Understanding Bad Debt and Allowance Method in Accounting Transactions

This article delves into the concept of bad debt expense and the allowance method in accounting. It outlines how businesses estimate future uncollectibles, examines the adjusting journal entries required at year-end, and illustrates how to handle write-offs for accounts receivable deemed uncollectible. Additionally, it provides examples of journal entries for specific sales and interest accruals, ensuring a concise understanding of their impact on financial statements and accounting records. Ideal for students and professionals in finance and accounting.

Understanding Bad Debt and Allowance Method in Accounting Transactions

E N D

Presentation Transcript

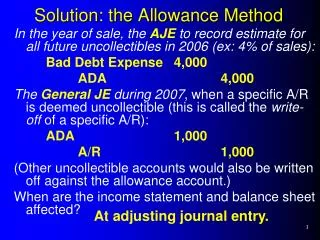

In the year of sale, the AJE to record estimate for all future uncollectibles in 2006 (ex: 4% of sales): Bad Debt Expense 4,000 ADA 4,000 The General JEduring 2007, when a specific A/R is deemed uncollectible (this is called the write-off of a specific A/R): ADA 1,000 A/R 1,000 (Other uncollectible accounts would also be written off against the allowance account.) When are the income statement and balance sheet affected? Solution: the Allowance Method At adjusting journal entry.

Given the following information: At December 31, 2007, Company Z prepared an aging schedule to determine that the uncollectible accounts receivable at that date were $18,000. The balance in the Allowance for Doubtful Accounts at 1/1/07 was a $3,000 credit. During 2007, the company wrote off $5,000 of specific accounts receivable that were deemed to be uncollectible. Required: prepare the AJE to record the estimated uncollectibles at 12/31/07. Class Problem 1

Solution to Class Problem 1 (1) Post the beginning balance and write-off. (2) Post the desired ending balance. (3) Post the adjusting journal entry. Allowance for Doubtful Accounts 3,000 Beginning (1) (1) W/O 5,000 20,000 AJE (3) 18,000 End. Balance (2) AJE: Bad debt expense 20,000 Allowance for D.A. 20,000

On November 1, 2008, Pistol Pete’s Western Gear sold merchandise totaling $10,000 to the Orange Cow Company. Pete’s accepted a note containing a 6 % annual interest rate, where interest and principal were to be repaid in 3 months, on January 31, 2009. Prepare the journal entries for Pistol Pete’s on the following dates: 1. Sale on November 1, 2008 (ignore COGS). 2. Interest accrual at December 31, 2008. 3. Collection of note and interest at January 31, 2009. Class Problem 2

1. Sale on November 1, 2008: 2. Interest accrual at December 31, 2008: 3. Collection of loan and interest at 1/31/09: Class Problem 2 Notes Receivable 10,000 Sales Revenue 10,000 Interest Receivable 100 Interest Revenue 100 Cash 10,150 Notes Receivable 10,000 Interest Receivable 100 Interest Revenue 50

1. a. Percent of sales 2% of 834,000 = 16,680 Bad Debt Expense 16,680 Allowance 16,680 (balance in Allow. not relevant to current JE) Exercise 7-2

Exercise 7-2 1.b Analyze Allowance: Allowance for Doubtful Accounts 2,600 Before AJE (1) 16,606 AJE (3) 19,206 End. Balance (2) AJE: Bad debt expense 16,606 Allowance for D.A. 16,606

Exercise 7-2 2.a. No difference 2.b. Analyze Allowance: Allowance for Doubtful Accounts (1) Before AJE 2,600 21,806 AJE (3) 19,206 End. Balance (2) AJE: Bad debt expense 21,806 Allowance for D.A. 21,806

1. Aging Schedule: % Uncoll. Current 200,000 x .10 = 20,000 < 1 mo. 60,300 x .25 = 15,075 1-2 mos. 35,000 x .35 = 12,250 > 2 mos. 45,000 x .75 = 33,750 Total 340,300 81,075 End Allow 2. Show higher uncoll. for that customer (don’t write off until bankruptcy court settles assets) Problem 7-2A

3. Balance sheet Accts. Receivable $340,300 Less: Allowance for DA 81,075 A/R Net $259,225 Problem 7-2A

Part 1 (1)Sales: A/R (80%) 630,000 Cash (20%) 157,500 Sales 787,500 (2)Collection on A/R: Cash 502,500 A/R 502,500 (3) Write-off of specific A/R: Allow. for Doubt. Acct 3,000 A/R 3,000 Problem 7-1A

Part 2a: % of Sales Bad Debt Expense is % of credit sales Sales x % = Bad Debt Expense (no analysis of Allowance necessary) Sales on account (credit sales) = 630,000 x .03 = 18,900 BD Exp. AJE(2a): Bad Debt Expense 18,900 Allow. for D.A. 18,900 Problem 7-1A

Problem 7-1A (% of Sales) Post A/R: Then post Allowance: (ending balance last) Accts. Receivable Allowance for D A B 105,000 1,950 B (JE1) 630,000 502,500 (JE2) 3,000 (JE3) 18,900 (AJE) (JE3) 3,000 E 229,500 17,850 E Part 3: Net A/R = 229,500- 17,850 = 211,650

Problem 7-1A (2b, % of A/R) Post A/R (same): Then post Allow: (AJE Last) Accts. Receivable Allowance for D A B 105,000 1,950 B (JE1) 630,000 502,500 (JE2) 3,000 (JE3) (3) 3,000 14,820 (AJE) E 229,500 13,770 E Calc. 6% before AJE AJE: Bad debt expense 14,820 Allowance for D.A. 14,820 Part 3: Net A/R = 229,500 - 13,770 = $215,730

Recognition of Bad Debt Expense (AJE): BDExp xx (+Exp, -NI) Decr. SE Allow xx (+Allow) Decr. Assets Write-off: Allow xx (-Allow) Incr. Assets A/R xx (-A/R) Decr. Assets No effect on total assets No effect on I/S No effect on Net A/R Problem 7-1A, Part 4