Yield Curve Analysis

Yield Curve Analysis. Yield Curve Definitions. What is Yield? A bond’s yield is a measure of its potential return given certain assumptions about how the future will unfold. We generally associate yield to maturity as our standard meaning for yield, but there are other forms of yield:

Yield Curve Analysis

E N D

Presentation Transcript

Yield Curve Definitions • What is Yield? • A bond’s yield is a measure of its potential return given certain assumptions about how the future will unfold. • We generally associate yield to maturity as our standard meaning for yield, but there are other forms of yield: • Current Yield • Yield to call • Yield to worst

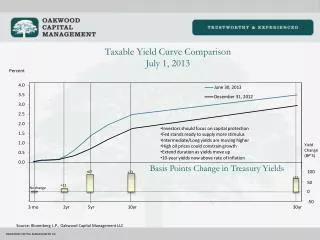

Yield Curve Definitions • What is a yield curve? • A key function of the yield curve is to serve as a benchmark for pricing bonds and to determine yields in all other sectors of the debt market (corporates, agencies, mortgages, bank loans, etc.).

Yield Curve Analysis • Four “classic” yield curves • Upward sloping • Downward sloping • Flat • Humped

Types of Yield Curve Shifts • Parallel • A flattening or steepening of the yield curve (i.e. a change in slope) • A change in the curvature of the yield curve

Yield Curve Shifts • An upward shift in the level is typically accompanied with a flattening of the yield curve and a decrease in its curvature. • A downward shift in the level is typically accompanied with a steepening of the yield curve and an increase in its curvature.

Yield Curve Facts • The yield curve changes shape and slope. • The yield curve changes level. • The yield curve is typically upward sloping. • Short rates are more volatile than long rates.

A Bond as a Package of Zeroes • The traditional approach to bond valuation is to discount every cash flow of a fixed income security using the same interest or discount rate. where: C = coupon payment M = principal payment y = yield measure (typically YTM) n = number of periods over life of bond

A Bond as a Package of Zeroes • Finance theory tells us that any security should be thought of as a package or portfolio of zero-coupon bonds. • The proper way to view a 4-year, 6% coupon Sovereign is as a package of zero-coupon instruments. • The 4-year security should be viewed as a package of 8 zero-coupon instruments that mature every six months for the next four years. M C C C C C C C C

Arbitrage-Free Valuation Approach • This approach to valuation does not allow a market participant to realize an arbitrage profit by breaking apart or “stripping” a bond and selling the individual cash flows at a higher aggregate value than it would cost to purchase the security in the market. • Arbitrage profits are possible when the sum of the parts is worth more than the whole or vice versa. • Because this approach to valuation precludes arbitrage profits, we refer to it as the arbitrage-free valuation approach.

Sovereign Spot Rates • To implement arbitrage-free valuation it is necessary to determine the theoretical rate that the Sovereign would have to pay on a zero-coupon security for each maturity. • ‘Theoretical’ because most Sovereigns do not issue zero-coupon bonds, with the exception of short-term discount notes. • Zero-coupon securities are created by dealer firms, such as Banc of America Securities. • The name given to the zero-coupon Sovereign rate is the Sovereign spot rate.

More Definitions • A spot rate is the rate used to discount a single expected future cash flow. • Strip rates are created from Separate Trading of Interest and Principal. • The most recently issued securities are used to create a theoretical spot curve…these are called the on-the-run or actives Treasury securities – I25. • In practice the yield on the on-the-run Treasury is adjusted such that the bond is at par…this is the par yield.

Par Curve • The par rate is the discount rate at which the bond’s price equals its par value. • The reason for this adjustment is that the observed price and yield may reflect cheap repo financing available from an issue if it is “on special”.

Building the On-the-Run Curve • Yields for missing maturities are interpolated using linear approximation. • Yield (n) = Yield (lower) + (Yield (upper) - Yield (lower)) x (n-lower)/(upper-lower) • What is the interpolated yield for a 4-year Treasury? • Yield (4) = Yield (3) + (Yield (5) - Yield (3)) x (4-3)/(5-3) • Yield (4) = 4.6437% + (4.6172% - 4.6437%) x (4-3)/(5-3) • Yield (4) = 4.6305%

Theoretical Spot Rates • The theoretical spot rates for Treasury securities represent the appropriate set of interest or discount rates that should be used to value default-free cash flows. • A default-free theoretical spot rate can be constructed from the observed Treasury yield curve or par curve. • The raw material for all yield curve analysis is the set of yields on the most recently issue (i.e. on the run) Treasury yields. • The U.S. Treasury routinely issues seven securities – the 3- and 6-month T-bills, the 2-, 3-, 5-, and 10-year notes, and the 30-year bond.

Determining Spot Rates • Suppose you observe the following data for three Treasury securities with annual compounding and exact maturities: • In order to find the spot rates from this data, we need to “strip” the coupons from the bonds and value them as standalone instruments.

Determining Spot Rates • The cash flow timeline from the stripped cash flows is as follows: 1 2 3 0 1-year bond -96.6463 +100 2-year bond -100.000 +3.8 +103.8 3-year bond -100.000 +4 +4 +104

Determining Spot Rates • Spot rates are used to discount a single cash flow to be received at some specific date in the future. • Since these bonds all have the same issuer, all cash flows received at t=1, must be discounted at the same rate. • The 1-year zero coupon bond has only one cash flow, we can use its YTM as the discount factor for other t=1 cash flows, i.e. use 3.62% as the one-year spot rate Z1. • The approach that we are employing to create a theoretical spot rate curve is called bootstrapping.

Determining Spot Rates • We can use the one-year spot rate to discount the cash flows for the 2-year bond as follows: 100.000 = 3.8/(1 + Z1)1 + 103.8/(1 + Z2)2 100.000 = 3.8/(1.0362)1 + 103.8/(1 + Z2)2 100.000 – 3.93756 = 103.8/(1 + Z2)2 96.06244 = 103.8/(1 + Z2)2 1.080547194 = (1 + Z2)2 1.03949372 = 1 + Z2 Z2 = 3.949372%

Determining Spot Rates • We can use the one- and two-year spot rates to discount the cash flows for the 3-year bond as follows: 100.000 = 4/(1 + Z1)1 + 4/(1 + Z2)2 +104/(1 + Z3)3 100.000 = 4/(1.0362)1 + 4/(1.03949372)2 +104/(1 + Z3)3 1.125079487 = (1 + Z3)3 Z3 = 4.0066406%

Valuing Bonds With Spot Rates • We can use the spot rates to value other bonds issued by the same entity or by adding a credit spread to value bonds issued by another entity. • Recall, Z1 = 3.62%, Z2 = 3.949%, Z3 = 4.007% • Use these spots rates to calculate the value of a three-year, annual-pay, 5% coupon bond with the same risk characteristics as the previous bond. Bond Value = 5/(1 + Z1)1 + 5/(1 + Z2)2 +105/(1 + Z3)3 102.778 = 5/(1.0362)1 + 5/(1.03949)2 +105/(1.04007)3

Valuing Bonds With Spot Rates • A coupon-bearing bond can be purchased and have the coupons stripped. • If the stripped security, discounted at spot rates, is worth more than the coupon security, then dealers can engage in arbitrage to drive the prices back into equilibrium (by the coupon security and sell the stripped cash flows). • This process of stripping and reconstitution assures that the price of a Treasury issue will not depart materially from its arbitrage-free value. • Empirical evidence suggests that non-U.S. government issues have also moved toward their arbitrage-free value as stripping and reconstitution of cash flows has been allowed.

Hypothetical Example: Valuation for 8%, 10-Year Treasury Using a Spot Curve Illustration of Spot/YTM The yield to maturity on this bond is 7.014%

Yield Spread Measures • There are three yield spread measures commonly used in practice: • Nominal Spread: an issue’s yield to maturity minus the yield to maturity of a Treasury security of similar maturity. • Static Spread (Z-Spread): spread over the spot rates in a Treasury term structure. The same spread is added to all risk-free spot rates. • Option Adjusted Spread (OAS): used when a bond has embedded options, this spread can be thought of as the difference between the static spread and the option cost. Z-spread - OAS = Option cost in percentage terms

Yield Spread Measures • Use the following information to calculate the nominal spread and static spread: • Use the previous spot rates ( Z1 = 3.62%, Z2 = 3.949%, Z3 = 4.007%) to determine the spread for a 3-year, 4% annual coupon ABC Manufacturing bond trading at 95. • The YTM on the ABC bond is 5.87% while the YTM on the three-year Treasury is 4%. The nominal spread is 187 basis points. • Static spread: 95 = 4/(1.0362+SS)1 + 4/(1.03949+SS)2 +104/(1.04007+SS)3 SS=187 basis points

Yield Spread Measures • Suppose you learn that the ABC Manufacturing bond is callable and that it has an option adjusted spread of 165 bp. • The cost of the embedded option is: • Z-spread (187 bp) - OAS (165 bp) = 22 basis points • For callable bonds, the OAS will be less than the Z-spread since you receive compensation for writing the option to the issuer, i.e. you have allowed the issuer the right to call the bond and the issuer has paid you for this right. • For putable bonds, the OAS will be greater than the Z-spread since you must pay for the right to put the bond back to the issuer.

Yield Spread Measures - Recap • Typically, the Z-spread and nominal spread will be close for a standard, coupon-paying bond. • The main factor causing any difference between the Z-spread and nominal spread is the shape of the Treasury spot curve. • The steeper the curve the greater the difference. • The option-adjusted spread is used to reconcile value with market price. • OAS is model dependent, i.e. the computed OAS depends upon the model used (binomial, Monte Carlo simulation). • OAS spread is used for bonds with embedded options. The option value is dependent on interest rate changes in the future. • The Z-spread does not consider how the cash flows will change when interest rates change…zero volatility of interest rates.

Forward Rates • A forward rate can be determined from the spot curve with the assumption of arbitrage-free valuation. • For instance, suppose we find the spot curve to look like the graph below: • If we have $100 to invest for three years do we want a three-year spot return? How about a one-year spot followed by two more years of spot returns…..

Forward Rates • Graphically, we need to assess the time line of interest to us: • The current one-year spot rate, z1, is 4.7599% and the current two-year spot rate, z2, is 4.6892%. z2 z1 1f1 4.6892% 4.7599%

Forward Rates • Graphically, we need to assess the time line of interest to us: (1+ z1)*(1+1f1) = (1+z2)2 (1+ 0.047599)*(1+1f1) = (1+ 0.046892)2 (1.047599)*(1+1f1) = 1.09598286 1+1f1 = 1.046185477 1f1 = 4.6185477% 4.6892% 4.7599% 4.6185%