Download

1 / 51

530 likes | 719 Views

Unit 4 The balanced Scorecard Implemetation. Overview.

E N D

Unit 4 The balanced Scorecard Implemetation

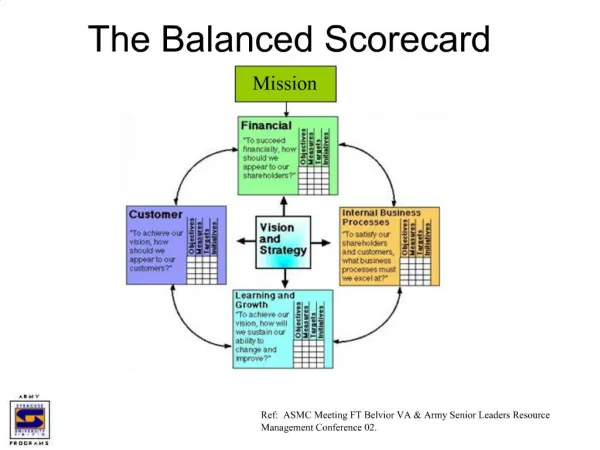

Overview The aim of this unit is to develop an understanding of how a balanced scorecard should be implemented. For this reason at the end of this unit you should be able to understand and explain what are the critical managerial practices for a successful balanced Scorecard implementation.

Key questions How should be a balanced Scorecard implemented ? How can managers define right measures for a successful balanced Scorecard implementation ? What are the critical managerial practices for a successful balanced Scorecard implementation ?

About the implementation of the balanced Scorecard • A successful balanced Scorecard implementation will enable employees at all levels of the organization to understand what they can do to help the organization meet its strategic objectives. • Once implemented, the balanced Scorecard allows the organization to test linkages and correlations between the various measures and consequently use this information to manage the organization.

Discussion question How can managers know whether the organisation strategy is right ? How can a company’s board communicate organisation strategy, mission and vision to their mid-level managers and line workers ? Take 10 min to think about

About the implementation of the balanced Scorecard • A successful balanced Scorecard implementation takes into account • Change management principles and issues; • Effective communication throughout the organization; • Implementing and utilizing the proper technology to gather and produce the measures;

Management responsibility Measurement analysis improvement Resource management Product realisation Product About the implementation of the balanced Scorecard Requirements Sat isfact ion Customer Customer Input Output The balanced Scorecard process also needs to incorporate the philosophy of continuous improvement. This will help ensure that measures are always correct, timely, and relevant. Some examples of continuous improvement process activities can include revising measures periodically, ensuring there is a timely feedback, and that there is an effective feedback mechanism in place.

Discussion question What happens when good performance in one area is offset by bad performance in another ? How can you make your performance measures inter-related ? Take 10 min to think about

Organisation Level Scorecard Organization Group/ Department Level Scorecard Group/ Department Individual Measures & Metrics and Scorecard Individual balanced scorecard architecture is unique to each organization Each organization is unique and so ultimately follows its own path for building, implementing, and maintaining a balanced Scorecard. Thus the balanced Scorecard architecture is unique to each organization and is dependent on what measures and metrics the company decides to focus upon. The balanced scorecards need to be developed for each level of the organization. This would help the employees to understand and follow the corporate strategy. The balanced Scorecard building process starts always with the organization’s strategy definition and it is an iterative process with a seteady link to the strategy. The scorecard provides a mechanism for aligning the individuals’ goals with organizational goals as it is shown from the following diagram.

Identify Organisation Identify Organisational Level Organisational Objectives to Scorecard strategy reach strategy Organization Group/ Group/ Group/ Select CSFs Department Department Department that the group Measures & Level Objectives can impact Metrics Scorecard Group/ Department Individual Select CSFs Individual Measures & that Individual Goals Metrics has impact on and Scorecard Individual balanced scorecard architecture is unique to each organization In the alignement process of individuals goals with organisational goals, corporate level measures can be broken down to lower level metrics within the organization. The following diagram shows how the organization’s strategy can be translated into objectives, critical success factors (CSFs) and measures which have meaning to individuals at all levels of the organization.

balanced scorecard architecture is unique to each organization The process of traslating organization’s strategy into objectives, critical success factors (CSFs) and measures for individuals at all levels of the organization enable local managers and employees to determine where they need to focus their efforts and what they must do well in order to improve the organisational effectiveness. From the individual’s perspective, the balanced Scorecard process helps employees to make a connection between their behaviors and their contribution to the business outcome. Scorecards should be always created for each level of the organization.

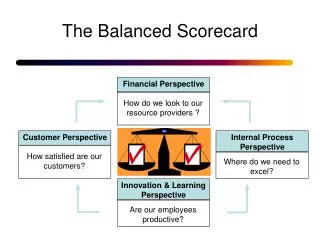

Customer Retention • Customer satisfaction Customer Financial • Reduce unit cost • Reduce Cycle time Vision & Strategy Learning & Growth Internal Process To reflect the hierarchy of strategy deployment through the balanced scorecard, scorecards may have different measures and weightings for various employee groups Executive Scorecard 40% 20% • ROE greater than Cost of Capital • Increase earnings per margin 20% 20% • Meet target revenue % from new products & target rollout date

Customer Retention • Customer satisfaction Customer Financial Vision & Strategy Learning & Growth Internal Process Employee Scorecard 10% 40% • Net profit vs Budget 10% 40% • Increase gross margin on old product • Meet target revenue % from new products & target rollout date • Increase net margin • Notice the different weights assigned to the quadrants .. Do you agree this allocation? • Can you justify the difference between the Executive Scorecard and Employee Scorecard Take 10 min to think about

Activity - Make a list of the possible factors that in accordance with your point of view affect a successful balanced Scorecard implementation.

Factors affecting a successful balanced Scorecard implementation The following are some relevant factors affecting a successful implementation of the balanced Scorecard are introduced. • It must be driven from the top of the organisation and the leadership needs to be committed to its success. • Effective communication is needed within the organisation throughout the balanced Scorecard implementation. • Communicate the need for measuring to all impacted people and groups. • A balanced Scorecard will not be effective unless you change behaviours. • Determining how you will overcome resistance to implementing performance measures or becoming measured. • Finding and removing obstacles before the balanced Scorecard implementation begins. • Finding and utilising resources and people that support the balanced Scorecard implementation effort. • Allowing adequate time for people to accept the balanced Scorecard adoption. • Defining the right measures and metrics. • Adopting an effective information system to support the balanced Scorecard implementation.

Right metrics for a successful balanced Scorecard implementation One of the key criteria for a successful implementation of the balanced scorecards is the quality of the measurements being implemented. The following template provides an approach to identify Metrics to be used in the balanced Scorecard.

Right metrics for a successful balanced Scorecard implementation • The suggested template can be used as a methodology to: • Define strategic objectives. Once the organisation strategy has been defined the strategic objectives/goals can be identified - What are the objectives/goals related to the organisation strategy ? • Identify business objectives. The objectives should be balanced across multiple dimensions of performance - What are the business objected following from the organisation strategy ? • Identify a set of possible metrics to measure the objectives - What are the metrics which we would like to implement to assess organisation performances against the defined targets of the business objectives ? • Identify type of metric: Outcome (Lagging) or Performance Driver (Leading) - What type of measures we want to adopt to control our businesses ? • Define strengths and weaknesses for each metric: behaviours the metric may drive, availability of data, ease of collection, frequency of reporting, relevance to business and strategy. What are the main strength and weakness features of our measures ? • Implement metric - Make the metric part of the everyday activities.

Perspectives Objectives Measures and Metrics Finance / Shareholder • Assure future access to capital • Maximize Product Margin • Maximize Profitability • Solvency, Bond rating • Break-even point in units,Contribution • Net Sales, Capital Turnover and Operating income Customer • Minimize Customer complaints • Monitor customer’s perception of value • Provide Quality Service • Customer satisfaction, Number of customer complaints • Customer profile and Focus groups • On-time delivery percentage, Respond time to customer service and requests Core Business Process • Monitor Purchasing activities • Monitor Materials Management • Provide Production Flexibility • Effective Education Program • Number of suppliers, Supplier lead-time • Raw materials supply accuracy, Back order volume • Number of setups per day, Average lot size • Improvements in error statistics, Student feedback Innovation and Learning • Integrate use of new technology • Monitor research program management • Production gains from new technology, Technical innovation • Research spending per time period Right metrics for a successful balanced Scorecard implementation The strategic objectives as well as both the business objectives and the measures/metrics have to define in each performance perspective of the balanced Scorecard. In the following an example of objectives and measures definition for each balanced Scorecard’s performance perspective is provided.

The role of information systems for balanced Scorecard implementation “If the information system is unresponsive, … it can be the Achilles’ heel of performance measurement” - Kaplan & Norton. Information systems play a critical role in supporting the implementation of the balanced Scorecard. An information system allows executives both to breakdown the summary measures and to perform queries on any unexpected trends to find the source of the trouble. The type of information system selected depends on the size and complexity of the organization. The information system tool chosen also depends on what measures and how many measures are being tracked. Prior to selecting the tool a cost/benefit software selection can be done to see which tool is the best for that particular organization. The tools used to build and maintain the balanced scorecard process vary from simple tools like Excel to more sophisticated ERP tools like SAP and PeopleSoft. In the last years a lots of software vendors have developd application based on the balanced Scorecard methodology. Some examples of balanced scorecard tools are SAS Institute’s Enterprise Scorecard, Corvu, Cognos, Comshare, and Gentia.

Implementing the balanced Scorecard To realise the full benefits of the balanced Scorecard, it should be adopted for all key organisational functions. This will provide: • common methodology and co-ordination; • framework for all organisational performance measurement efforts; • common “language” for organisational managers; • common basis for understanding measurement results; • an integrated picture of the organisation overall. In order to drive you in implementing a balanced Scorecard in the following nine best practice of implementation will be presented.

Best Practices for balanced Scorecard Implementation Make a commitment at all levels — especially at the top level. Senior management leadership is vital throughout the performance measurement and improvement process.

Best Practices for balanced Scorecard Implementation Develop organisational goals. To be meaningful, they must include measurable objectives along with realistic timetables for their achievement.

Best Practices for balanced Scorecard Implementation Offer training in improvement techniques to expand employees’ technical capabilities and to achieve “buy-in” for undertaking meaningful improvement efforts.

Best Practices for balanced Scorecard Implementation Establish a reward & recognition system to foster performance improvements. Thus, employee incentives will tend to reinforce the organisational objectives being measured by the BSC.

Best Practices for balanced Scorecard Implementation Break down organisational barriers - Like any other change initiative, to be successful the organisation must overcome employee resistance to change by open communication, education, and publishing success stories

Best Practices for balanced Scorecard Implementation Make realistic initial attempts at implementation. If initial attempts are too aggressive, the resulting lack of organisational “buy-in” will limit chance of success. If implementation is too slow, organisational momentum may suffer.

Best Practices for balanced Scorecard Implementation Integrate the Scorecard into the organisation. Incorporate performance measurement & improvement into existing management structure, rather than treating it as a separate program.

Best Practices for balanced Scorecard Implementation Change the corporate culture. To achieve long-term success, it is imperative that the organisational culture evolve to the point where it cultivates performance improvement as a continuous effort.

Best Practices for balanced Scorecard Implementation Institutionalise the process. Creating, leveraging, sharing, enhancing, managing and documenting BSC knowledge will provide critical “corporate continuity” in this area.

The case study The balanced Scorecard project at Wakefield Metropolitan District Council: the way to deliver performance management around the Best Value legislation Take 30 min to think about

The case study The context Not only are companies in the private sector focusing on enhancing their efficiency and customer satisfaction ratings, but public agencies are also under scrutiny to deliver better services at lower cost. To insure districts are delivering cost-effective services, the British Government mandated all local organisations to “achieve 2% efficiency savings/year for a continuing five year cycle.” In addition, each district must meet performance standards tied to the quality of services delivered. The government identified key areas of Corporate Health, Cultural Services, Education, Environmental Health and Trading Standards, Environment, Housing, Taxes, Planning, Social Services, and Transport. These make up the basic themes for local public services in districts such as Wakefield. Source: adopted from LOTUS - IBM

The case study ABOUT WAKEFIELD With a population of about 300,000 citizens, Wakefield District is located in the north of England; it is one of the five districts of West Yorkshire. The City of Wakefield is the seat of government for the district. The Council is responsible for providing most local services with the exception of police and fire. It has 13,500 employees and an annual turnover of approximately £500 million. Source: adopted from LOTUS - IBM

The case study CHALLENGE Given the national government issued Best Value, a program challenging all councils to increase efficiency and effectiveness, Wakefield and all other local authorities must implement a system to measure its performance in delivering services to its citizens. Within five years, each District must be performing in the upper 25% of the March, 2000 levels. The government has established nearly 200 statutory performance indicators covering most services delivered. How could Wakefield identify its starting points? How could it track its progress? How could it accurately report its performance? Source: adopted from LOTUS - IBM

Targets Targets Targets Targets The case study SOLUTION Development of a balanced Scorecard using and relying on IT through powerful reporting software. Source: adopted from LOTUS - IBM

The case study balanced SCORECARDS REFLECT EFFICIENCIES IN AN ORGANIZATION To measure a district’s success, performance indicators were established for each area. The criteria are presented as “balanced Scorecards”, a methodology developed in conjunction with Arthur Anderson, in effect a report card measuring outcomes (e.g. percent of taxes collected, number of sick days lost, etc.) Within each scorecard, four criteria were used to categorise the outcomes: strategic objectives, cost efficiencies, service delivery outcomes, and quality/fair access. Best Value Source: adopted from LOTUS - IBM

The case study balanced SCORECARDS REFLECT EFFICIENCIES IN AN ORGANIZATION Like the other local authorities, Wakefield faces huge challenges. It lacked baseline information upon which to base its actions in meeting the Government’s Best Value criteria. Also, its culture did not reflect performance management practices. This is all changing. Using Lotus software applications (Lotus Notes™/Domino™ and ShowBusiness Cuber™ ), the Council developed a management system called Q-Net, the Wakefield Quality Network, running on its corporate intranet. Q-Net uses the Action Driven balanced Scorecard (ADBS) methodology, a means of displaying information graphically using the universal concepts of a traffic light (green = performance above the standard; yellow = within the standard; red = below the standard) making it easy for management to identify critical process problems or departmental inefficiencies. ADBS also supports analyses and action plans for each indicator. Drawing upon its existing data sources along with other databases created to capture new information, Wakefield outputs performance measurements in colored, graphical formats that assist its managers in tracking outcomes. “With the ShowBusiness/Lotus™ solution, we now have a tool to help us manage this process. This tool helps us understand which “Best Practices” really are the Best!” acknowledged Mr. Beeley, Strategic Manager of Corporate Best Value Group, City of Wakefield Metropolitan District Council. Source: adopted from LOTUS - IBM

The case study MANAGERS ARE LOOKING FOR THE GREEN The tax collection department has responsibility for collecting taxes as well as paying invoices. One of the cost efficiency measures local governments must report on is the level of taxes collected. Wakefield has evaluated its collection success rate for various taxes and determined it needed to address its ”yellow” criteria and turn them to ”green”. Source: adopted from LOTUS - IBM

The case study MANAGERS ARE LOOKING FOR THE GREEN What programs have the greatest impact on collecting taxes? For example, is it more effective to send delinquent taxpayers a letter versus take court action? The District is using the balanced Scorecard methodology by Q-Netto in order to evaluate the results. Wakefield’s target is to increase the Council Tax (the local resident property tax) collection rate from about 95% to over 96% by 2005. In current terms this will generate another £1.3million in additional annual income for the Council. Not only is Wakefield focusing on collecting monies in a more timely manner, but it is also concerned about reimbursing its suppliers more quickly. After reviewing the cycle times for processing invoices, management determined the time could be reduced, thereby improving relations with its vendors. The Finance Department re-engineered the payment process and entered an action plan into Q-Netso all employees could use the new process. As a result, the department has increased invoices paid in 30 days from 58% to 85%! The target is to pay 100% within 30 days by 2003. Source: adopted from LOTUS - IBM

The case study LIBRARIES, PARKS, MUSEUMS EVALUATE CUSTOMER SATISFACTION EASILY Public Services is another department that expects to reap the benefits of the implementation of the balanced Scorecard methodology by using the Domino/Cuber system. Libraries, parks, and museums want to provide services the public really wants and values. In the past, it conducted ad hoc surveys and implemented programs it felt the community wanted. Now Cultural Services is planning on implementing customer satisfaction surveys accessible on the web or from terminals placed in social service offices and sports centres. Because Wakefield by the adoption of the balanced Scorecard has a means of quickly collecting and analysing user input, it expects it can design and implement cultural services more in tune with its community. Program and performance information will be available to the public over the web. Source: adopted from LOTUS - IBM

The case study UPFRONT PREPARATION FOR TOP PERFORMANCE & LITTLE TRAINING TIME Wakefield worked with ShowBusiness to tackle the key areas of data and training. One of the most time consuming activities is populating the databases with reliable data. Much of the original data had to be cleansed and input manually into the system. Future data will be downloaded where possible from current systems. Another upfront task has been training of all personnel who will be using the system. Since the Q-Net is quite intuitive, Wakefield is finding managers require only about a half day of training. “Like every other council, we have been challenged by central government to implement Best Value and find savings of 2% of our £273 million budget, year on year for the next five years across all of our service areas.” Mr. Beeley went on, “Early reviews of our multi-million pound service areas have identified potential savings of 10% if performance is well-managed. For any organization, this is substantial! Managing performance with the focus on effectiveness, not just efficiency, is a powerful tool in improving public services and delivering Best Value.” Source: adopted from LOTUS - IBM

Read and Analyse 4.1 Supporting the balanced scorecard Sanger, MarkWork Study; Volume 47 No. 6; 1998

Maintaining the balanced Scorecard Sustainability and improvement of the balanced Scorecard and its processes will be achieved by incorporating a continuous improvement philosophy throughout the organization and by linking the ongoing scorecard review process to the annual strategic planning process. • The balanced scorecard process needs to be maintained, monitored, and continuously improved if it is to remain effective, so: • Review the results or measures being recorded, such as: Routine Review of Actual Results; Root cause analysis; Behavior review; Corrective actions; Lessons learned; Review of supporting activity measures by department. • Monitor the scorecard administration process, Perform an annual review of the entire balanced scorecard; Support of Strategic Objectives; Investments linked to measures; Capital Plan/Targets; Links to long term plans and initiatives; Link to supply chain strategy. • Business Results Achieved, such as Actual vs. Target - Improvement targets met; Review of lessons learned; Behavioral changes achieved; Aligned with Financial results.

Some lessons learnt by implementing balanced Scorecards • Balanced Scorecard takes a significant amount of time and effort to setup and administer. Detailed planning should start right from the beginning of the process. • Each organization will need to determine its own unique set of deliverables during the creation and implementation of the balanced Scorecard. • Allocation and commitment of key resources is a necessary requirement to the success of the balanced Scorecard implementation process. • It is critical that the effort be lead by the most senior executives. • balanced scorecards are seldom implemented in isolation to other initiatives and so need to be closely integrated with these other initiatives. Lessons … I

Some lessons learnt by implementing balanced Scorecards • Build extra time into your plan for establishing the common level of understanding, and implementing the metrics, processes, collection, and reporting. • A set of definitions should be published along with the balanced Scorecard to ensure the audience is using definitions and calculations consistently. • An effective balanced Scorecard should reflect organizational goals and objectives, it is not a metrics report card or a service level reporting mechanism. • Provide fast feedback to managers and employees - directly inform them of success or failure Lessons … II

Some lessons learnt by implementing balanced Scorecards • Keep the balanced Scorecard simple and focused on key strategic measures. Don’t confuse it with operational or status reporting. • Don’t wait until it’s perfect to roll it out. The act of publishing and beginning to understand and manage by the metrics drives change and improvement to the metrics and targets. • Educate and motivate the workforce. Confirm /develop measures that people can understand. • Give local managers the authority to define measures appropriate for their objectives and action plans, working within the overall strategy. Lessons … III

Some lessons learnt by implementing balanced Scorecards • The Key Performance Indicators need to link directly to the Critical Success Factors that support the overall strategic priorities. • The metrics selected must relate to and measure the business objectives which in turn must be fulfill the organization’s strategy. • balanced Scorecards are only effective if the measures and data that are gathered are relevant, accurate, and timely. • Focus on Continuous Improvement. As current needs and issues are addressed, target new areas for improvement and change or adjust measures accordingly. Lessons … IV

Unit Assignment Read and Analyse 4.2 “Benchmarking performance management systems” Amir M Sharif Benchmarking: An International Journal (2002) Vol. 9 N. 1 pp. 62-85

Read and Analyse 4.3 The golden rules for implementing the balanced business scorecard Roest, PimInformation Management and Computer Security; Volume 5 No. 5; 1997

Group On-line Discussion 4.1 What are the three most important factors affecting a right balanced Scorecard implementation ? While many aspects have been highlighted, you should be able to drill down to the top three criteria/issues/initiatives that must be ‘done right’ for successful implementation

Unit Assignment 4.1 • Select one of the papers from the Read and Analyse sections presented in the unit • Critically analyse this paper and write a 1000 word report • do you agree with the ideas presented in the paper • how do you assess the applicability/practicality of these ideas • can you reflect on where/how these ideas can have practical implications in you professional life