Download

1 / 15

150 likes | 539 Views

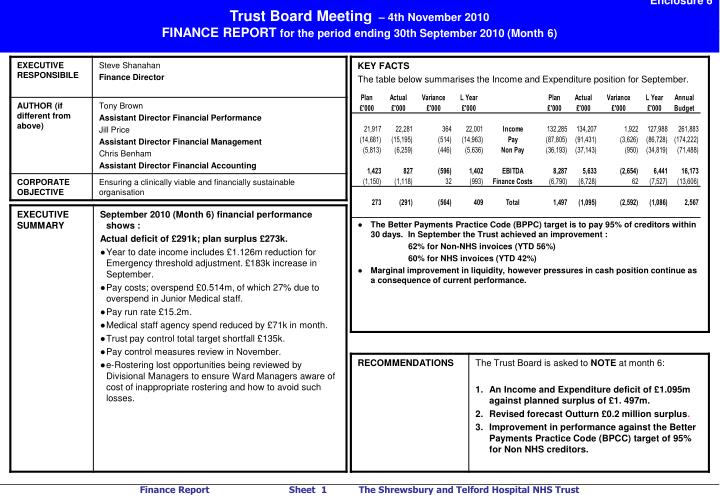

Enclosure 6 Trust Board Meeting – 4th November 2010 FINANCE REPORT for the period ending 30th September 2010 (Month 6). Section One- EXECUTIVE SUMMARY. Section Two – Expenditure - Pay. PAY

E N D

Enclosure 6 Trust Board Meeting – 4th November 2010 FINANCE REPORT for the period ending 30th September 2010 (Month 6)

Section Two – Expenditure - Pay PAY • Month 6 Pay overspend £514k, across all staff groups. Efficiencies required to cover the pay award continue to be the main cost pressure. • Pay cost in Month 6 was £15.2m, the average for months 1 to 5 was £15.3m • Pay control totals were allocated to divisions during August . The June pay spend of £15.4m was taken as a base against which to allocate run rate reductions of £350k per month. In month 6 the pay cost exceeded the control total by £135k. The month 6 run rate is a reduction in pay cost of £215k against the June level. • Key initiatives to reduce the level of nursing spend are being implemented, these include reducing bank shift duration, changing working patterns and contracting for hours to be worked over a given period rather than fixed weekly hours. Divisional lead nurses have led these reviews to ensure quality and service levels are maintained. • Review of the progress in implementation of initiatives and the effectiveness of those already in place along with an assessment of further initiatives to control the pay run rate will take place in November. AGENCY • Month 6 agency costs increased to £576k (August £571k). This is equivalent to 55 wte. • September agency spend per wte is £10.4k. (Month 5 £10.2k.) • Consultant agency utilisation shows an increase in the month. This is largely in Radiology(linked to reducing external reporting costs), Oncology and Ophthalmology covering sickness and vacancies. • Medical staffing agency spend shows a further reduction in September. • Use of nursing agencies has risen in the month. The key driver for this has been the need to open escalation beds. • Further reductions are reported in Other Clinical and Non-clinical groups. In Facilities the reduction is partly due to improvements in sickness levels.

Section Two – Expenditure – Pay – Medical Staffing • Medical Staff overspend £141k (August £323k). Agency overspend within this is £150k which as reported previously is due to the premium cost of providing cover to ensure continuity and safety of service and compliance with EWTD requirements. Where safe and possible, Divisions only provide agency cover for out of hours and weekend periods. • Temporary staffing department reports that in September 453 shifts were filled. Of these 43 (9.5%) were internally covered, the balance of 410 (90.5%) were filled by agency. For 2009/10 the average was 652 shifts with the agency cover averaging 511. • Medical staff agency cover costs have decreased in September to £377k (£448k in August). • The graphs opposite show the trend in medical staffing expenditure over the 12 months. The graph shows that the cost of directly employed and locum have remained even. However, from September 2009 the reliance on agency to cover Deanery vacancies and EWTD rota gaps increased. In October 2009 agency was 29.5% of the total medical staffing spend, in September 2010 this is 18.3% reflecting the improved fill rate for rotational posts. • The impact of the improved fill rate in the August rotation is now fully reflected in the run rate, the September cost of Medical Staffing is the lowest in the year to date. • Managers are currently assessing the potential impact and risk linked to agency reliance following the October rotation.

Section Three - Cash • Closing cash balance of £316k is a decrease of £1,622k on the prior month. • EBITDA shortfalls (YTD £2,589k) and the requirement to make capital expenditure payments have been managed through creditor payments within working capital. This management of working capital is reflected within the poor compliance status of the Better Payment Practice Code (BPPC). • The Trust follows the national timetable of activity reconciliation and as a result is carrying significant levels of accrued revenue. Until agreement has been reached the Trust cannot invoice this significant amount of accrued revenue. • The Trust has concluded it’s review of the historical working capital loan drawdown. Papers have been submitted to Finance and Performance Committee Meeting and Trust Board. Further to recent SHA and Chief Executive meetings the Trust will be completing an application for a working capital loan. • The Trust will escalate the prior year Shropshire County PCT debtor to the SHA to assist in accelerating payment. • Revised forecasting procedures are in place with significant cash outflows in the first quarter 2010/11 due to the completion and timing of large capital projects (including decontamination offsite solution).

Section Three – Cash Forecast • Forecast closing cash balance in line with Plan and EFL of £200k. • Forecast EBITDA shortfall of £2,383k will be managed through creditor payments within working capital. • Forecast capital expenditure includes c £2,500k cash outflow relating to prior year Decontamination project and will be managed through creditor payments within working capital. • Total working capital movement adverse variance to plan of £4,677k explained by EBITDA shortfall and prior year capital expenditure. • Planned loans for capital expenditure not progressed. • Forecast PDC of £500k relates to cash backed CRL transfer from T&W PCT. • Forecast does not include any effect of the anticipated working capital loan.

Section Four – Forecast Outturn During September significant work has taken place with Divisions to build detailed forecasts; in addition a detailed review and assessment of activity and income has been undertaken. These two work streams were consolidated and a revised forecast outturn of £0.2m surplus was submitted in the month 6 FIMS return, this followed detailed discussions with the SHA. The forecast includes the following assumptions: • PCT QIPP schemes do not deliver. • Current non-elective activity over performance for Shropshire County PCT continues. • Emergency Threshold adjustment, forecast £2.6m, is not returned. • Pay run rates continue in line with divisional forecasts including full recruitment to previously approved additional posts including consultant and medical staff linked to ensuring patient safety and quality levels. • Escalation beds required during the winter pressure period. • Divisional forecasts incorporate pay run rate reductions and medical agency cost reductions. • CIPs at 66% of target. • Strategic Change Reserve funding receivable £3.5m.

Section Five - Improvement Programme The summary position is as follows: • IP target for 2010/11 is £6.8 million. • At Month 6 £1.258m has been delivered against a target of £1.756m. This equates to 72%. Against the revised forecast of £1.653m delivery equates to 76%. • The current forecast outturn assumption is that delivery will be at 66% (£4.5m)

Section Six - Financial Risk Rating Risk rating of 2. • Deterioration in each of the FRR performance metrics other than liquidity. • Liquidity metric shows rating of 1. Reduced cash balance reflecting payment of PDC dividend. Current asset reduction due to lower levels of cash, NHS debtors and prepayments. Current liabilities improvement due to PDC dividend accrual reduction and payment, and reduced levels of NHS creditors and non-NHS capital creditors. • Performance below plan continues to impact on the liquidity position • The diagram above illustrates the Trust position in each metric of the FRR against the full year plan position and illustrates the in-month deterioration against each of the metrics, other than liquidity.

Section Seven- Activity and Income In Patient Performance • Total elective and day case activity was 311 spells above plan in September. This has given rise to an income over-recovery of £59k. • Day Cases show an over performance of 323 spells in September. Key areas of over performance are Gastroenterology, Ophthalmology, Clinical Haematology, Gynaecology, Nephrology and Clinical Oncology. • Elective inpatient activity was 12 below plan in September. • Non elective activity is 131 spells above plan in September notably in General Medicine. Income has been adjusted to reflect the emergency threshold tariff adjustment, this has reduced reported income by £1,126k. Non elective activity in total including maternity is £229k above plan in September. • Maternity activity is below plan 11 spells in September. Out Patient Performance • In September outpatients were 3,180 attendances above plan, the income over recovery for the six months is £1,928k, (September £470k). • In September new outpatients are 2,226 attendances above plan. This includes Outpatient Procedures overperformance in the month of 1,005. The underlying new outpatient activity is 1,226 above plan. Areas of underperformance include Orthopaedics, Orthodontics, Dermatology and Geriatric Medicine. • Outpatient procedure activity is above plan in Breast Surgery, Colorectal Surgery, Orthodontics, Dermatology, Obstetrics and Gynaecology. This offsets new outpatient underperformance. • Follow up outpatients are 954 attendances above plan and 2,347 attendances above the August level. Accident and Emergency • A & E attendances are 206 above plan in September (1,088 YTD). In month activity analysis shows RSH 51% and PRH 49%,

Section Eight - Expenditure – Non-Pay and Finance Costs • Non pay shows an overspend of £446k in month. All non-clinical non-pay expenditure requisitions continue to be reviewed and scrutinised for validity and necessity before being approved. • Divisional Reports highlights specific areas of non pay over spend including: • Cancer/ Oncology/ Haematology drugs offset, by income recovery • Theatres Orthopaedic products, hip, knee and trauma related. Division 3 are undertaking a baseline review to identify expenditure linked to backlog work. • Patient Transport Costs, offset by income. • Compensation Recovery Unit write offs in excess of accrued amounts. • Transfer back to revenue of previously capitalised costs associated with schemes unlikely to proceed. • Finance costs are £32k underspent in September. Forecast outturn is in line with plan.

Section Nine - Debtors • Trade debtors have decreased by £722k compared to prior month with an increase in accrued revenue of £250k. Total debtors have therefore decreased by £478k when including the £6k increase in bad debt provision. • Shropshire County PCT prior year invoices remain unpaid with no movement within the month. As part of the recent Month 6 financial returns submission the PCT disputed these invoices via the agreement of balance process. Discussions with the SHA will begin to attempt to accelerate the payment of balances that were agreed as part of the year end financial returns process 2009/10. There have been small reductions in the +60 and +30 days categories. • Telford and Wrekin PCT prior year invoices show a reduction of £231k with the remaining balance represented by high cost drugs. There have been small increases in the +60 and +30 days categories. • Herefordshire prior year has been paid on 15 October 2010. • Of the other debtors outstanding £33k has been referred to a specialist collection agency with appropriate provisions for write off made based on expected collection success. • £56k in respect of an overseas visitor with no means to pay is shown in line with DH guidance – this debtor has been provided for in full. • The credit balance of £113k for West Midlands Specialised Services is the net result of a September raised credit note for £227k.

Section Ten – Creditors (Non NHS) • Table 1 summarises the non-NHS creditor payment performance for the cumulative prior year, month 6 and year to date position. The graph shows the prior year by month with current month position. • The Better Payment Practice Code stipulates a target of 30 days. • Increase in monthly compliance position due to prioritisation of non-NHS payments. The current cumulative compliance is on par with month 5 and is 32% for volume and 56% for value. • Table 2 summarises the actual payment performance in the month.

Section Ten – Creditors (NHS) • Table 1 summarises the non-NHS creditor payment performance for the cumulative prior year, month 6 and year to date position. The graph shows the prior year by month with current month position. • The Better Payment Practice Code stipulates a target of 30 days. • The cumulative compliance position at Month 6 shows a small improvement against the prior month at 25% for volume and 42% for value. • Table 2 summarises the actual payment performance in the month.

Section Eleven - Capital • The Capital Programme for 2010/11 has been revised to £8,505k. This is based on internally generated funds with additional CRL transfers of £300k and £500k agreed by the SHA at Month 06 for Maternity Refurbishment and Patient Status at a Glance (PSAG), respectively. • £154k of capital funds remains available. • CT Scanner PRH – temporary CT Scanner currently in use. The building works are nearly completed with delivery of CT Scanner is scheduled for early October. Planned date for new CT Scanner to be operational remains at 25 October 2010. • Decontamination Project – handover of the facility is planned for early November 2010 following a delay in the utility upgrades. It is expected that the unit will become operational in February 2011. PRH service move is planned for February 2011 with RSH service move planned for Mid-Spring 2011. • Theatres Air Handling Scheme – Theatre 1 now operational, Theatre 2 to be formally handed over early October. • Breast Screening Service move to Digital - a phased approach over a three year timeframe has been approved to move from analogue to digital equipment. Due to securing RSH League of Friends funding for the equipment in the Static Assessment Unit at RSH the Trust has been able to accelerate the Project by bringing forward the purchase of a mobile digital unit at a heavily discounted price. Phase 1 now consists of equipment and enabling works in a Static Assessment Unit at RSH; Stage 1 of necessary software/links to PACS; and purchase of ex-demo mobile unit fully equipped with digital equipment.