Download

1 / 1

10 likes | 151 Views

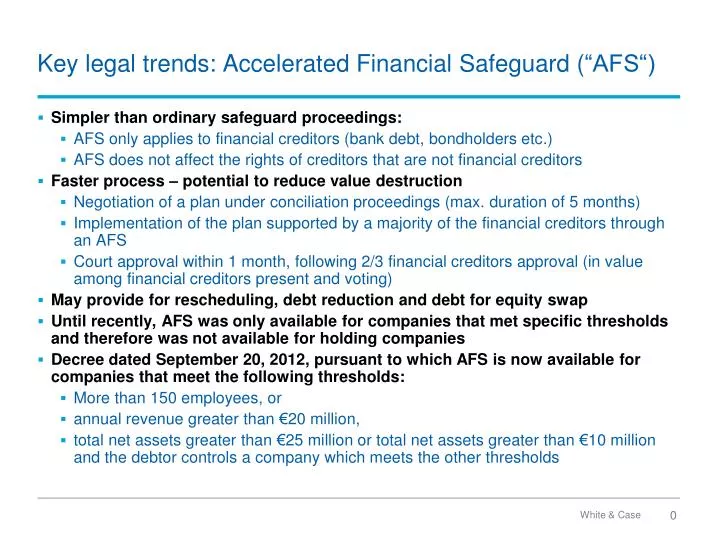

Key legal trends: Accelerated Financial Safeguard ( “AFS“). Simpler than ordinary safeguard proceedings: AFS only applies to financial creditors (bank debt, bondholders etc .) AFS does not affect the rights of creditors that are not financial creditors

E N D

Key legal trends: Accelerated Financial Safeguard (“AFS“) • Simpler than ordinary safeguard proceedings: • AFS only applies to financial creditors (bank debt, bondholders etc.) • AFS does not affect the rights of creditors that are not financial creditors • Faster process – potential to reduce value destruction • Negotiation of a plan under conciliation proceedings (max. duration of 5 months) • Implementation of the plan supported by a majority of the financial creditors through an AFS • Court approval within 1 month, following 2/3 financial creditors approval (in value among financial creditors present and voting) • May provide for rescheduling, debt reduction and debt for equity swap • Until recently, AFS was only available for companies that met specific thresholds and therefore was not available for holding companies • Decree dated September 20, 2012, pursuant to which AFS is now available for companies that meet the following thresholds: • More than 150 employees, or • annual revenue greater than €20 million, • total net assets greater than €25 million or total net assets greater than €10 million and the debtor controls a company which meets the other thresholds