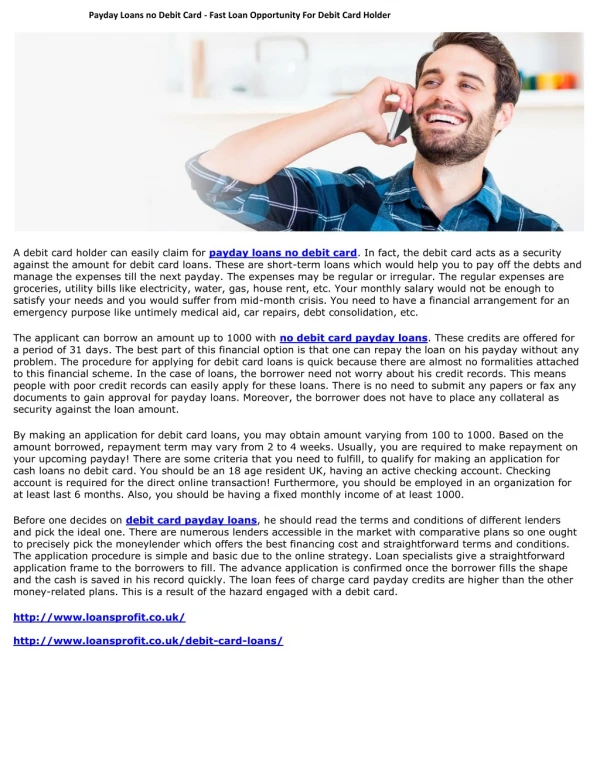

Download

1 / 15

150 likes | 253 Views

Analysis of European Debit Card MSC Differences. TARJETAS DE PAGO Y TASAS DE INTERCAMBIO Madrid, 2 nd February 2006. Objectives. Test the hypothesis:

E N D

Analysis of European Debit Card MSC Differences TARJETAS DE PAGO Y TASAS DE INTERCAMBIO Madrid, 2nd February 2006

Objectives Test the hypothesis: “That the level of debit MSC in any market is substantially linked to the maturity of its domestic EftPos payments infrastructure and the effectiveness of its national displacement strategy”. Specifically to: • Identify the sources of Merchant Service Charge (MSC) differences within Europe • Explore the relationship between Europe’s varied MSC levels and the level of debit usage • Identify potential causes of differences between national debit markets • Support PSE’s position that imposing a common European debit interchange could have unforeseen impacts, and that a lengthy convergence period would be required.

Scope and Methodology Scope: • Major EU Cards Markets (Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Netherlands, Norway, Portugal, Spain, Switzerland, and the UK) • National data from Eastern European nations on historical and current card and cash usage was not yet regarded as sufficiently reliable, or comparable, to allow inclusion.

HEADLINE MSC Rates Acquired Volumes/ Cross Border Values Transactions Terminal/ Merchant Settlement/ Float Support Costs Costs NORMALISED MSC Rates Headline European MSC Rates Current MSC Rates in Europe PSE Normalisation Approach Current Headline Rates are Currently Non-Comparable

Rate Variation within the EU Substantial Variations Still Exist in the MSC Rate Structures

Impact of Normalisation Normalised MSC Rates in Europe Impact of Normalisation Average MSCs drop by 5% following Normalisation, with Spanish Rates falling by 25%

Usage and Maturity Variation in the EU Total Value of Debit POS (per annum per capita) Volume of Debit POS Transactions (per annum per capita) Wide range of Maturity Levels within the Western European Market for POS usage

The DCD Metric in the EU DCD Scores 1996-2005 • Scores range from 1% to 69% • Majority of countries have experienced increases in their DCD metrics over the past ten years, a reflection of their maturing debit card market

The MSC DCD Relationship The MSC DCD Relationship (2005) Analysis indicates a relationship between the DCD score and the level of MSCs

Answer to the most frequently asked question… “…this analysis proves the hypothesis that countries with very low or no MSCs have successful EftPOS strategies” Country comparisons show that this is not so: • Germany has a debit MSC of c.€0.3 but has one of the lowest card transactions per head of population per annum • France also has a debit MSC of c.€0.3 but has one of the highest card transactions per head of population per annum (also has high card/ bank accounting fees) The MSC Debit Usage Relationship (2005) …lower MSCs do not reflect successful cash displacement or EftPOS strategies

Characteristics of Less Developed Countries • Lack of a coherent national cash displacement strategy and strong central leadership. This results in a fragmented approach to EftPos. • Difficulty in building early support for debit card EftPos amongst the largest merchants and supermarkets. • Business models that vary substantially from those of successful countries, such as: • Three party structures which eliminate the use of an acquiring bank and operate without a MIF generating insufficient revenues to incentivise consumers and deliver merchant benefits. • Bundled MSC structures, complex MIF formulae and merchant contracts. • Fragmented and complex acquiring structures which result in multiple terminal placement, loss-making acquiring and insufficient funds to change consumer behaviour. • Strong consumer cultural propensity to use cash

Summary and Conclusions • There is a negative correlation between the simple DCD metric and the level of normalised debit MSC • These differences are necessary and that inappropriate intervention may have undesirable consequences on the development of domestic payment infrastructure. • If working effectively, card markets will converge over time around lower debit MSC levels as card payments displace cash usage. • Successful cash displacement strategies reflect clear national direction, strong competitive commercial frameworks, and good incentives to invest in infrastructures, change consumer behaviour and deliver merchant benefits.

Peter JonesManaging DirectorChris Jones Senior Consultant+44 (0) 20 8891 6244info@pseconsulting.com