Technology & Strategy

440 likes | 592 Views

Technology & Strategy. GEST-D-484 Manuel Hensmans. First things first…. Register by 16 February Fill out your name , year of study and student id on sheet in class In capitals , please !. All info on…. http ://technologystrategy.skynetblogs.be /

Technology & Strategy

E N D

Presentation Transcript

Technology & Strategy GEST-D-484 Manuel Hensmans

First things first… • Register by 16 February • Fillout yourname, year of study and student id on sheet in class • In capitals, please!

All info on… • http://technologystrategy.skynetblogs.be/ • Slides, readings, syllabus description, guide to grading, overview course…

Some general references • Non-compulsoryreferencetextbooks • Strategic Management Of Technological Innovation (3rd Edition) • Author: Melissa Schelling • Exploring Corporate Strategy (8th or 9th edition) • Authors: Johnson, Scholes & Whittington

Overview Course • Part I: Introduction • Class 1: Overview • Class 2: Introductory strategic concepts

Overview Course • Part II: Industry dynamics techn innov How and why innovation occurs in an industry Why some innovations rise to dominate others • Class 3: Strategic sources of innovation • Class 4: Technological (R)evolution • Class 5: Standard Wars • Class 6: Strategic timing of innovation • Class 7: Class presentations

Overview Course • Part III: Firm-level strategy How to formulate techn innovation strategy How to organize techn innovation strategy • Class 8: Strategic direction • Class 9: Ecosystem strategy • Class 10: E-business strategy • Class 11: Organizing for innovation • Class 12: Class presentations

Presentations • Choose a business involved in a tech innovation • Presentation 1 • Strategicanalysis of pastdynamics • Describehistorytechnological innovation and industrydynamics to create & capture value • In terms of relevant theoriesof Parts I & II • Focus on rivalryestablishedplayers & new entrants

Presentations • Presentation 2 • Strategicchoices for the future • From the viewpoint of business & recenttechnological innovation • in terms of relevant theoriesof Part III • Whatwouldestablishedplayers vs new entrants do? • Whywouldtheymakesuchstrategicchoices?

Examples of choices… non-exhaustive list! • Car industry • E.g. electrical / hybrid cars • E-businesses • E.g. social media, insurance,… • Biotech & pharma • E.g. UCB, biotechinbrussels.be,… • Mature industries underthreat • E.g. newspapers… • ...

Case-study • On chosenfirms • Elaborate on presentations • 6000-8000 words • Create a group blog to monitor progress of presentations and cases

Marking • 10 points • class presentations & case-study • participation in class! • 10 points • 1 question on your case-study • 1 open question

Strategic management of technological innovation • How to obtain, use or developtechnology to achieve a new competitiveadvantage or to defend an existingcompetitiveadvantageagainsterosion LAST CLASS How tosustainably create and capture value of innovation

Today 1) Tech Strategydifferentfromgeneral business strategy? • Reading • « Increasingreturns& the new world of business » 2) Main framework for industryanalysis • 5 forces framework • Apply to biotechnologyindustry • Reading • « Can science be a business?»

Discussion Reading • Who has read? Discuss! • Whyhas Nokia dumpeditsown mobile operating system Symbian? • Symbianis world leader in marketshare! • Android phones • 1 yearago: 1/25th of market • Now: ¼ of market

Increasingreturns • Marketinstability • More accuratethan in text? • «Thosethat are growing, willgrow more; thosethat are shrinking, willshrink more » • Unpredictability • Multiple potentialoutcomes • Small changes in interdependence, large effects • Samsung leftSymbian, joinedAndroidplatform • Lock-in • Due to customerswitchingcosts • Inferiorproductcan come to dominate!

Increasingreturns • Winner-takes-it-all tendency • Fat profits for winner(s) • Others • Eitherloseeverything • Or becomecomplementors to winningplatform

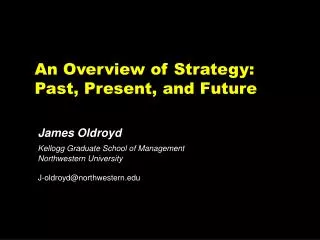

Talk of a « New Economy » • New Economy? • Post-1995 acceleration • Exponentialgrowth in computer speed, memory & interconnectedness • Development of the Internet • Frictionlesseconomy? • No inflation of costs, no diminishingreturns… • What do youthink? • «The computer chip has transformed us at least as much as the advent of electricity or internalcombusionengines »

1 2 3 4 Pre-internet computers Rise of the Internet Stock market crash Normalization? – 45% NASDAQ Points 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Year Launch of Amazon.com

Onlytrue to someextent • Not jobless technologies… • Limitations on human attention & time • Substitution one technology for another? • Productivity revival new economy? • Primarily computer hardware, telecom… • Withspillover to 12% economyinvolving manufacture durable goods • Mostly in US, not in Europe! • Why? • Greatestbenefits computers in the past?

Joblesstechnology possible? • See article on 3D manufacturingtechnology • Appeared in The Economist • Seehttp://technologystrategy.skynetblogs.be/

In sum: technologystrategy • How differentfrom business strategy? • moreuncertainty • verysmall portion new tech leads to new products/processes • more use of intellectualpropertymanagement • R&D, protection & translation tacitknowledge • probability of radically new products/services • biggeropportunities for new ventures

In sum: technologystrategy • How differentfrom business strategy? • alignmentneededwithHR/organizationaldynamics • E.g. • especially if basic scientific R&D isinvolved • Tension customer orientation vs technologicaldiscovery? • in some aspects differentdecision-making • Standards, increasingreturns, tipping points, first moveradvantage…

2nd part class: Industry analysis • What is an “industry”? • Firms producing similar principal products/services • 2 goals of industry analysis? • Assess attractiveness industry structure • Should we get in or out? • Can we shape industry structure in our favour • Once in, can we improve or not?

Read article + Break • Read hand-out • « Can science be a business? » • Think about the attractiveness of the biotechindustry • Think about the industry structure and how itcouldbechanged

Industry analysis: 5 forces POWER SUPPL I ERS POWER BUYERS THREAT OF ENTRY THREAT OF SUBSTITUTES

1Competitive rivalry • Among existing competitors • Competitor balance • Numerous or roughly equal in size & power? • Industry growth • Slow often means fierce rivalry • Fast could mean rivalry about profit is still coming! • Fixed costs • High often means fierce rivalry • Exit barriers • High tends to increase rivalry (esp declining ind) • Low differentiation?

Global biotechindustry • Competitiverivalry? • Large number of biotech startups and SMEs • Alongsidesmallnumber of large companies • Novartis, Roche,... • High fixedcosts • Few companiesmake profit • Struggle to discover « biotech blockbuster » • >Overallmoderatelystrongrivalry

2Threat of Entry • Height entry barriers • Economies of scale and experience • Automobiles, advertising FMCG, pharma • But Internet banking (only 10,000 customers to be viable) • Expected retaliation • Price war or marketing blitz; global retaliation • E.g. Coca-Cola or videogame industry • Access to supply or distribution channels • Bypassed by Dell and Amazon • Legislation or government action • Lengthy & costly clinical trials in biotech industry

2Threat of Entry • Height entry barriers • Switching costs customer • Long-distance telephone vs Skype • Diversification from other markets • Leverage existing resources and capabilities • Apple and music distribution

Global biotechindustry • Threat of entry • Stronggrowth, but high entry barriers! • Strongintellectualproperty protection • Most biotech start-ups are… • Academicresearch spin-offs • Long start-up periodswithlittle profit • High fixedcosts • But pharma diversifyingintobiotech! • >Moderatelystrongthreat

3Threat of substitutes • Price/performance ratio • Alumnium vs steel in automobile applications • Videoconferencing vs travel • Extra-industry influences • Always present, always take into account! • Demand wired teleph lines in emerging economies • Capped due to choice for wireless mobilies • How many people have mobile phone access?

Global biotechindustry • Threat of substitutes? • Medicalbiotech • conventionaltherapeuticdrugs • Less effective thanbiotechdrugs • BUT! New threat of « biosimilars» • http://www.economist.com/node/17316667 • Traditional pharma • Ownerbecomespoacher • At the moment, moderatethreat

4Power of Buyers • Power of buyers (not necess ultimate customers) • Concentrated buyers • Telecoms didn’t want Nokia to partner with Google • Low switching costs • Low for weakly differentiated commodities • Steel, mobile phones (not smartphones)... • Buyer competition threat • Buyer own supply facilities? • Threat of backward vertical integration • E.g. window manufacturers against glass manufact

Global biotechindustry • Power of buyers? • Main buyersare… • Medicalbiotech • Healthcare providers such as GP doctors, hospitals,… • Agricultural biotech • Farmers, growers… • One companyownership of innovation • Patent protected = Lessbuyer power • Reference pricingimposed by government • More buyer power • >Overall…moderatethreat

5Power of Suppliers • Power of suppliers • Concentrated suppliers • Iron ore industry: 3 main producers • Fragmented steel companies: weak bargaining power • High switching cost • Microsoft’s operating system • Buyers prepared to pay premium to avoid hassle • Supplier competition threat • Foward vertical integration: e.g. on-line booking • Low-cost airlines cut out travel agencies

Global biotechindustry • Power of suppliers? • Major suppliers are • Manufacturers of labequipment, software publishers, chemicalcompanies… • Littledifferentiationbetweensuppliers • Less supplier power • Yet, more supplier power • smalllikelihoodbackwardintegration • buyerscan’t substitute certain rawmaterial or equipment • > Moderatethreat

Industry analysis: difficulty! • Define the right industry • Different market segments • E.g. Biotech industry • Converging industries • Pharma (marketing) & biotech (discovery) • Telephone & photographic • Kodak vs Nokia or Samsung • Complementors (sixth force?) • 1+1>2 • Dell and Microsoft () • ARM & Apple

Achieve accredited supplier status e.g. Microsoft ecosystem (or business schools) Fragmented nature of doctors and hospitals good for pharma! BUTcollaboration with centralized government drug-specifying agencies Competition and Collaboration Internet customer self-service, co-creation or customization e.g. Amazon, Made.com (on-line furniture retailer), Dell Trade associations may promote safety standards or technical specifications Collaborative timing Microsoft MS-DOS OS & IBM’s personal computer

To read for next class • “Is the Internet a US invention?” • By David C. Mowery & Timothy Simcoe • Research Policy 31 (2002), pp. 1369–1387 • Additional reading if you have time… • “China vs the World” • By Hout and Ghemawat • Harvard Business Review, December 2010