Download

1 / 47

470 likes | 611 Views

Credit Default Swap with Nonlinear Dependence. Chih-Yung Lin Shwu-Jane Shieh 2006.12.14. Abstract.

E N D

Credit Default Swap with Nonlinear Dependence Chih-Yung Lin Shwu-Jane Shieh 2006.12.14

Abstract • The first-to-default Credit Default Swap (CDS) with three assets is priced when the default barrier is changing over time, which is contrast to the assumption in most of the structural-form models. • We calibrate the nonlinear dependence structure of the joint survival function of these assets by applying the elliptical and the Archimedean copula functions.

Abstract • The empirical evidences support that the Archimedean copula functions are the best-fitting model to describe the nonlinear asymmetric dependence among the assets. • We investigate the effects and sensitivities of parameters to the survival probability and the par spread of CDS with three correlated assets by a simulation analysis.

Abstract • The simulation analysis demonstrates that the joint survival probability increases as these assets are highly positive correlated.

Outline • 1. Introduction • 2. Methodology • 3. Empirical and Simulation Results • 4. Conclusions

1. Introduction • A. Two Core Issues • B. First-to-Default Credit Default Swap (CDS) • C. Elliptical Copulas and Archimedean Copulas • D. Related Literatures

Twocore issues • a. structural-form model : • how to use credit default model in the pricing of first-to-default CDS in the structural-form model . • b. copula function : • how to use copula function in the pricing of first-to-default CDS consisting of three assets.

Structural-form model : • This part is the extension of “the model of Finkelstein, Lardy, Pan, Ta, and Tierney (2002)”. • That discusses the pricing of one firm’s CDS in the structural-form model. • In this paper, we discuss with the pricing of CDS in two companies, three companies and n companies.

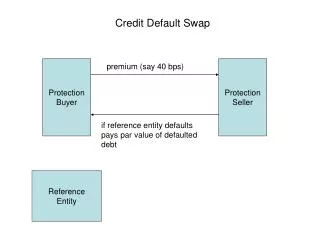

First-to-Default Credit Default Swap • the buyer : • may experience a credit default event in the portfolio of assets which may cause their loss uncertainly. • the seller: • receive the payments that the buyers pay every season or every year before the credit incident happened. • When the first credit incident happened, the sellers have to pay the loss to the buyer.

Elliptical Copulas and Archimedean Copulas • Elliptical Copulas a. Gaussian copulas b. t copulas • Archimedean Copulas a. Clayton copulas b. Frank copulas c. Gumble copulas

Related Literatures • Credit default swap (CDS) • Finkelstein, Lardy, Pan, Ta, and Tierney (2002) apply the credit risk model of KMV to calculate the prices of CDS. • This is the first paper that finds out the closed form result of the pricing of CDS in literature. • The default barrier in their model is variable, but the default barrier of KMV is regular.

Related Literatures • Li (2000) has a main contribution in discussing with how to use copula function in the default correlation and first-to-default CDS valuation. • Junk, Szimayer, and Wagner (2006) where they calibrate the nonlinear dependence in term structure by applying a class of copula functions and show that one of the Archimedean copula function is the best-fitting model.

2. Methodology • A. Valuing Credit Default Swap with single firm • B. Definition, basic properties about Copula • C. Solving survival function with copula function

Valuing Credit Default Swap with single firm • a. Firm’s assets : • We assume that the asset's value is a stochastic process V and V is evolving as a Geometric Brownian Motion (GBM). ……….. (1) • where W is a standard Brownian motion, σ is the asset's standard deviation, and μ is the asset value average. We also assume that 0=μ.

Valuing Credit Default Swap with single firm • b. Recovery rate : • We assume that the recovery rate L follows a lognormal distribution with mean and percentage standard deviation λ as follows: …….…….. (2) …….…….. (3) …….…….. (4)

Valuing Credit Default Swap with single firm • Where L is the global average recovery on the debt and D is the firm’s debt-per-share. • The random variable Z is independent of the Brownian motion W, and Z is a standard normal random variable.

Valuing Credit Default Swap with single firm • c. Stopping time • The survival probability of company at time t can be defined as the probability of the asset value (1) does not reach the default barrier (4) at time t. ……….. (5)

Valuing Credit Default Swap with single firm • We can do some conversions in the formula (5). First, we introduce a process Xt in the formula (6); then we convert formula (5) to formula (7). ……….. (6) ……….. (7)

Valuing Credit Default Swap with single firm • d. Survival function • Now we want to find the first hitting time of Brownian motion in the formula (7). For the process Yt = at + bWt with constant a and b, we have (see, for example, Musiela and Rutkowski (1998)) ……….. (8)

Valuing Credit Default Swap with single firm • Apply to Xtwe can obtain a closed form formula for the survival probability up to time t. ……….. (9) Where

Valuing Credit Default Swap with single firm • e. The pricing of Credit Default Swap • do some transfer in the calculating of the asset standard deviation …….. (10) Where

Gaussian copulafunction • when n=k, we can get the Gaussian copula function as follows:

Gaussian copula function • when n=3, we can calculate the joint survival function of three companies as follows: ……… (17) +

t-copula function: • Y is the random variance of distribution ……… (18) Where

t-copula function: • when n=k, we can get t-copula function as follows:

t-copula function • when n=3 : … (20)

Clayton copulafunction • when n=3 :

Frank copula function • when n=3 :

Gumbel Copula function • when n=3 :

3. Empirical and Simulation Results • A. Data • B. Empirical Results • C. Simulation Results

Empirical Results • Moreover we can find there is steady positive correlation between T and c*. The empirical results support that the dependence among these assets are asymmetric and can be better described by the Archimedean copula functions. • The results obtained here are consistent with those documented by Junker, Szimayer, and Wagner (2006) where they calibrate the nonlinear dependence in term structure by applying a class of copula functions and show that one of the Archimedean copula function is the best-fitting model.

Simulation Results • In this part, we want to find the relationship between model parameters and the survival probability (S). On the other hand, we also discuss with the relationship between model parameters and the par spread (c*). • So we use AT&T Inc. and Microsoft Corp. to be our reference companies. Then we use the basic stock price on 2006/3/08 to estimate the par spread of CDS in T=480.

The effect of the correlation (ρ) • In our intuition, the lower correlation leads to the higher survival probability(S). But we find some interesting evidences in the simulation results. We can find that the survival probability is always the highest when the correlation is 0.9. But we can not get a steady result in the comparing between ρ=0.001 and ρ=-0.9. • Thus we can find that the difference of the survival probability between ρ=0.001 and ρ=-0.9 is always very small. In addition, we can find that the positive correlation among assets has a positive effect to the survival probability.

4. Concluding Remarks • We derive the pricing of Credit Default Swap (CDS) in three companies under the situation where the default barrier is variable, the survival probability is lognormal distributed and the default-free interest rate is constant. • The joint survival probability of three companies is derived by employing the Elliptical and Archimedean copula functions and we can price the CDS with three assets. • In addition, we also investigate how the model parameters affect the survival probability of the three companies by a simulation analysis.