Download

1 / 21

210 likes | 500 Views

Unit 13 – Adjusting and Closing Entries. Previously…. All adjustments were made on the work sheet. The ledger accounts have not yet been changed. (currently, are incorrect and do not reflect the adjustments made on the work sheet)

E N D

Previously… • All adjustments were made on the work sheet. The ledger accounts have not yet been changed. (currently, are incorrect and do not reflect the adjustments made on the work sheet) • Adjusting entries are used to record the adjustments in the ledger accounts.

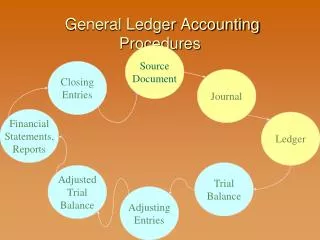

Adjusting Entries • Work sheet • Journal form • Post them to the ledger

Adjusting Entries • Work sheet • Journal form • Post them to the ledger • Adjusted Trial Balance

Closing Entries • Summary • Income statement: net income or net loss for a specific accounting period. (data found in revenue and expense accounts) • New accounting period = revenue and expense accounts should show zero balances. • “Matching principle” – revenue for each accounting period is matched with the expenses for that accounting period to determine net income or loss. • Closing the books: the process by which revenue and expense accounts are reduced to zero at the end of each accounting period.

Temporary (vs) Permanent Accounts • Temporary accounts: • Contain information for the current accounting period only • Balances not carried over to next accounting period • Examples: Revenue & Expense accounts • Permanent accounts: • Balances are carried forward from one accounting period to another (they are not closed – put to 0) • Examples: Asset, Liability, & Owner’s Equity accounts

Purpose of Closing the Books • Prepare Revenue and Expense accounts for the next accounting period (by reducing them to 0) 2) Updating the Owner’s Equity account - Increase or decrease of capital [Net income/loss, and Drawings]

Income Summary Account • Closing Revenue & Expense accounts Income Summary Account Transfer balances

Steps – Closing the Books • Close Revenue Accounts into Income summary • Close Expense Accounts into Income summary • Close Income summary into Capital • Close Drawings into Capital

Step 3: Close Income Summary into Capital Net income Credits > Debits Increases OE

Closing Books (from work sheet) • Same process. • (simply retrieving information from the work sheet) • Example: Page 244-248 • See Ledger Accounts (after adjusting and closing entries have been posted) – Page 246-248

Post-Closing Trial Balance • Created after adjusting and closing entries have been posted to the general ledger. • Purpose: prove mathematical accuracy of the general ledger. (debits = credits) … ready for the next fiscal period. • This trial balance is much shorter. • Only asset, liability, & capital accounts have balances. (others have been closed)

Post-Closing Trial Balance Example 249-250 (Effect of a net loss) …Decreases Owner’s Equity.

Updated Accounting Cycle New Accounting Period Begins Proof Post-closing Trial Balance Business Transactions Adjusting and closing entries posted Journalizing Journal Financial Statements Ledger Posting Financial Statements Prepared Ledger Work Sheet Journal Work sheet including Trial Balance Prepared Adjusting and closing entries journalized