Download

1 / 25

250 likes | 272 Views

Improve your understanding of management processes by exploring planning, directing, motivating, and controlling through the lens of budgeting. Learn about the benefits of budgeting, advantages in goal setting, coordination, and responsibility accounting. Dive into different types of budget systems and participatory budgeting approaches. Test your knowledge with practical examples on sales budgeting, production planning, and raw material purchases. Discover the motivational side of budgeting and its impact on organizational performance.

E N D

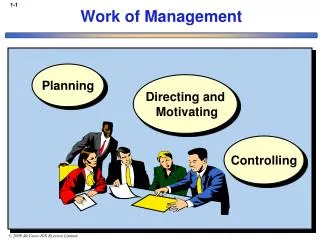

Work of Management Remember! Planning Directing and Motivating Controlling

Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control -- involves the steps taken by management that attempt to ensure the objectives are attained. Planning and Control

Which of the following is not a benefit of budgeting? • It uncovers potential bottlenecks before they occur. • It coordinates the activities of the entire organization by integrating the plans and objectives of the various parts. • It ensures that accounting records comply with generally accepted accounting principles. • It provides benchmarks for evaluating subsequent performance.

Advantages of Budgeting Define goal and objectives Communicating plans Think about and plan for the future Advantages Coordinate activities Means of allocating resources Uncover potential bottlenecks

Responsibility Accounting Managers should be held responsible for those items — and only those items — thatthe manager can actually controlto a significant extent.

Fairmont Inc. uses an accounting system that charges costs to the manager who has been delegated the authority to make decisions concerning the costs. For example, if the sales manager accepts a rush order that will result in higher than normal manufacturing costs, these additional costs are charged to the sales manager because the authority to accept or decline the rush order was given to the sales manager. This type of accounting system is known as: A) responsibility accounting. B) contribution accounting. C) absorption accounting. D) operational budgeting.

Choosing the Budget Period Operating Budget 1999 2000 2001 2002 The annual operating budget may be divided into quarterly or monthly budgets.

Choosing the Budget Period Continuous or Perpetual Budget 1999 2000 2001 2002 This budget is usually a twelve-month budget that rolls forward one month as the current month is completed.

Participative Budget System Flow of Budget Data

The Budget Committee A standing committee responsible for • overall policy matters relating to the budget • coordinating the preparation of the budget

A method of budgeting in which the cost of each program must be justified every year is called: • operational budgeting. • zero-based budgeting. • continuous budgeting. • responsibility accounting.

Zero-Base Budgeting Managers are required to justify all budgeted expenditures, not just changes in the budget from the previous year. The baseline is zero rather than last year’s budget.

Parlee Company's sales are 30% in cash and 70% on credit. Sixty percent of the credit sales are collected in the month of sale, 25% in the month following sale, and 12% in the second month following sale. The remainder are uncollectible. The following are budgeted sales data: Total sales:January $60,000 February $70,000 March $50,000 April $30,000 Total cash receipts in April would be budgeted to be: A) $38,900. B) $47,900. C) $27,230. D) $36,230.

Modesto Company produces and sells Product AlphaB. To guard against stockouts, the company requires that 20% of the next month's sales be on hand at the end of each month. Budgeted sales of Product AlphaB over the next four months are: Budgeted sales in units JuneJulyAugustSeptember 30,000 40,000 60,000 50,000 Budgeted production for August would be: A) 62,000 units. B) 70,000 units. C) 58,000 units. D) 50,000 units.

Friden Company has budgeted sales and production over the next quarter as follows: AprilMayJune Sales in units 100,000 120,000 ? Production in units 104,000 128,000 156,000 The company has 20,000 units of product on hand at April 1. A minimum of 20% of the next month's sales needs in units must be on hand at the end of each month. July sales are expected to be 140,000 units. Budgeted sales for June would be (in units): A) 188,000. B) 160,000. C) 128,000. D) 184,000

Marple Company's budgeted production in units and budgeted raw materials purchases over the next three months are given below: January FebruaryMarch Budgeted production (in units) 60,000 ? 100,000 Budgeted raw materials purchases (in kilograms) 129,000 165,000 188,000 Two kilograms of raw materials are required to produce one unit of product. The company wants raw materials on hand at the end of each month equal to 30% of the following month's production needs. The company is expected to have 36,000 kilograms of raw materials on hand on January 1. Budgeted production for February should be: A) 105,000 units. B) 82,500 units. C) 150,000 units. D) 75,000 units.

Budgets can be defined as: “a quantitative model, or summary of the expected consequences of the organization’s short-term operating activities.” Management Accounting Atkinson, Banker, Kaplan & Young What is this definition implying?

The definition suggests: • Availability of quantitative data, • Predictability of short-term outcomes, • Clear-cut organizational structures. There is one major logical problem, which is? If the above are true, what do you need the budget for?

The budgetary process is rather a process • To quantify “qualitative” judgment, • To forecast the impacts of some uncertain events, • To simplify the complex organizational structures.

As Zimmerman indicated (p.244), the budget process • is a communication device involving both vertical and horizontal information transfer • is a negotiation and internal contracting procedure • is part of the performance evaluation system • partition decision rights

Budgets to Solve “Agency” Problems • Short-term budgets as internal contracts. • To formally commit responsibility centers • As a warning for future monitoring actions • Long-term budgets to reduce information asymmetry. • To solicit private, specialized information from local managers • Force managers to think strategically, rather than on just the short-term results

Budgets to Solve “Agency” Problems • Line-item budgets • Authorize managers to spend only up to a certain amount per line item • Cannot transfer excess to and from line-items • No incentive to reduce spending • Budget lapsing – no carryovers to next period • Incentive to spend all the budgeted amounts • Intend to avoid managers building up slacks and smoothing performance over time

International Aspects of Budgeting • Multinational companies face special • problems when preparing a budget. • Fluctuations in foreign currency exchange rates. • High inflation rates in some foreign countries. • Differences in local economic conditions. • Local governmental policies.