Download

1 / 0

0 likes | 97 Views

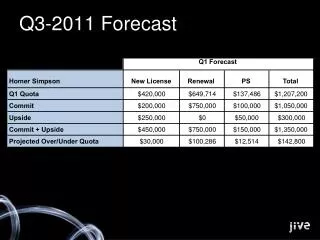

Nov 2011 Banking Sector Q3-2011 Update. P/E Regional Comparisons. P/E Sector Comparisons at ASE. Liquidity Sector Comparisons at ASE. Net Income Projections. Our Forecast Methodology of Net Income:

E N D