Download

1 / 31

310 likes | 446 Views

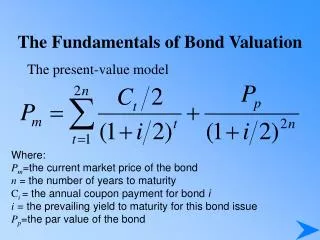

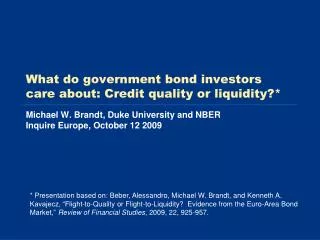

What do government bond investors care about: Credit quality or liquidity?* . Michael W. Brandt, Duke University and NBER Inquire Europe, October 12 2009.

E N D

What do government bond investors care about: Credit quality or liquidity?* Michael W. Brandt, Duke University and NBERInquire Europe, October 12 2009 * Presentation based on: Beber, Alessandro, Michael W. Brandt, and Kenneth A. Kavajecz, “Flight-to-Quality or Flight-to-Liquidity? Evidence from the Euro-Area Bond Market,” Review of Financial Studies, 2009, 22, 925-957.

Motivation Flight-to-quality or flight-to-credit? • Flight-to-quality • Portfolio rebalancing from fixed income securities that are more credit risky to ones that are less credit risky • In equilibrium results in yield differentials between securities with different credit quality • Flight-to-liquidity • Portfolio rebalancing from fixed income securities that are more liquid to ones that are less liquid • In equilibrium results in yield differentials between securities with different liquidity • Both types of flights tend to be associated with “market stress” • Major events or economic news releases • Unusually low market-level liquidity • Unusually high market-level volatility

Motivation Research question • Which security characteristic, credit quality or liquidity, do fixed income investors care about more • Unconditionally • Conditionally during periods of market stress • Differentiate between • Valuation effect • How are yield spreads explained by credit quality and liquidity in the time-series and cross-section? • Trading behavior • How are large flows into (and out of) the bond market related to credit quality and liquidity in the cross-section?

Motivation Empirical challenge • Difficult to disentangle credit quality and liquidity because the two are generally positively related in the cross-section • Example: • U.S. Treasuries are both more liquid and less credit risky compared to U.S. corporate bonds • If we see investors sell corporate bonds to buy Treasury bonds, is this a flight-to-quality or a flight-to-liquidity? • Difficult to measure credit-quality of fixed income securities • Top-down, bottom-up, and reduced form credit risk models • Difficult to measure liquidity of fixed income securities • Until recently over-the-counter market • Now multiple electronic trading platforms

Motivation Evidence from the Euro-area bond market • Euro-area sovereign bond market • Credit quality and liquidity are inversely related • Empirically and theoretically • Intuition • Credit quality of sovereign debt increases with a country’s fiscal discipline (i.e., lower deficit/GDP ratio) • Liquidity of sovereign debt depends on the quantity of outstanding debt and thus decreases with a country fiscal discipline • Allows us to disentangle flights to quality and liquidity • Liquid sovereign credit default swap (CDS) market • Market-implied credit risk • Electronic market • Single dominant trading platform (MTS, >70% of turnover) • Allows us to precisely measure liquidity

Motivation Outline • Data • Variable construction and preliminaries • Results • Valuation (yield spreads) • Unconditional • Conditional • Trading behavior (order flow) • Linking valuation and trading behavior • Conclusion

Data Bond market data • MTS trading platform • Intraday European bond market data for over 750 individual fixed income securities, approximately 88% of which are issued by governments, and a market share greater than 70% of daily average turnover in 2003 • Security identification information • Issuing country, maturity, coupon, etc. • Trade information • Date and time, buy/sell indicator, trade price, and size • Quote information • Prices and depths at the three best bid and offer prices on each side of the limit order book • 10 European Union countries • Austria, Belgium, Finland, France, Germany, Greece, Italy, The Netherlands, Portugal, and Spain • April 2003 through December 2004

Data Credit default swap (CDS) data • Credit default swap data from Lombard Risk, an independent valuation service currently owned by Fitch Rating Inc. • Daily survey of key credit default swap (CDS) market makers for the 3, 5, 7 and 10yr maturities for each country • Data includes date, country, currency, maturity and the mean and standard deviation of the CDS spread in basis points • CDS contract with restructuring clause • Softest credit event triggering the payoff of the CDS is restructuring • ISDA defines restructuring to include events that lead to a reduction in interest payments, a reduction in principal repayments, a postponement or deferral of interest or principal payments, or any change in the currency or composition of any payment of interest or principal

Variable construction and preliminaries Variables • Separate bonds by country, remaining time-to-maturity (3, 5, 7, 10yr), and benchmark (e.g., on-the-run) status • Sovereign yield spreads • Fit Nelson and Siegel (1987) zero-coupon yield curve to coupon bond prices for each country quoted in the last two hours of trading • Transform zero-coupon yield curve into a par-bond yield curve • Use Euro-swap curve as benchmark yield spreads = yield for given country/maturity – Euro-swap yield • Credit variables • CDS spread • Liquidity variables • Effective bid-ask spread • Average quoted depth • Average cumulative limit order book depth • Liquidity index = (avg. quoted depth / avg. percent quoted spread)

Variable construction and preliminaries Summary statistics • Considerable variation in credit default swap spreads as well as liquidity across countries

Variable construction and preliminaries Correlation between credit quality and liquidity

Variable construction and preliminaries Correlation between credit quality and liquidity

Variable construction and preliminaries Correlation between credit quality and liquidity • Another dimension of variation is across maturities • Strong negative correlation between credit quality and liquidity • Lower credit quality is associated with higher liquidity (narrower effective spread and/or larger depths)

Results Unconditional valuation results • Yield spread regression

Results Unconditional valuation results (cont) • Coefficients on credit and liquidity have anticipated signs • Credit (+): higher credit risk → higher yield spread • Liquidity (effsp -, depth +): lower liquidity → higher yield spread • Coefficients are significant at the 1% level and R2 of 22 to 57% • Economic significance • 100 bps increase in the CDS spread differential increases the yield spread by 62 to 96 bps • 10 cents increase in the effective bid-ask spread differential increases the yield spreads by 23 (3-yr) to 2 (10-yr) bps • 100 million Euro increase in quoted depth differential decreases the yield spread by 11 (3-yr) to 1 (10-yr) bps

Results Unconditional valuation results (cont) • Decompose yield spreads into credit and liquidity components • Grand average proportions • 89% credit quality and only 11% liquidity • Large Degree of Heterogeneity across countries and maturities

Results Unconditional valuation results (cont) • E.g., 10yr maturity for the liquidity index

Results Unconditional valuation results (cont) • E.g., 10yr maturity for the liquidity index

Results Conditional valuation results • Condition regressions on periods of market stress • Low liquidity • Below median bond market liquidity index • High equity market volatility • Above median VSTOXX implied volatility index • High interest rate volatility • Above median swaption implied volatility • Sign and significance of the coefficients in the conditional regressions are the same as for the unconditional regressions • Conditional R2 slightly lower for the 3-yr maturity and slightly higher for the 5, 7 and 10-yr maturities • Conditioning on VSTOXX helps explain the short-end • Conditioning on interest rate volatility helps explain the long-end

Results Conditional valuation results (cont) • E.g., 10yr maturity • Conditional vs unconditional coefficients • Credit coefficients substantially smaller for all maturities except 10-yr • Liquidity coefficients larger and dramatically so for the 7 and 10-yr

Results Conditional vs unconditional valuation results E.g., 10yr maturity • Liquidity plays a much greater role in times of market stress • 1/3, 2/3, 3/4 and all of countries register an increase in the role of liquidity for the 3, 5, 7 and 10-yr maturities, respectively

Results Conditional vs unconditional valuation results E.g., 10yr maturity Unconditional Conditional

Results Trading behavior • Identifying flights • Look at aggregate bond market orderflow instead of specific dates • Flight into the market = daily or weekly net order flow > 75%ile • “Flight” out of the market = daily or weekly net order flow < 25%ile • Country level bond market net order flow sum all buyer initiated trades – sum all seller initiated trades • Empirical observations • Flights are associated geopolitical events and economic news • Flights do not seem to target a particular maturity range • Regression specification

Results Trading behavior (cont) • E.g., 10yr maturity flights into the bond market • Flights into the bond market are short-lived flights-to-liquidity • Liquidity always has a positive sign • When credit is significant, it has the sign of a flee-from-quality • Weekly net order flow is not related to credit or liquidity

Results Trading behavior (cont) • E.g., 10yr maturity flights out of the bond market • Flights out of to the bond market are longer-lived • Money flows out of liquid and lower credit quality securities • Weekly net order flow is considerably more predictable

Results Linking valuation and trading behavior • Yield spread decomposition conditional on large net order flow • E.g., 10yr maturity • Comparison to the unconditional results • Same signs for credit and liquidity • Coefficients on credit are basically unchanged • Coefficients on liquidity are 2-3 times their unconditional magnitude • Slightly higher R2

Conclusion Conclusion • Unconditionally and on average, credit risk accounts for 89 and liquidity accounts for 11% of EU sovereign yield spreads, but there are large differences across countries and maturities • Importance of liquidity on sovereign yield spreads increases dramatically (up to two-fold) during periods of market uncertainty • Large flows into the aggregate bond market are directed toward more liquid bonds, not less credit risky bonds, which suggests a flight-to-liquidity • Large flows into the bond market are more urgent than large flows out of the bond market • During flight episodes, liquidity explains an even greater proportion of EU sovereign yield spreads (up to three-fold)