Estimation and Hypothesis Testing

This course explores the fundamentals of estimation and hypothesis testing as they relate to investment decisions. Participants will learn how to assess the expected return on investments and apply statistical methods to estimate key parameters, such as returns and standard deviations, while considering the probability density functions (PDFs). Through practical exercises involving random sampling and estimators, learners will understand the importance of unbiased and consistent estimators, and how these concepts influence their investment strategies.

Estimation and Hypothesis Testing

E N D

Presentation Transcript

The Investment Decision • What would you like to know? • What will be the return on my investment? • Not possible • PDF for return • Assume the normal PDF • Use statistics to estimate E[r] and s. Use statistics to estimate the correct PDF. Can do for discrete PDF’s. For continuous PDFs, beyond the scope of this course.

The Game of Investing • Suppose you’re offered to play a game: • Cost: $1.25 • Flip a coin • If heads, you get $2 (return is 60%) • If tails, you get $0 (return is -100%) • Coin may be biased • Assume the true pdf for this investment is • Of course, this information is unknown!

The Game of Investing • You would like to know • What will the coin flip turn out to be? • Not possible • What is the PDF (probability of getting heads/tails)? • Not possible to know with certainty: need to estimate • E[r] and s • Not possible to know perfectly: need to estimate. • How to estimate? Why not flip the coin a few times?

Random Sample • Suppose you flip the coin 10 times and get • H, H, T, H, H, H, H, H, H, T • 8 heads, 2 tails • This is an independent random sample • A sample of observations generated by the same pdf • Independent: One outcome does not affect others • Nothing other than the pdf determines how observations are chosen. • No “cherry picking”: picking certain observations you like, and eliminating others • How do we use this information to estimate • f(heads) • E[r] • s

Estimators • Estimator – function of outcomes for a random sample. • An estimator is a random variable • It has it’s own PDF! • Let be an estimator of E[r] • Two important properties of estimators: • Unbiased: • Consistent: As the number of observations we observe becomes large, • Suppose we use the following rule to get our estimator of E[r]: • For any random sample, choose the first observation as our estimate of E[r]. • Call this estimator r1.

Estimator of E[r] • Is r1 unbiased? • For any random sample of any size, r1 is simply a random variable governed by the pdf • So E[r1]=12%=E[r] • r1 is therefore an unbiased estimator of E[r]

Estimator of E[r] • Is r1 consistent? • For any random sample of any size, r1 is simply a random variable governed by the pdf • So Var[r1]=0.5376 for any sample size. • r1 is therefore not a consistent estimator of E[r]

Estimator of E[r] • Suppose we use the following rule to get our estimator of E[r]: • For any random sample, take the average return as our estimator of E[r]. • Call this estimator .

Estimator of E[r] • Is unbiased? • What is ? Use stat rule #1 • is therefore an unbiased estimator of E[r]

Estimator of E[r] • Is consistent? • How do we find the variance of a sum of random variables? • We haven’t learned this yet, but we will later. • We can generate random samples of estimators to get some idea of the properties of their PDF. • For each outcome for an estimator, we need to generate a random sample of observations, and then compute the estimator. • Use Excel Spreadsheet (posted on course website)

Comment • Why do we use probability weights when calculating E[r] from a pdf, but when we estimate E[r] we just use an equally weighted average? • Given the PDF above, we should expect in any random sample to see heads 70% of the time. • Assume we draw a sample where exactly 70% are heads • 70% of the returns in the sample will be 0.60 • 30% of the returns in the sample will be -1.00 • A simple average across observations is equal to • Simple averages naturally put more weight on those outcomes which are more likely.

Estimator of Stdev[r] • How do we use data to estimate Stdev[r]? • Var[r]=E(r-E[r])2 = E[r2]-E[r]2 • Stdev(r)=sqrt(Var(r)) • Suppose we use the following rule to get our estimator of Stdev[r]: • Is the estimator unbiased? • Is the estimator consistent? • Use Excel spreadsheet.

Average • The same results apply to continuous PDFs • For a given random sample:

Estimates • When is the average a good estimate of E[r]? • When is our estimator for standard deviation a good estimate of Stdev[r]? • When you have a large sample of outcomes • When the PDF doesn’t change mid-sample

Stat Rules • Stat Rule 1.E • Let x1,…,xnbe a random sample of the random variable X. • Let y1,…,ynbe a random sample of the random variable Y. • Let zi=axi+byi, for i=1,…,n where a and b are constants. • Then • Stat Rule 2.E • Let x1,…,xnbe a random sample of the random variable X. • Let zi=axi+c, for i=1,…,n where a is a constant • Then

Estimated Sharpe Ratio • The Sharpe Ratio may be estimated as where we use the yield on a t-bill as a proxy for the risk-free rate.

Time and E[r] and Stdev[r] • E[r] and stdev[r] have a unit of time attached to them. • E[r]=10% over a year is much different than E[r]=10% over a day. • s[r]=0.16 over a year is much different than s[r]=0.16 over a day. • Let p denote a “short” time period (e.g., a month) • Let P denote a “long” time period (e.g., a year) • Let N denote the number of “short” time periods in a “long” time period (e.g., 12) • Let Ep[r] and sp[r] be the appropriate parameters over the short time period • Let EP[r] and sP[r] be the appropriate parameters over the long time period • Then to a close approximation,

How Good Are the Estimates? • Does the E[r] for a stock meet some pre-determined benchmark? • You can’t observe the PDF to calculate the true E[r] • Over the past 10 years, returns have been as follows: • From this you estimate E[r] to be 18.3% • Is this enough information to reject the hypothesis that the true E[r] for the PDF that generated this sample is 10%?

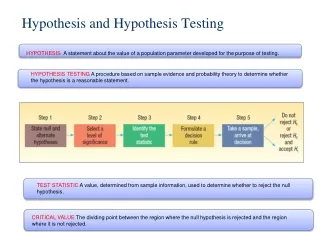

Hypothesis Testing • Null Hypothesis • The hypothesis to be tested • E[r]=10% • Alternative Hypothesis • E[r] ¹ 10%

Hypothesis Testing • c = distance of test statistic from null hypothesis that defines zone of acceptance.

Hypothesis Testing • Standard Practice: Choose c so that we know the probability of making a type 1 error.

Hypothesis Tests of the Mean • Let (X1, X2, …,Xn) be an independent random sample from anyPDF • True mean=m • True standard deviation=s • What PDF governs the outcome for the sample average? • The laws of statistics say that the sample average is approximately • Normally distributed • True mean=m • Standard Deviation= • The standard deviation of the sample average is called the “standard error”

Hypothesis Testing • Null Hypothesis • E[r]=10% • Alternative Hypothesis • E[r] ¹ 10% • Assuming the null is true, the sample mean is approximately normally distributed with • m=.10 • s=0.0921

Hypothesis Testing • For any normally distributed random variable, there is only a 5% probability of getting an outcome above m+1.96s or below m-1.96s. • Assuming the null is true, there is only a 5% chance of drawing a sample average above 0.10+1.96*(0.0921) =0.2805 or below 0.10-1.96*(0.0921)=-0.08052 • If the sample average is above 0.2805 or below -0.08052, we therefore conclude that it’s too unlikley (<5%) that we would observe such an outcome, given the null is true. • Hence, the null must not be true. Reject H0.

Hypothesis Testing The sample average we observe is 18.3% This is in the zone of acceptance. Do not reject the null hypothesis. “We cannot reject the hypothesis that the true mean is 10% with 95% Confidence.

Hypothesis Tests of the Mean • Example • Hypothesis: m =2% • Alternative: m¹ 2% • 100 years of stock market returns • Sample Average = 16% • Standard Deviation = 0.18 • Hence, standard error is 0.18/10 = 0.018

Hypothesis Tests of the Mean • c = 1.96*0.018 = 0.03528 • Assuming null hypothesis is true, too unlikely you would observe the actual sample mean. Reject the null hypothesis.