Download

1 / 36

420 likes | 866 Views

Chapter 13: The Capital Asset Pricing Model. Objective The Theory of the CAPM Use of CAPM in benchmarking Using CAPM to determine correct rate for discounting. Chapter 13 Contents. The Capital Asset Pricing Model in Brief Determining the Risk Premium on the Market Portfolio

E N D

Chapter 13: The Capital Asset Pricing Model • Objective • The Theory of the CAPM • Use of CAPM in benchmarking • Using CAPM to determine • correct rate for • discounting

Chapter 13 Contents • The Capital Asset Pricing Model in Brief • Determining the Risk Premium on the Market Portfolio • Beta and Risk Premiums on Individual Securities • Using the CAPM in Portfolio Selection • Valuation & Regulating Rates of Return • Modifications and Alternatives to the CAPM

Introduction • CAPM is a theory about equilibrium prices in the markets for risky assets. • It is important because it provides • A justification for the widespread practice of passive investing called indexing, and • A way to estimate expected rates of return for use in evaluating stocks and projects.

The Capital Asset Pricing Model in Brief • CAPM is an equilibrium theory based on the theory of portfolio selection. • The basic question: What would risk premiums on securities be in equilibriumif people had the same set of forecasts of expected returns and risks, and all chose their portfolios optimally according to the principles of efficient diversifications?

Assumptions of CAPM • Assumption 1 (homogeneous in information processing) Investors agree in their forecasts of expected rates of return, standard deviation, and correlations of the risky securities. • Assumption 2 (homogeneous in behavior) Investors generally behave optimally according to the theory of portfolio selection.

Intuitive of CAPM • All the investors will allocate their investments between the riskless asset and the same tangent portfolio. • In equilibrium, the aggregate demand for each security is equal to its supply. • The only way the asset market can clear is if the relative proportions of risky assets in tangent portfolio are the proportions in which they are valued in the market place, i.e. the market portfolio.

Expected Return (%) CML Market Portfolio ● E(rM)- rf rf sM The Capital Market Line (CML) Lending Borrowing Standard Deviation s

Efficient Risk-Reward • In equilibrium, any efficient portfolio should be a combination of the market portfolio and the riskless asset. • The best risk-reward depends on how much the market-related risk a portfolio bears.

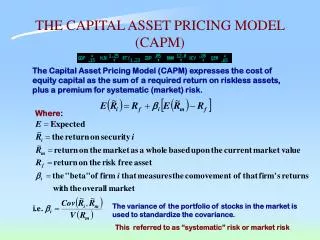

Determining the Risk Premium on the Market Portfolio • The equilibrium risk premium on the market portfolio is the product of • variance of the market, σ2M • weighted average of the degree of risk aversion of holders of risk, A

Team Work • To express the covariance between a risky security and the tangent portfolio, Cov(ri, rT) , in our example in Chapter 12, as the functions of rf , E[ri], E[rT], and σT .

Expected Return SML E(rM) Market Portfolio rf Risk = b 1 Security Market Line (SML)

A Simple Derivation of CAPM • Utility maximization • risk tolerance, risk-adjusted expected return

A Simple Derivation of CAPM • For investor k • Aggregation

The Beta of a Portfolio • When determining the risk of a portfolio • using standard deviation results in a formula that’s quite complex • using beta, the formula is linear

Return SML · Q . · Market Portfolio A rf Risk = bi 1 Mispriced

Risk Decomposition • Total risk for a security = Market risk + Unique risk • Since the unique risk can be diversified out, the market compensates only for the market-related risk.

Using the CAPM in Portfolio Selection • Passive portfolio management • Proxy for market portfolio • indexing • Active portfolio management • Positive ALPHA • Beat the market

The Market Portfolio and Index Funds • The most important implication of CAPM, that the market portfolio is an efficient portfolio, forms the theoretical basis for constructing proxies of the market portfolio—the index portfolio and index funds. • However, structuring an index portfolio from the primitive securities and making adjustments are inefficient and costly. • The efficient and cheap instruments, index futures contracts were not available until 1982. • In the U.S. market, the market value of outstanding index funds was only 6 million dollars in 1971. • After ten years, the value increased to 10 billion dollars. • In 1992, the value increased to 270 billion dollars with about 1/3 pension funds being in the state of indexing.

Valuation and Regulating Rates of Return • Discounted Cash Flow Valuation Models • Suppose you are considering investing in a new project in the same industry of Betaful Corp. • The market rate is 15%, and the risk-free rate is 5%. • The beta of Betaful’s stock is 1.3. • The capital structure of Betaful: 80% of equity, 20% of bond.

Valuation and Regulating Rates of Return • Compute the beta of Betaful’s operations

Valuation and Regulating Rates of Return • Beta of Betaful’s operations is equal to the beta of the new project. • Applying the CAPM to find the required return on the new project. Cost of capital

Valuation and Regulating Rates of Return • Assume that you start up a company which is just a vehicle for the new project, 60% capital is financed by issuing equity and 40% by issuing bond. • The beta of your unquoted equity is

Valuation and Regulating Rates of Return • Your company is all-equity financed. • Your company has an expected dividend of $6 next year, and that it will grow annually at a rate of 4% for ever, the value of a share is

Modifications and Alternatives to CAPM • Empirical testing of CAPM • Modifications • The proxy of market portfolio • Market imperfection • Multifactor Intertemporal CAPM (ICAPM): beta, sensitivity to changes in interest rates and in consumption good prices • Alternatives • Arbitrage Pricing Theory (APT)