Download

1 / 25

250 likes | 403 Views

2008: let the fight begin. PETER BROOKE Head Macro Strategy Investments. What did we say last time. What did we say last time. Jan 2007 Equities have re-rated but there is still some beef on the bull Cash may be attractive in the next 12 months but it is NOT a growth asset

E N D

2008:letthefight begin PETER BROOKEHeadMacro Strategy Investments UT\PressConf_0108_RSpeter

What did we say last time What did we say last time Jan 2007 • Equities have re-rated but there is still some beef on the bull • Cash may be attractive in the next 12 months but it is NOT a growth asset • Overweight growth assets: equity and property June 2007 • “Total returns will be lower across all asset classes” • “High earnings and a maturing cycle will lead to greater equity volatility” • Look at lower equity funds: Old Mutual Stable Growth UT\PressConf_0108_RSpeter

Asset Class ReturnsFor the 12 Months to 31.12.07 US Dollars Returns Rand Returns SA Equities SWIX SA Listed Property SA Bonds SA Cash Int’l Returns MSCI AC World Emerging Market Bonds Cash 18.7 26.5 4.3 9.4 6.2 35.5 7.4 1.0 18.7 26.5 4.3 9.4 6.2 35.5 7.4 1.0 21.8 30.6 7.6 12.8 9.6 39.8 10.8 4.2 UT\PressConf_0108_RSpeter

recession vs reflation UT\PressConf_0108_RSpeter

Newspaper* stories that mention ‘recession’ 2,000 1,500 This summer the R word comes back 1,000 500 0 1990 95 2000 05 08** * In the New York Times and the Washington Post ** Q1 forecast Source: Factiva.com UT\PressConf_0108_RSpeter

Growth expectations falling • US housing starts 38% down YoY • Sub-prime crisis spreading • US consumer / wealth effect • Financial system / access to credit • UK house prices to fall ML Global Manager Survey UT\PressConf_0108_RSpeter

But central banks will react • Bad news will bring relief through interest rates • The Fed has cut 100bps and is expected to cut another 150bps • Bond yields are also helping • Other Central Banks are coming to the party with Canada & the BOE cutting US rate expectations falling sharply 6 5 4 3 US: Rate expectations 2 1 0 -1 -2 Jul-05 Jul-07 Jul-06 Jan-05 Jan-06 Jan-07 Mar-05 Mar-06 Mar-07 Sep-05 Nov-05 Sep-07 Nov-07 Nov-06 Sep-06 May-05 May-07 May-06 UT\PressConf_0108_RSpeter

cyclical vs secular UT\PressConf_0108_RSpeter

Developed cyclical slowdown • OECD lead indicator down -1.8% YoY • Spreading into Europe & Japan • German ZEW index down to -42 100 110 80 105 60 40 100 20 95 0 -20 90 -40 ZEW 85 -60 IFO expectations -80 80 Jul-95 Jul-00 Jul-05 Jan-93 Jan-98 Jan-03 Jan-08 Mar-92 Mar-97 Mar-02 Mar-07 Nov-93 Sep-94 Nov-98 Sep-99 Nov-03 Sep-04 May-96 May-01 May-06 UT\PressConf_0108_RSpeter

Vs. Emerging market structural change • More than half the worlds economy on a PPP basis is in developing countries • 86% of the world’s population is in the developing world! • Decoupling: More than half of Chinese exports are outside the G7 Share of world GDP (PPP) 22.5 22.5 20.0 USA 20.0 17.5 17.5 15.0 15.0 12.5 12.5 China 10.0 10.0 7.5 7.5 5.0 5.0 2.5 2.5 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 UT\PressConf_0108_RSpeter

South Africa cyclical slowdown • The South African economy is also battling with a cyclical slowdown. • There is clear evidence that the 400bps of hikes are starting to work: • Vehicle sales -18% YoY • Building plans passed -9.4% YoY • Retail sales only up 0.2% YoY UT\PressConf_0108_RSpeter

Vs. Improvement in long-term growth trend • Trend in real GDP growth has improved to 4%+ • Structural improvement in fiscus, inflation, real commodity prices • Fixed investment boom will continue • Job growth, real wage increases, emergent consumer will prevent a wipe-out • OMIGSA forecast: Real GDP growth 4.5% in 2008, 5.0% in 2009 10 8 6 4 Real GDP Growth (%) 2 0 -2 High commodity prices Isolation ANC government -4 1970 1973 1979 1982 1985 2003 1961 1964 1967 1976 1988 1991 1994 1997 2000 2006 2009E UT\PressConf_0108_RSpeter

fear vs valuation UT\PressConf_0108_RSpeter

Bogeymen • Stagflation: • We believe core inflation is well contained globally • Central bank policy error • The Fed has already made a mistake. Will it be exacerbated by the ECB? This is a risk in SA as well • China recession (if you call 8% growth a recession) • Will emerging markets manage to decouple? Does China slump after the Olympics with disastrous effects on commodities? • Rand weakness UT\PressConf_0108_RSpeter

Rand weakness • Does the uncertainty about politics cause foreign investors to panic out of SA? • We don’t think so but the current account deficit is a fundamental flaw • While it exists we think it is prudent to have international diversification in a portfolio • In the short-term the rate differential is keeping the rand artificially strong UT\PressConf_0108_RSpeter

Fear has moved into prices3mth performance to 20 Jan 2008, own currency Very little de-coupling here! UT\PressConf_0108_RSpeter

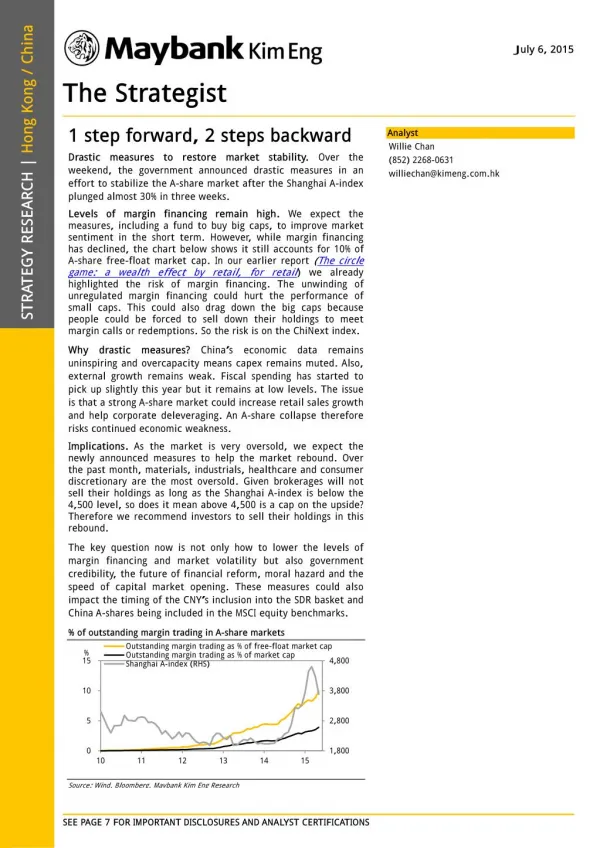

Global valuationsGlobal 12 month forward P/E • Markets have already pre-empted much of the bad news and valuations have fallen to attractive levels • Forward price:earning ratios are: World 11.7x, US 12.6x, UK 10.9x,Europe 10.3x • This provides a buffer for downward earnings revisions which we expect The global stock market P/E ratio is just 11.7x - 8% below the previous trough of 12.5x reached in Sep ‘90 Source: Lehman Brothers Equity Strategy, FTSE, IBES, Exshare UT\PressConf_0108_RSpeter

Global valuations • Valuations are particularly attractive relative to bond yields, and increasingly against cash • Earnings yields less real bond yields are high providing a margin of safety • Corporates recognise this opportunity and continue to buy back shares UT\PressConf_0108_RSpeter

Equity return drivers Price Earnings Ratio All Share Total Ret. Earning Per Share Forward Div. Yield All Share Index Dec 2006 24915 2573 3.0% 1440 17.3x Dec 2007 28958 3067 3.2% 1994 14.5x Ann. Change 16.2% 19.2% +38% -16% UT\PressConf_0108_RSpeter

Valuations: SA • The market has de-rated and now trades on a forward PER of 11.5x. Half* the stocks are on fwd PER’s of 10x or less • 1/3rd of our universe of stocks have a dividend yield of 5% or better • 20 companies have forward yields greater than the after-tax return on cash 25 20 15 SA Forward PER (x) 10 5 0 Jan-60 Jan-63 Jan-66 Jan-69 Jan-72 Jan-75 Jan-78 Jan-81 Jan-84 Jan-87 Jan-90 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 * Numbers based on OMIGSA’s universe of 150 stocks UT\PressConf_0108_RSpeter

All Share Corrections greater than 20% Months to Decline Months to Peak Trough Trough Decline (Ann) Recovery 31/05/31 31/07/32 14 -34.8 -30.7 7 31/10/36 30/04/39 30 -22.8 -9.8 25 31/01/48 30/09/53 68 -37.9 -8.1 72 31/01/60 30/04/61 15 -30.3 -25.1 10 30/04/69 31/10/71 30 -58.1 -29.4 20 31/03/74 31/08/76 29 -42.6 -20.5 23 31/10/80 30/06/82 20 -38.8 -25.5 5 31/08/87 29/02/88 6 -42.6 -67.1 13 30/04/98 31/08/98 4 -39.7 -78.1 16 31/05/02 30/04/03 11 -30.5 -32.8 9 31/10/07 31/01/08 3 -18.7 -56.2 0 Source: OMIGSA & Firer, C. and McLeod, H.Analysis based on the ALSI Total Return UT\PressConf_0108_RSpeter

Expected Returns • EQUITIES - OVERWEIGHT • Total returns, over time, of 10% - 13% p.a. • Higher risk (volatility) for this return. • PROPERTY - OVERWEIGHT • Expect ±11% p.a. over time • Limited re-rating potential. Key driver is now growth • BONDS - UNDERWEIGHT • Have adjusted to lower inflation. Low real return potential • Expect ±8% p.a. over time • CASH - OVERWEIGHT • Attractive on a risk adjusted basis in the short-term • Expect ±7% p.a. in the medium-term • OFFSHORE - NEUTRAL • Offshore exposure prudent for risk diversification UT\PressConf_0108_RSpeter

how manyrounds? UT\PressConf_0108_RSpeter

Conclusion • 2008 is a tale of two halves: a tough H1 with bad newsflow and a better H2 as markets look forward to 2009 and the impact of rate hikes • There is a lot to fear and caution is warranted. However, volatility will create opportunity and investors should be looking for this • Valuations are becoming refreshed and the long-term outlook for emerging markets and hence SA remains good • We continue to invest for the long-term in growth assets UT\PressConf_0108_RSpeter

Regulatory Information Old Mutual Investment Group (South Africa) (Pty) Limited Physical Address: Mutualpark, Jan Smuts Drive, Pinelands, 7405 Telephone number: +27 21 509 5022 Old Mutual Investment Group (South Africa) (Pty) Limited is a licensed financial services provider, FSP 604, approved by the Registrar of Financial Services Providers (www.fsb.co.za) to provide intermediary services and advice in terms of the Financial Advisory and Intermediary Services Act 37 of 2002. Old Mutual Investment Group is a wholly owned subsidiary of Old Mutual (South Africa) Limited. Reg No 1993/003023/07. The investment portfolios may be market-linked or policy based. Investors’ rights and obligations are set out in the relevant contracts. Market fluctuations and changes in rates of exchange or taxation may have an effect on the value, price or income of investments. Since the performance of financial markets fluctuates, an investor may not get back the full amount invested. Past performance is not necessarily a guide to future investment performance. Personal trading by staff is restricted to ensure that there is no conflict of interest. All directors and those staff who are likely to have access to price sensitive and unpublished information in relation to the Old Mutual Group are further restricted in their dealings in Old Mutual shares. All employees of Old Mutual Investment Group are remunerated with salaries and standard short-term and long-term incentives. No commission or incentives are paid by Old Mutual Investment Group to any persons. All inter-group transactions are done on an arms lengths basis. In respect of pooled, life wrapped products, the underlying assets are owned by Old Mutual Life Assurance Company (South Africa) Limited who may elect to exercise any votes on these underlying assets independently of Old Mutual Investment Group. In respect of these products, no fees or charges will be deducted if the policy is terminated within the first 30 days. Returns on these products depend on the performance of the underlying assets. Old Mutual Investment Group has comprehensive crime and professional indemnity insurance. For more detail, as well as for information on how to contact us and on how to access information please visit www.omigsa.com. UT\PressConf_0108_RSpeter