Construction under way, 15% complete • 9 miles 115kV underground • Projected in-service date: 2008 • Under contract – construction under way, 10% complete • 11 miles 138kV submarine cable • Joint project with LIPA • Projected in-service date: 2008 • Under contract – cable being manufactured

Percentage of Peak Load that Could Be Served by Transmission Imports 100% 80% 60% 40% 20% 0% VT RI MA ME CT NH Status of Connecticut Transmission Infrastructure Power Moves into Connecticut and SWCT from MA and RI • Within Connecticut transmission constraints exist that limit the flow of power from external sources • Significant transmission enhancements are under construction in SW Connecticut to meet that area’s needs • Future projects are in the planning phase to address power flows into Connecticut Connecticut Southwest Connecticut Norwalk-Stamford 345-kV Lines Boundaries of Major Constraints 345-kV Lines under construction With import capability of only 2,500 MW, CT is the least interconnected state in New England.

Southern New England Transmission Reinforcement Projects Are the Next Major Undertaking • The SNETR projects with National Grid solve four area problems: • Interstate transfer capability • Connecticut East-West transfer capability • Springfield Reliability • New England East-West transfer capability 4 3 1 • 2006 Activities: • Complete planning studies • Analyze routing options • 2007 Activities: • Begin siting process in Connecticut and Massachusetts • ISO-NE technical approval 2 2005 2006 2007 2008 2009 2010 2011 2012 2013 Planning Siting Construction

We Have Selected the Southern New England Transmission Reinforcement Project Preferred Routes The four components, identified to date, are: A Springfield Reliability Component An Interstate Reliability Component A Rhode Island Reliability Component A CT East-West Reliability Component Post-SNETR Import Capability is expected to grow to 3600MW

Sound Progress On Two Largest Projects On Distribution/Generation Side • Conversion of 50 MW coal unit to burn wood • Dramatic reductions in mercury, NOx, SOx emissions • Entered commercial operation 12/1/06 • Completed below $75 million budget • No rate increase due to RECs, tax credits • $108 million 1.2 bcf LNG • Filled from pipeline or via LNG tanker truck • On budget, on schedule • Improve reliability • Save customers money due to lower pipeline charges

2006 NU Transmission Project Performance Summary – Excellence, Execution • Project construction milestones were on-time and spending was on-budget • Capital spending of approximately $470 million in 2006 • Plant-in-service totaling $390 million -- $10 million greater than budget • We have maintained excellent safety and environmental records • We have completed and energized the $340 million Bethel-Norwalk project as of October 12, $10 million under budget • We have completed and energized the new $29 million Killingly substation in northeast Connecticut, $3 million under budget • Completion of projects will result in significant cost savings for customers

Financing The Growth: 2007 Projected Sources Projected Uses • Cash from generation sale: $1 billion • Regulated company long-term debt issuances: $600-$700 million • Cash from operations: $500-$600 million • Capital expenditures: $1.2 billion • Taxes on generation sale: $450-$500 million • Short-term debt reduction: $300-$400 million • Dividends: $125 million Cash from generation sale helps to comfortably fund requirements

Financing The Growth: 2007-2011 $2.5 Billion Cash from Operations $3 Billion New Issuances, and Cash from Generation Sale $5.5 Billion Projected Capital Expenditures and Dividends NU will meet its cash needs almost exclusively from internal sources and debt financings

NU Undergoes Its Second Major Redeployment Of Capital In 8 Years 1999 - 2002 IN OUT • Securitization: $2.1 billion • Millstone sale: $1.2 billion • CT and MA plant sales: $0.5 billion • Seabrook sale: $0.3 billion • Debt, preferred retirement: $1.3 billion • IPP buyouts, buydowns: $1.1 billion • Share repurchases: $0.4 billion • Taxes on Millstone sale: $0.3 billion OTHER • Hydro assets “sold” to NGC • Yankee Energy acquired in 2000 for NU shares, cash • $263 million of debt remains outstanding

Obligations At Year-End (in milions) ** * * * Private placements **Offset by trust account

Likely Issuances in 2007 • CL&P • $500 million of FMBs ($300 in March) • WMECO: • $40 million of senior unsecured in second quarter • Yankee: • $35 million private placement in second quarter • PSNH: • $50 million of FMBs later in year

Main NU Contacts David McHale CFO 860-665-5601 mchaldr@nu.com Jeff Kotkin VP – IR 860-665-5154 kotkij@nu.com Randy Shoop Treasurer 860-665-3259 shoopra@nu.com Patricia Cosgel Asst. Treasurer 860-665-5058 cosgepc@nu.com Bud Eckenroth Dir. Financial Policy 860-665-3693 eckengj@nu.com Greg Osgood Dir. Financial Forecasting 860-665-5310 osgooga@nu.com Don Haight Mgr. Financial Policy 860-665-5507 haighdw@nu.com Barbara Nieman Investor Relations Spec. 860-665-3249 niemabf@nu.com