The Balanced Scorecard

The Balanced Scorecard. Linking Operations to Strategy. Information for Guiding Operations. Decisions cannot be based solely on financial information Much quantitative information cannot be reduced to monetary amounts Much information cannot be quantified

The Balanced Scorecard

E N D

Presentation Transcript

The Balanced Scorecard Linking Operations to Strategy

Information for Guiding Operations • Decisions cannot be based solely on financial information • Much quantitative information cannot be reduced to monetary amounts • Much information cannot be quantified • Much information provides feedback but not guidance

Criticisms of Traditional Measures • Lack of relevance • Many measures are interesting, but not useful • Market share, revenue, etc. • Trends may be useful • Measures may be poorly designed or collected • Customer satisfaction, employee morale, etc. • Goals are arbitrarily determined, beyond the ability of the system

Criticisms of Traditional Measures • Lack of vision • Short-term focus impedes decisions with long lead times or long-term payoffs • Focus on what is currently being done, not what should be done • Fail to consider the overall organization

Criticisms of Traditional Measures • Promote detrimental outcomes • Short-term thinking • Local optimization • Manipulation of operations or measures • Well-intentioned but detrimental actions • “The numbers these systems generate often fail to support the investments in new technologies and markets that are essential for successful performance in global markets” Eccles, p. 28

Signs of an Ineffective Performance Measurement System • Performance is acceptable on all dimensions except profit • Measures are not aligned with strategy • Measures do not reflect critical success factors • Competitive price, but customers do not buy • Functionality or quality may be more important to the customers

Signs of an Ineffective Performance Measurement System • No one notices if the measures are not produced • Not using them anyway • Irrelevant • Redundant • Questionable • Managers debate the meaning of the measures • Measures are confusing

Signs of an Ineffective Performance Measurement System • Share price is lethargic despite solid financial performance • Measures are backward looking • Share price reflects future expectations • The market expects that current performance will not continue

Signs of an Ineffective Performance Measurement System • Have not changed the measures or targets in a long time • Obsolete, easily met, do not foster change • Corporate strategy has changed • Measures become irrelevant

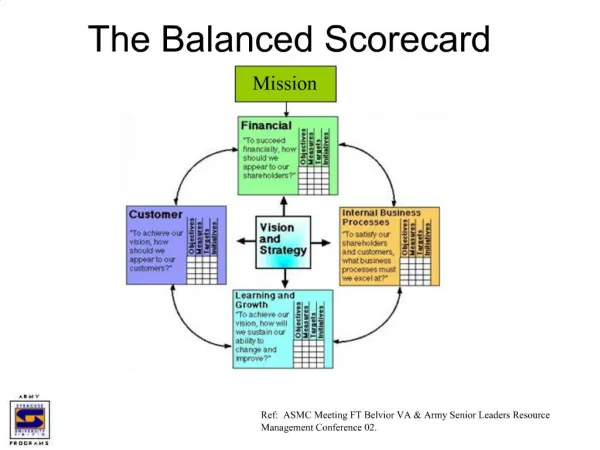

The Balanced Scorecard • Performance measurement and guidance tool • Balance between • Measures of current performance and long-term competitive abilities • Feedback and guidance • Financial and non-financial measures

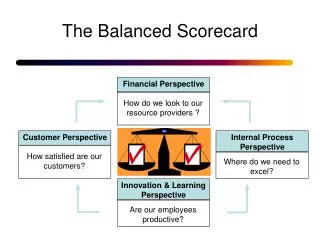

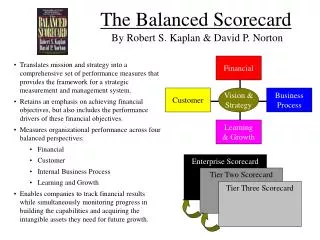

The Balanced Scorecard • Four aspects of firm performance • Financial • Internal business processes • Customer • Innovation and learning • Some entities may use more or less than four perspectives depending on their unique situations

The Balanced Scorecard • Financial perspective • How is the company doing financially? • Traditional financial measures • Operating income • Cash flow • Revenue growth • Stock price • Etc.

The Balanced Scorecard • Internal business perspective • At what must the company excel currently? • Manufacturing or service excellence • Backlogs • Cycle time • Quality • New product or service introductions • Etc.

The Balanced Scorecard • Customer perspective • How do our customers view the company? • Responsiveness to customer desires • Market share • Customer satisfaction • Customer retention • Customer’s perception of the company and its products • Etc.

The Balanced Scorecard • Innovation and learning perspective • Can the company continue to create value? • Technological leadership • Research and development • Employee training • Employee satisfaction • Investments in new technologies • Etc.

The Balanced Scorecard • The four perspectives are interrelated • Not a random collection of measures • Emphasizes the synergies and relationships existing within the company and with its customers • Innovation and learning results in better products and internal processes which please customers which then results in positive financial results • Strategy map

Designing a Balanced Scorecard • Step 1: Develop company strategy • Measures must relate to the strategy • Reflecting the critical success factors • Measures must be interrelated • Must understand how the perspectives influence each other • Organization-wide view replaces local focus

Designing a Balanced Scorecard • Step 2: Determine critical success factors (goals) • What must be achieved to survive, or what will cause the company to fail if it is not achieved? • Determine success factors for each of the four perspectives • Limit the number to items that are critical, not just interesting

Designing a Balanced Scorecard • Step 3: Determine the activities that drive the achievement of the critical goals • Must understand the linkages between the activities and the goals • Will this activity help us achieve the desired goal?

Designing a Balanced Scorecard • Step 4: Develop metrics to evaluate performance • Provide feedback and also indicate problem areas • Metrics may be financial, non-financial, trends, surrogates, internally or externally gathered, etc. • Should include leading and lagging measures • May not be “exact”

Designing a Balanced Scorecard Critical Success Factors Strategy Activities Measures Fedex Strategy – produce superior financial returns by providing high value-added supply chain, transportation, business and related services… CSFs – stock price growth, on-time delivery… Activities – increase operating income by reducing fuel usage, deliver packages to central sorting facility by midnight… Measures - fuel usage, acquisition of, or commitments to acquire, more fuel efficient planes, percent of packages arriving late…

Designing a Balanced Scorecard • Not a quick process • May take months to accomplish • Thought and analysis of strategy, critical success factors, activities, metrics • How do the pieces fit together?

Designing a Balanced Scorecard • Requires teamwork and collaboration • Different perspectives and expertise are required • No one individual has a complete view of the organization • Greater participation produces greater “buy-in” • Employees have a sense of ownership in the resulting scorecard • More likely to use the scorecard to guide their decisions

Implementing a Balanced Scorecard • Initiative must start with senior management • Understanding of overall strategy • Authority to make strategic decisions • Commitment level will determine success or failure • The project may fail if senior management does not show continued interest and support in the design process • The scorecard will be ignored if management does not promote its use for performance evaluation and guidance

Implementing a Balanced Scorecard • Link to databases and information system • Modify information system if necessary to collect and report the metrics • What data is available? What is not available? • How should it be collected? How often? • The scorecard should determine what data is collected • The data available should not determine the scorecard • Determine reporting procedures • Who gets the information? How is it reported? How often is it reported?

Implementing a Balanced Scorecard • Communicate to employees • What is being measured • Why it is being measured • What is expected of the employees • How to use the information • Develop scorecards for lower levels • Want the employees to understand what they must do to support the level above

Implementing a Balanced Scorecard • Periodic reviews • The scorecard must evolve with the company • Has company strategy changed? • Are the critical success factors still valid? • Are the activities still valid? • Are the metrics still valid?

The Road to Disaster • Senior management is not committed • No one else will be • Lack of consensus • Lack of commitment • Poor use of consultants • Provide expertise, but cannot take over the project without employee input

The Road to Disaster • Failure to communicate to employees • Risks “business as usual” • Lack of “push down” • Lower levels continue to operate as before • The scorecard cannot stay in the boardroom

The Road to Disaster • Carve it in stone • It will not ever be perfect • Poorly designed scorecard • Will not see strategic improvements even if individual measures show progress • The activities are not linked to strategy

The Scorecard as a Change Agent • The scorecard should be used to guide future operations and decisions • Four steps • Translate the strategy into action • Communicating and linking • Business planning • Feedback and learning

The Scorecard as a Change Agent • Translating the strategy into action • Strategy must be reduced to a set of quantifiable goals and measures that can be operationalized • “We want to be the best” will not do • Communicating and linking • Strategy must be communicated to all levels • Lower levels are the foundation on which the rest of the organization is built

The Scorecard as a Change Agent • Business planning • Integrate the financial plan with the business plan • Use the scorecard to allocate resources to critical activities • Assures critical activities receive adequate resources • Avoids the short-term spending mentality • Feedback and learning • Monitor short-term results to determine if progress is being made toward long-term goals • May need to refine the scorecard

Analysts’ “Top 10” List • Ernst and Young study of financial analysts’ use of non-financial measures • Improves earnings forecasts • 35% of a company’s valuation is attributable to non-financial information

Analysts’ “Top 10” List • The “Top 10” • Ability of the company to execute its strategy • Credibility of management • Does the company do what it says it will do? • The quality of the strategy • Will management’s vision create future value?

Analysts’ “Top 10” List • Innovativeness • How readily does the company adapt to changing technologies and markets? • Ability to attract and retain talented people • Market position • How quickly can the company realize sales, profits and cash flow from products introduced in the prior three years? • How strong is the company’s brand?

Analysts’ “Top 10” List • Management experience • What skills and experiences does the management team bring to the organization? • What is their success rate in similar situations? • Executive compensation • Are compensation policies aligned with strategy? • How many executives have their pay tied to value creation?

Analysts’ “Top 10” List • Quality of major processes • How well does the company execute its strategy? • Does it have plans and processes that enable it to adapt to changing market conditions? • Research leadership • How well does the management understand the link between creating knowledge and using it? • R&D budget as a percent of sales, profits and cash flow