Understanding Capital Asset Pricing Model (CAPM) and Investment Opportunities

110 likes | 206 Views

Learn about the CAPM model by Sharpe & Markowitz, the concept of beta, risk types, investment opportunities, and stock risks. Explore how CAPM determines required returns and assesses market risks. Discover practical applications in investment decisions.

Understanding Capital Asset Pricing Model (CAPM) and Investment Opportunities

E N D

Presentation Transcript

CAPITAL ASSET PRICING MODEL(CAPM) It is developed by Professors Sharpe & Markowitz in 1960. Prof Sharp won Nobel Prize in 1990

Types of investors • Risk taker: The investor who take risk. • Risk Aversor: The investor who avoided risk and if he take risk he ask for more reward and in this case it is risk premium.

CAPM Defined • It is a model which describes the relationship between risk and expected (required) return. • In this model a security expected (Required) return is equal to risk free rate and risk premium based on the systematic risk of the security.

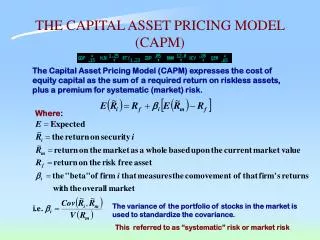

Mathematically CAPM is written as Rj= Rf + Bj (Rm – Rf) Where: Rj = Required (expected) rate of return of security j Rf = Risk free rate of short term govt bond Bj = It is the systematic risk of security “j” which can not be diversified. Rm = Required rate of return of market (KSE 100 index) (Rm – Rf) = Risk premium because of bearing risk “B” (beta)

Assumption of CAMP • The capital market is efficient, in that investor are well informed. • No transaction cost. • Negligible restriction on investment. • No investment is large enough to effect the market price of a stock. • There is no taxes. • The quantities of all assets are given fixed. • All assets are perfectly divisible and perfectly liquid.

Investment Opportunities • Investment in risk free securities whose return are fixed. Short term rate is used is CAPM. • Market portfolio of common stock.

Beta • It is a tendency of a Stock to move with the Market (or Portfolio of all Stocks in the Stock Market). it is the building block of CAPM. Total Risk = Diversifiable Risk + Market Risk Total Stock Return = Dividend Yield + Capital Gain Yield

Stock Risk Vs Stock Beta: Stock Risk: • It is a statistical spread of possible returns (or Volatility) for that Stock Stock Beta: • It is a statistical spread of possible returns (or Volatility) for that Stock relative to the market spread i.e. spread (or Volatility) of the fully diversified market portfolio or index. • Beta Coefficients of Individual Stocks are published in “Beta Books” by Stock Brokerages & Rating

Meaning of Beta for Share ABC in Karachi Stock Exchange (KSE): • If Share A’s Beta = +2.0 then that Share is Twice as risky (or volatile) as the KSE Market i.e. If the KSE 100 Index moved up 10% in 1 year, then based on historical data, the Price of Share B would move up 20% in 1 year. • If Share B’s Beta = +1.0 then that Share is Exactly as risky (or volatile) as the KSE Market • If Share C’s Beta = +0.5 then that Share is only Half as risky (or volatile) as the KSE Market • If you could find a Share D with Beta = -1.0 then that share would be exactly as volatile as the KSE Market BUT in the opposite way i.e. If the KSE 100 Index moved UP 10% then the price of the Share D would move DOWN by 10%! • The Beta of most Stocks ranges between + 0.5 and + 1.5 • The Average Beta for All Stocks = Beta of Market = + 1.0 Always.