Credit Default Swaps

Credit Default Swaps. Can someone explain to Brian Williams what a CDS is? An insurance policy taken out by a buyer of a bond against the risk of default by a bond seller. The ticking bomb in the financial markets. Essentially How it Works.

Credit Default Swaps

E N D

Presentation Transcript

Credit Default Swaps • Can someone explain to Brian Williams what a CDS is? • An insurance policy taken out by a buyer of a bond against the risk of default by a bond seller. • The ticking bomb in the financial markets

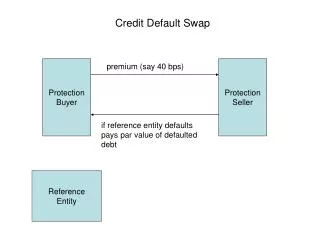

Essentially How it Works Risky Business (RB) borrows $10,000,000 from Rock of Gilbraltar (RoG). (RB Sells RoG a $10,000,000 bond.)

The Insurance Policy Snidely Whiplash (SW) sells RoG an insurance policy against the risk that RB will default on the loan (bond)

It’s Simple, Really… http://en.wikipedia.org/wiki/Credit_default_swap Sellers of CDS contracts will give a par quote for a given reference entity, seniority, maturity and restructuring e.g. a seller of CDS contracts may quote the premium on a 5 year CDS contract on Ford Motor Company senior debt with modified restructuring as 100 basis points. The par premium is calculated so that the contract has zero present value on the effective date. This is because the expected value of protection payments is exactly equal and opposite to the expected value of the fee payments. The most important factor affecting the cost of protection provided by a CDS is the credit quality (often proxied by the credit rating of the reference obligation. Lower credit ratings imply a greater risk that the reference entity will default on its payments and therefore the cost of protection will be higher.

So (for Example), Here’s the Deal • One year term. • Par Premium is c% (e.g., .02 or 2%) • Notional value is N (e.g., $10,000,000) • Premiums paid quarterly at times t1, t2, t3, t4. Default, if it occurs, happens at one of these times. • Quarterly premium payment = Nc/4 paid at the end of the quarter. (Nc/4=$50,000) • Recovery rate is R (e.g., .50 or 50%). If RB defaults, SW pays RoG N(1-R)

What’s Needed for SW and RoG to Agree on a Deal • Probabilities of no default looking ahead from time 0 are P1, P2, P3, P4. These depend on the credit rating of RB. • Discount rates for computing present discounted values of cash flows to be received 1, 2, 3, and 4 periods in the future, δ1, δ2, δ3, δ4.

5 Ways The Contract Ends Time t0 Time t1 Time t2 Time t3 Time t4

Joint Probabilities – The Contract Ends with Default at Time T2 Prob(Default at T1) =P(D1) Prob(Not Default at T1) =P(ND1) Prob(Default at T2|ND1) =P(D2|ND1) Prob(Not Default at T2|ND1) =P(ND1) P(Default at T2 and Not Default at T1) = P(D2|ND1)P(ND1) = P1(1-P2)

Present Values of Cash Flows Sum = Expected PDV of Sum to obtain Expected PresentPremium Payments Discounted Value of Default Payment

Setting the Price N, The probabilities p1, p2, p3, p4,The discount rates, δ1, δ2, δ3, δ4The recovery rate, R All known. Set PV = 0. The only unknown is c, which is the price.

So What’s the Big Deal? • Snidely Whiplash is an insurance company • He need not have any reserves to insure that he can actually pay off if the borrower really does default • There is no regulation over the forms of these agreements. • There is no regulation and no agreement on what constitutes a “credit event.” • So what? These are grownup willing buyers and sellers who know what they are doing.

Why Do “We” Care? • There are about $60 trillion in existing CDS contracts, up from less than $30T last year, up from about $13T in December 2005. Quadrupled in two years. • The pool of CDSs exploded as the underlying mortgage backed securities began to look unpleasant (toxic). • The pool of underlying bonds grew far far less. • The underlying bonds that are the subject of these “bets” add up to about $6 trillion. • Thus, essentially, $54T are side bets • Noone really believed (until last week) that all (or even some) of these bonds would fail at once

How Does This Relate to This Course? • The PDV is an expected value • The price setting mechanism is a fair game – set the expected PDV to zero. This looks exactly like our warranty calculation. • The default probabilities are conditioned on borrower specific information (just like Fair Isaac) • The probabilities are based on a probability model that is essentially the same as our light bulb model. • The paths to termination of the CDS look like our analysis of litigation risk in using conditional and marginal probabilities.