Download

1 / 15

170 likes | 428 Views

Introduction of Credit Default Swaps. R N Kar Reserve Bank of India. Brief Background. Announcement in the 2 nd Quarter Review of Monetary Policy of 2009-10 Objective- Provide credit risk management tool, and increase investor’s interest in corporate bond Constitution of Internal Group

E N D

Introduction of Credit Default Swaps R N Kar Reserve Bank of India

Brief Background • Announcement in the 2nd Quarter Review of Monetary Policy of 2009-10 • Objective- • Provide credit risk management tool, and • increase investor’s interest in corporate bond • Constitution of Internal Group • Draft Report • Put in public domain on August 4, 2010

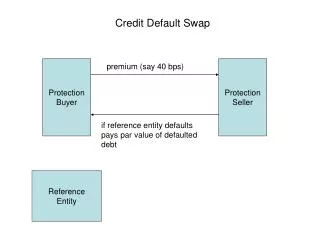

Product Design • Plain vanilla CDS • Only on Corporate Bonds • Issued by single legal resident entities • Rated issuers (no minimum prescribed) • Unrated SPVs of rated Infra Cos permitted • Original maturity exceeding 1 year

Eligible Participants • Bifurcation into Market Makers & Users • Market Makers: (both buy and sell) • Commercial Banks • NBFCs having financial strength and involved in providing credit facilities- case to case basis • Insurance companies and MFs, subject to regulatory approval • Users: [only to buy(hedge)] • Commercial Banks • NBFCs • Primary Dealers • MFs • Insurance Cos • HFC,PFs • Listed Corporates

Proposal to restrict naked CDS by users • Users • The users can buy CDS for amounts not higher than the face value of credit risk held by them and for periods not longer than the tenor of credit risk held by them • Can only unwind the protection with the original counterparty • Mandating physical delivery for users and restricting the users from selling CDS

Standardisation • Standardisation • Settlement dates • 20th March, June, Sept, December • Coupons (spreads) • Coupons (spreads) to be decided by market (FIMMDA)

Credit Events • Credit Events • Standard ISDA credit events • bankruptcy, • failure to pay, • repudiation/moratorium and • obligation acceleration • Restructuring excluded in the early stages • Master agreement to cover the details

Settlement Methodologies • For users, physical settlement is mandatory. • Market-makers can opt for any of the three settlement methods • Physical settlement, • Cash settlement , • Auction based settlement

Market Coordination • Important for CDS • FIMMDA to coordinate with ISDA • Determination Committee (Indian) • Adequate participation from all stake holders • At least 25% of the members may be drawn from the users • Conduct of Auctions • Dissemination of daily credit curves for valuation

Risk Management • Protection sellers • Protection sold within overall exposure limits • Position limits for seller • Reference entity wise and Gross • Risk Limits • Board to fix a limit on their Net Long risk position in terms of Risky PV01, linked to a percentage of the Total Capital Funds of the entity • PV01 within 0.25 per cent of net worth (for all OTC non-option rupee derivatives) • Protection buyer- Board approval, periodic assessment and legal advise

Reporting Arrangements • Centralised Repository for CDS trades • Electronic Reporting Platform • Market Makers to report within 30 minutes • Information to be made available to • Regulators • Market dissemination • Additional Regulatory reporting of • Risk limits • Adherence to controls • Audit findings etc

Collateralisation issues • Protection sellers need to maintain margins with buyers • Bilateral arrangements difficult (valuation, discipline) • Third Party arrangements preferred • Non-Guaranteed settlement through a clearing house would resolve the problem • Eventual migration to guaranteed settlement -CCP • More entities can be permitted on both sides

CCP arrangements • A CCP to be identified to commence the process of building systems • Co. registered under Payment and Settlement Act, 2007 • CCP risks incase of CDS are unique due to Jump-to-default risk • Need for • Defined Legal Status • Liquidity arrangement • Robust risk management system