Download

1 / 20

200 likes | 504 Views

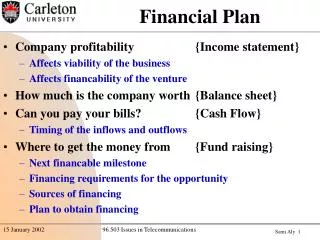

The Financial Plan Contributed by Arya Kumar Chief ED & IPR Unit BITS, Pilani Financial objectives are both the starting & finishing point of a good business plan.

E N D

The Financial Plan Contributed byArya KumarChief ED & IPR UnitBITS, Pilani

Financial objectives are both the starting & finishing point of a good business plan. The Financial plan seeks to reflect the financial implications of your marketing, people and operational plans in the form of profit-loss accounts, cash flows, and balance sheets.

Planning Assumptions • Example - SARAVANA BHAVAN Saravana bhavan will set up and operate a small chain of south-indian restaurants in UK. These will provide traditional south-indian food in a relaxed atmosphere offering value-for-money food in the middle priced NRI market. The chain of Saravana Bhavan is already a proven concept in parts of Indian subcontinent, serving south-indian food on a quick throughput basis but without the fast-food image. Labour costs are low and with a limited menu, waste is avoided and in turn makes value for money possible. One Saravana Bhavan has been in operation for six months in London, so the following assumptions have been drawn partly from experience and partly from market research.

Profit & Loss Assumptions • A) Sales • Number of outlets in operation will be : • Year 1 2 • Year 2 4 • Year 3 7 • Year 5 onwards 10 • Operating six days a week, meals sales will be : • Year 1 40 per day • Year 2 50 per day • Year 3 onwards 60 per day • Sales value per meal will be : • Food £ 6.50 • Drink £ 2.50 • B) Cost of sales per meal • Food £ 1.75 • Drink £ 1.00 • Labour £ 2.70 • Total £ 5.45 This equals 61 % of sales.

Profit & Loss Assumptions • C) Wages: each outlet will employ seven staff at a cost of £ 42,600 per annum (labour costs = 30 % of sales, which compares favorably with a general restaurant’s 40 percent). • D) Directors: paid £ 15,000 per year, rising to £ 20,000 from year 3. • E) Administrative staff: needed mainly from year 2. Costs will rise from £ 5,000 to £ 40,000 over seven years. • F) Rent and services : £ 30,000 per outlet per annum • G) Alterations, equipment and decoration : £ 40,000 per outlet. • H) Advertising : £ 2.000 per outlet per annum • I) Inflation: all income and expenditure is stated at current prices.

Cash-Flow assumptions • No debtors – all meals paid in cash • Salaries and wages paid monthly • Purchases paid monthly • Rent paid half-yearly • Rates paid monthly • Loan interest paid quarterly from month 1 • Overdraft interest paid quarterly from month 3 • Sales spread evenly over each month of year Balance sheet assumptions • Closing stock : building up to six weeks’ sales • Depreciation of fixed assets: improvements and office, 20 percent per annum; fixtures and fittings, 25 percent per annum • Creditors: Equivalent to one month’s cost of sales

Once the set of assumptions is made one has to take care of the following : • Key assumptions • Basis of each Assumption • Confidence in each assumption • What will happen if the assumption proves incorrect • When contingency action can be taken, when it should actually be taken

Income Statement or Profit & Loss Account • A financial statement for companies that indicates how Revenue (money received from the sale of products and services before expenses are taken out, also known as the "top line") is transformed into net income (the result after all revenues and expenses have been accounted for, also known as the "bottom line"). The purpose of the income statement is to show managers and investors whether the company made or lost money during the period being reported.

Cash-Flow Statement • A financial statement that shows a company's incoming and outgoing money (sources and uses of cash) during a time period (often monthly or quarterly). The statement shows how changes in balance sheet and income accounts affected cash and cash equivalents, and breaks the analysis down according to operating, investing, and financing activities.

Balance Sheet • A summary of a persons or organization's assets, liabilities and Ownership equity on a specific date, such as the end of its financial year. A balance sheet is often described as a snapshot of a company's financial condition.

Financing a New Venture • Financial assistance to entrepreneurs is available from institutions such as Nationalized banks, Small Industries Development Bank of India, Regional Rural Banks,etc…. depending upon the project requirement and promoters background. • Financial assistance has two components : • Loan for Fixed Capital • Loan for Working Capital

Industrial Finance in India • National Level Industrial Development Banks • Industrial Development Bank of India (IDBI) • Industrial Finance Corporation of India (IFCI) • Small Industries Development Bank of India (SIDBI) • Industrial Reconstruction Bank of India (IRBI) • Shipping Credit and Investment Company of India (SCICI) • Specialized Financial Institutions • Technology Development & Information Company of India Limited (TDICI) • Risk Capital & Technology Finance Corporation Limited (RCTC) • Tourism Finance Corporation of India (TFCI)

Industrial Finance in India • Investment Institutions • Unit Trust of India (UTI) • General Insurance Corporation of India (GIC) • Life Insurance Corporation of India (LIC) • Other Banks Offering Financial Assistance • Small Industries Development Bank of India (SIDBI) • Industrial Development Bank of India • Industrial Finance Corporation of India • ICICI Bank • National Bank for Agriculture and Rural Development (NABARD) • State Bank of India

Venture Capital • Venture Capital - Venture capital is a type of private equity capital typically provided by professional, outside investors to new, growth businesses. • Venture capital investments are generally made as cash in exchange for shares in the invested company.

Venture Capitalists Generally : • Finance new and rapidly growing companies • Purchase equity securities • Assist in the development of new products or services • Add value to the company through active participation • Take higher risks with the expectation of higher rewards • Have a long-term orientation • Some Venture Capital Organizations • ICICI Venture Funds Management Company Limited • SIDBI Venture Capital Limited (SVCL) • IFCI Venture Capital Funds Ltd. (IVCF) • Gujarat Venture Finance Limited (GVFL) • IL & FS Group Businesses

Venture Capital Financing Process • In general the Venture Capital Financing Process is divided into 5 different stages: • The SEED Stage – In this stage relatively small amounts of capital is used to prove concepts & finance feasibility studies. • The START-UP Stage – In this stage funding is done for product development and initial marketing, but with no commercial sales yet (basically to get operations started). • The SECOND Stage – In this stage working capital is used for initial growth phase, but no clear profitability or cash flow yet. • The THIRD Stage – In this stage financing is done for major expansion for company with rapid sales growth, at break even or positive profit levels but still private company. • The BRIDGE/PRE-PUBLIC Stage – In this stage Bridge financing is done so as to prepare the company for public offering. EARLY- STAGE FINANCING EXPANSION or DEVELOP-MENT FINANCING